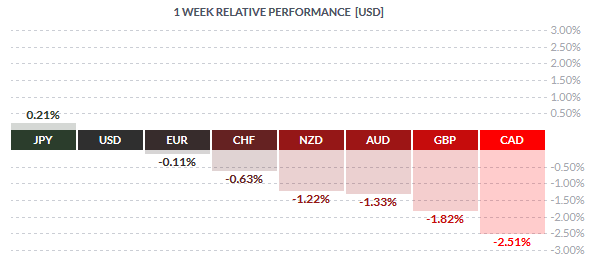

The Yen closed another week with gains, rising 0.21% for the week and on a month to date basis, the Yen is up 2.77%. The gains in the Yen are primarily driven by safe haven bets with lingering concerns from China’s economy and the stock market volatility. Following the Yen, the Euro has emerged strongly with 0.41% gains for the week. Data from the Eurozone has been mixed with inflation continuing to stay flat and industrial production remaining weak. However, the Euro managed to make steady gains on a modestly weaker Greenback.

Making up the tail end of the scale, the commodity risk currencies were weak with the Australian dollar taking a beating. The AUD is down -1.83% for the week followed by the Canadian dollar which fell -1.16% and the British Pound which is down -1.09% for the week. Over the week, the BoE left interest rates unchanged leaving the GBP on a bearish trend ahead of next week’s inflation and unemployment numbers.

Fundamentals for the Week 18/01 – 22/01

| Date | Time | Currency | Detail | Forecast | Previous |

| 18-Jan | 01:30 | AUD | MI Inflation Gauge m/m | 0.10% | |

| 02:30 | AUD | New Motor Vehicle Sales m/m | 1.00% | ||

| 18th-20th | CNY | Foreign Direct Investment ytd/y | 7.90% | ||

| 06:30 | JPY | Revised Industrial Production m/m | 1.40% | 1.40% | |

| JPY | Tertiary Industry Activity m/m | -0.60% | 0.90% | ||

| 19-Jan | 04:00 | CNY | GDP q/y | 6.90% | 6.90% |

| CNY | Industrial Production y/y | 6.00% | 6.20% | ||

| CNY | Fixed Asset Investment ytd/y | 10.20% | 10.20% | ||

| CNY | NBS Press Conference | ||||

| CNY | Retail Sales y/y | 11.30% | 11.20% | ||

| 09:00 | EUR | German Final CPI m/m | -0.10% | -0.10% | |

| 10:15 | CHF | PPI m/m | 0.20% | 0.40% | |

| 11:00 | EUR | Current Account | 19.3B | 20.4B | |

| 11:30 | GBP | CPI y/y | 0.10% | 0.10% | |

| GBP | PPI Input m/m | -1.40% | -1.60% | ||

| GBP | RPI y/y | 1.00% | 1.10% | ||

| GBP | Core CPI y/y | 1.20% | 1.20% | ||

| GBP | HPI y/y | 7.30% | 7.00% | ||

| GBP | PPI Output m/m | -0.20% | -0.20% | ||

| 12:00 | EUR | German ZEW Economic Sentiment | 8.2 | 16.1 | |

| EUR | Final CPI y/y | 0.20% | 0.20% | ||

| EUR | ZEW Economic Sentiment | 27.9 | 33.9 | ||

| EUR | Final Core CPI y/y | 0.90% | 0.90% | ||

| 15:30 | CAD | Foreign Securities Purchases | 12.1B | 22.1B | |

| Tentative | NZD | GDT Price Index | -1.60% | ||

| 17:00 | USD | NAHB Housing Market Index | 61 | 61 | |

| 23:00 | USD | TIC Long-Term Purchases | -16.6B | ||

| 23:45 | NZD | CPI q/q | -0.20% | 0.30% | |

| 20-Jan | 01:30 | AUD | Westpac Consumer Sentiment | -0.80% | |

| 09:00 | EUR | German PPI m/m | -0.30% | -0.20% | |

| 11:30 | GBP | Average Earnings Index 3m/y | 2.10% | 2.40% | |

| GBP | Claimant Count Change | 4.1K | 3.9K | ||

| GBP | Unemployment Rate | 5.20% | 5.20% | ||

| 12:00 | CHF | ZEW Economic Expectations | 16.6 | ||

| 15:30 | CAD | Manufacturing Sales m/m | -1.10% | ||

| CAD | Wholesale Sales m/m | -0.60% | |||

| USD | Building Permits | 1.20M | 1.28M | ||

| USD | CPI m/m | 0.00% | 0.00% | ||

| USD | Core CPI m/m | 0.20% | 0.20% | ||

| USD | Housing Starts | 1.19M | 1.17M | ||

| 17:00 | CAD | BOC Monetary Policy Report | |||

| CAD | BOC Rate Statement | ||||

| CAD | Overnight Rate | 0.25% | 0.50% | ||

| 17:30 | USD | Crude Oil Inventories | 0.2M | ||

| 18:15 | CAD | BOC Press Conference | |||

| 23:30 | NZD | Business NZ Manufacturing Index | 54.7 | ||

| 21-Jan | 02:00 | AUD | MI Inflation Expectations | 4.00% | |

| AUD | HIA New Home Sales m/m | -3.00% | |||

| 06:30 | JPY | All Industries Activity m/m | -0.70% | 1.00% | |

| 14:45 | EUR | Minimum Bid Rate | 0.05% | 0.05% | |

| 15:30 | EUR | ECB Press Conference | |||

| USD | Philly Fed Manufacturing Index | -3.1 | -5.9 | ||

| USD | Unemployment Claims | 281K | 284K | ||

| 17:00 | EUR | Consumer Confidence | -6 | -6 | |

| 22-Jan | 03:35 | JPY | Flash Manufacturing PMI | 52.8 | 52.6 |

| 10:00 | EUR | French Flash Manufacturing PMI | 51.6 | 51.4 | |

| EUR | French Flash Services PMI | 50.4 | 49.8 | ||

| 10:30 | EUR | German Flash Manufacturing PMI | 53 | 53.2 | |

| EUR | German Flash Services PMI | 55.6 | 56 | ||

| 11:00 | EUR | Flash Manufacturing PMI | 53 | 53.2 | |

| EUR | Flash Services PMI | 54.2 | 54.2 | ||

| 11:30 | GBP | Retail Sales m/m | -0.10% | 1.70% | |

| GBP | Public Sector Net Borrowing | 13.6B | |||

| 14:00 | GBP | MPC Member Cunliffe Speaks | |||

| 15:30 | CAD | Core CPI m/m | -0.30% | ||

| CAD | Core Retail Sales m/m | 0.00% | |||

| CAD | CPI m/m | -0.10% | |||

| CAD | Retail Sales m/m | 0.10% | |||

| 16:45 | USD | Flash Manufacturing PMI | 51.5 | 51.2 | |

| 17:00 | USD | Existing Home Sales | 5.21M | 4.76M | |

| USD | CB Leading Index m/m | -0.10% | 0.40% |

Time: GMT+2

Currencies/Events to Watch this Week

AUD: The week ahead for the Australian dollar is limited to second-tier data including MI inflation gauge and inflation expectations and new motor vehicle sales and new home sales reports. For the most part, the Aussie could remain under pressure from the markets as China reports some important numbers such as the GDP and industrial production. A miss on the estimates from China could potentially trigger another bout of selling in the markets.

NZD: While the Kiwi also remains susceptible to the risk sentiment from China’s GDP and other important data, the NZD will be looking at the quarterly inflation numbers due for release on 19th January. Expectations call for New Zealand inflation to dip -0.20% after holding steady at for the past two quarters. A dip on quarterly inflation could potentially set ahead expectations for further RBNZ rate cuts. Also during the week, the GDT price index is due for release.

JPY: There is not much of data to go by from Japan but as with the markets in general, the Yen’s direction could be defined by how the markets react to the data from China over the week. So far, the Yen has posted two straight weeks of gains against the US Dollar and another weak data set from China could simply trigger more declines with the Yen strengthening. On the flipside with the markets quite bearish, positive data from China could see the Yen ease back as markets attempt to recover lost ground.

EUR: The week ahead will be important for the single currency as German ZEW Economic sentiment and Eurozone final CPI is due for release. Expectations are for the headline Eurozone CPI to increase 0.20% while the Core CPI is expected to stay flat at 0.90%. Another weak reading could set the ECB on a dovish narrative as the Central Bank meets on Thursday, 21st January. After the December policy changes, the ECB could remain neutral but try to talk down the Euro. However, with the EURUSD staying largely flat since December, the ECB could remain a non-event at worst.

GBP: After posting strong losses over the past few weeks, the British Pound will be looking to the inflation numbers due on Tuesday. Expectations are for the CPI to stay flat at 0.10% while the Core CPI is expected to remain steady at 1.20%. Also later in the week, the UK unemployment data is due for release. The unemployment rate is expected to remain unchanged at 5.20% while the average earnings index which has gained importance in recent months is expected to rise at a slower pace of 2.10%. Winding up the week will be the UK retail sales numbers which are expected to show -0.10% decline down from -0.70% declines a month before.

CAD: The Bank of Canada takes center stage next week with market expectations divided. For the moment, the expectations are for the BoC to cut rates by 25bps to bring the benchmark overnight lending rates from 0.50% to 0.25%. The rate cut prospects are well priced in with the CAD losing out strongly to the Dollar. However, in the event of a surprise, the USDCAD could be looking at significant downside risks. Also during the week, the Canadian retail sales numbers are due following the monthly inflation report.

USD: The US markets will be looking at a holiday-shortened week with Monday closed on account of Martin Luther King Day. However, data picks up over the week with the monthly inflation numbers due for release. The headline monthly CPI is expected to stay flat at 0.0% while the Core CPI is also expected to stay put at 0.20%. The remainder of the week comes with the Philly Fed manufacturing Index and the weekly unemployment claims.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)