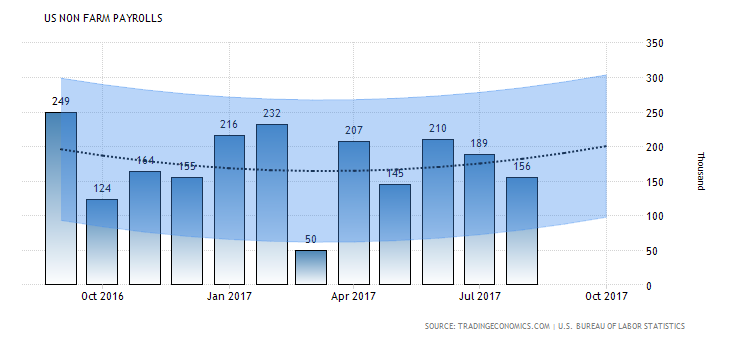

The September nonfarm payrolls data will be released today by the Bureau of Labor Statistics. According to the median estimates of economists polled, the US economy is expected to add just 88k jobs during the month of September.

The weak pace of job gains are attributed to the disruptions caused by the hurricanes Irma, Harvey, and Maria.

The weak print expected for September is however likely to be a temporary blip. The Fed already acknowledged the downside risks from the natural disasters, in its September FOMC meeting. As a result, the market reaction could be muted. However, some downside risks persist if the actual headline payrolls come out weaker than the estimates.

On the unemployment rate, the median estimates call for an unchanged print. The US official unemployment rate is expected to remain steady at 4.4%, unchanged from the previous month.

Wages are expected to be a bright spot with economists predicting a 0.3% increase in wages for September. This would show some strong acceleration from 0.1% increase registered in August.

Overall, the US labor market data is likely to fall in line with the prevailing trend, and even a worse than expected print on all fronts is unlikely to move the Fed much into postponing its rate hike plans for the fourth quarter.

Inflation is likely to dominate with recent reports suggesting that inflation in the US continues to remain sluggish.

Consumer spending in the US weakens in August

Last week, data showed that the Fed’s preferred gauge of inflation, the personal consumption expenditure or PCE price index rose just 0.2% in August on a month over month basis. Excluding the volatile food and energy prices, core PCE was seen rising 0.1% on the month. The data was weaker than the median estimates.

On a year over year basis, consumer prices were seen rising 1.4% while core PCE was up 1.3%, both of which are well below the Fed’s 2% inflation target rate. The Fed has signaled that it hopes to hike interest rates one more time by December.

However, for this to happen, inflation will need to show signs of firming in the coming three months. Other measures of inflation such as the headline CPI and the core CPI showed some optimism as both measures of inflation was seen rising in August. But most of the gains came on account of an increase in shelter costs.

Despite the recent upward revision to the GDP figures in the second quarter, growth is forecast to slow to an average of 2.1% in the third quarter. The Atlanta Fed’s GDPNow model currently puts the third quarter GDP expectations at around 2.3%.

Markets likely to look through weak payrolls print

Despite the weak estimates on the payrolls and the potential for a weaker than expected payrolls data, the impact could be limited. Previous examples such as the aftermath of Hurricane Katrina showed that while the data from BLS initially showed a weak print, it was later revised higher.

With the Fed also signaling that it will look through the short-term factors, it is evident that any weakness in the payrolls could be attributed to the hurricanes.

It will be important for the US dollar however as that leaves just three more payrolls report for the Fed to assess before it decides whether or not to hike interest rates.

In an ideal scenario, a pickup in wages alongside higher inflation albeit short-lived could help make the case for Fed officials to proceed as planned. This could, however, see only some short-term strength in the US dollar.