The markets will be moving into the final trading week of the month of March, and the economic calendar is somewhat light, which increases the risk sentiment based on politics.

Some of the important economic events that stand out this week include the GDP figures from the U.S., UK, and Canada while preliminary PMI’s and inflation figures will be coming out from the Eurozone. Here are this week’s key market events for the currencies.

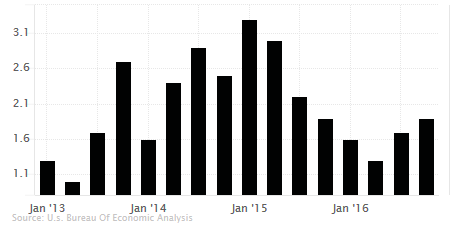

U.S. final revised GDP, Q4 2016 to show 2.0% increase

Data from the U.S. next week will see the final GDP figures for the fourth quarter of 2016. Economists polled are forecasting a 2.0% increase in the GDP for the final revision, which is slightly higher than the 1.9% print seen as of the second revision. The final GDP price index is also expected to remain unchanged at 2.0%, same as the month before.

The U.S. economy was seen expanding at a pace of 3.5% in the third quarter of 2016, and it was the best growth rate seen in nearly two years. The U.S. Federal Reserve is projecting the GDP to expand at a rate of 2% in the near term.

Besides the GDP figures, the weekly U.S. unemployment claims will also be coming out this week. Later in the day, the personal income and spending details will also be released.

Forecasts point to a 1.2% increase in the core PCE on a quarterly basis, rising at the same pace as the previous quarter while personal consumption is projected to rise 3% quarter over quarter.

On Friday, the PCE data will be coming out which is the Fed’s preferred gauge of inflation. Core PCE is expected to rise 0.2% on a month over month basis which is expected to push the annual core PCE rate to 1.7%. Personal spending and Chicago PMI numbers make up for the remainder of the economic releases for the remainder of the week.

German Ifo business climate and flash CPI

It is a rather slow week from the eurozone but the week starts off with the German Ifo business climate. Business confidence in Germany has improved steadily in February rising on the back of the ECB’s projection that economic growth was strengthening in the eurozone.

The Ifo business climate in Germany registered a print of 111.0 in February following a revised 109.9 print in January. The current economic conditions also accelerated to 118.4 from 116.9 in January with future expectations rising to 104.

Economic data from Germany has been consistent and steadily rising as the economy reaffirmed its pole position as the leading economy in the EU. Growth is expected to continue despite the political turbulence from the France and German elections due later. The Ifo business climate data is forecast to show a modest improvement from 111.0 in February to 111.2 in March.

Other economic releases during the week also include the preliminary inflation figures. Following the rise to 2.0% inflation rate, data this week forecasts headline inflation to rise at a slower pace of just 1.8%, while core CPI is expected to rise at a slower pace of 0.8%.

German retail sales and French consumer spending numbers will be making up for other economic releases from the eurozone during the week.

UK to trigger Article 50 on March 29th

Amid a rather slow week in the UK, the focus will be on Wednesday’s official announcement on the Article 50. Coming close to a year since the UK voted to leave the EU, the Brexit bill which was approved by the UK Parliament and passed as law the week before will be used to formally start the exit negotiations with the EU.

While politics will clearly overshadow the economic calendar this week, the final revision to the GDP for the fourth quarter of 2016 will be released this week. Economists polled expect to see the final GDP print remain unchanged at 0.7%, although the index of services is expected to be revised down from 0.8% to 0.7% while the revised business investment is forecast to show a 1.0% decline.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)