The month of March saw the Federal Reserve Bank hiking interest rates by 25 basis points in a highly anticipated move. The central bank signaled that it would stick to three rate hikes this year amid speculation that the Fed could move for a more aggressive rate hike path.

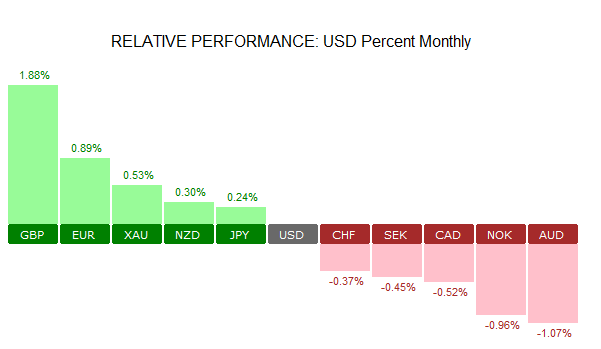

The U.S. dollar remained mixed across the board during the month. Elsewhere, officials in the EU and the UK agreed to a transitory Brexit deal that would enable the UK to prepare for an orderly exit from the EU. The news brought renewed optimism into the British pound. The GBP was the top performer of the month, gaining 1.88%. This was followed by the euro currency with gains of 0.89%.

Investors continue to remain bullish on the euro with speculation rising that the European Central bank could end its QE program this year. This comes amid the fact that consumer prices are not forecast to rise close to the ECB’s 2% inflation target rate until 2019. The ECB held its monetary policy meeting in March and left its interest rates and the QE purchases unchanged. However, the removal of the dovish language from the ECB’s statement was seen as a hawkish forward guidance.

The remainder of the central banks left monetary policies unchanged. The Bank of England signaled that the next rate hike will come in May.

April 2018 Monthly Outlook

Following the start of the first month of the second quarter, investors will be focused on the quarterly GDP performance across the various G7 economies. From a monetary policy perspective, we do not expect to see any big changes to interest rates coming this month.

However, the central bank economists will be closely monitoring the developments from the first quarter. With the market sentiment somewhat mixed on account of the global trade uncertainties growth could be seen taking a hit especially in the month of March after President Trump announced the tariffs on Steel and Aluminum imports as well as slapping China with tariffs of up to $60 billion USD.

Here’s a quick preview of the main events to look forward to in the month of April.

Bank of England to retain hawkish outlook

Geo-political risks aside, the Bank of England will be looking to keep the market speculation going about the potential rate hike in May. There is no monetary policy meeting scheduled from the Bank of England for the month April.

However, officials are likely to not miss any speaking engagements in order to drum up support for the rate hike in May. With consumer prices recently easing back and wage growth starting to rise, the central bank officials will be keeping a close watch on the inflation and wage growth data for the month of March, which will be released this month.

The downside being that consumer prices could once again rise in the month of March due to seasonal effects such as the Easter spending. The period around the Easter weekend typically see’s an increase in airfare costs which is expected to push consumer prices higher.

Still, as long as the rise in inflation remains a one-time thing, further data for the month of April could cement expectations if consumer prices ease back. This could potentially set the stage for the BoE to hike rates at the monetary policy meeting in May.

Ongoing developments on the Brexit will also play a factor.

Advanced Q1 GDP reports

Following the end of the first quarter, the last part of April will signal the release of the advance GDP reports from some of the key G7 economies. Focus will be on the U.S. and the UK GDP reports that are due later in April.

With the U.S. economy seen rising at a pace of 2.9% compared to the initial estimates of 2.6%, the markets are looking for the GDP growth to maintain the momentum. Initial estimates from various GDP trackers show that the U.S. economy might have advanced on average 2.4% – 2.7% according to the Atlanta Fed’s GDP now and the NY Fed’s Nowcast respectively.

For the UK, growth is expected to rise at a slower pace compared to other G7 economies. GDP growth in the UK is expected to pick up only slightly to 0.5% on the quarter.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)