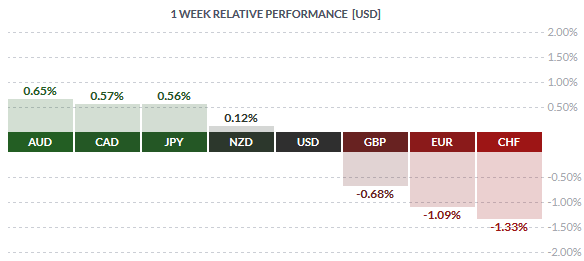

The US Dollar saw a mixed week, stronger against the Euro and the British Pound while the commodity risk currencies posted gains. The Australian dollar closed the week with 0.65% gains against the Greenback while the Canadian dollar gained 0.57%. The gains in the commodity risk currencies came on a strong rally in Oil prices and Gold which was already trending stronger. The US Dollar opened the week on a positive week but soon eased back on the rally following the FOMC meeting minutes. Friday’s consumer inflation data posted strong numbers helping the dollar to stabilize. The Yen continued to trade firm across the board, indicating a slight hint of risk aversion still in play.

The week ahead will see data from the US which includes the durable goods orders and the second estimate GDP data for the fourth quarter. From the Eurozone, data is limited to flash PMI’s and inflation numbers. The British Pound remains susceptible to the ongoing negotiation between the UK and its EU partners, as the currency turned weak on Friday despite strong retail sales numbers.

Fundamentals for the Week 22/02 – 19/02

| Date | Time | Currency | Detail | Forecast | Previous |

| 22-Feb | 00:10 | AUD | RBA Assist Gov Debelle Speaks | ||

| 04:00 | JPY | Flash Manufacturing PMI | 52 | 52.3 | |

| NZD | Credit Card Spending y/y | 7.40% | |||

| 10:00 | EUR | French Flash Manufacturing PMI | 49.9 | 50 | |

| EUR | French Flash Services PMI | 50.4 | 50.3 | ||

| 10:15 | CHF | PPI m/m | -0.20% | -0.40% | |

| 10:30 | EUR | German Flash Manufacturing PMI | 52.1 | 52.3 | |

| EUR | German Flash Services PMI | 54.8 | 55 | ||

| 11:00 | EUR | Flash Manufacturing PMI | 52.1 | 52.3 | |

| EUR | Flash Services PMI | 53.4 | 53.6 | ||

| 13:00 | GBP | CBI Industrial Order Expectations | -12 | -15 | |

| 16:45 | USD | Flash Manufacturing PMI | 52.5 | 52.4 | |

| 17:30 | AUD | CB Leading Index m/m | 0.30% | ||

| 23-Feb | 09:00 | EUR | German Final GDP q/q | 0.30% | 0.30% |

| 11:00 | EUR | German Ifo Business Climate | 107 | 107.3 | |

| 13:15 | CHF | SNB Chairman Jordan Speaks | |||

| USD | S&P/CS Composite-20 HPI y/y | 5.60% | 5.80% | ||

| 17:00 | USD | CB Consumer Confidence | 97.6 | 98.1 | |

| USD | Existing Home Sales | 5.42M | 5.46M | ||

| USD | Richmond Manufacturing Index | 2 | 2 | ||

| 24-Feb | 01:50 | JPY | SPPI y/y | 0.30% | 0.40% |

| 02:30 | AUD | Construction Work Done q/q | -2.10% | -3.60% | |

| AUD | Wage Price Index q/q | 0.60% | 0.60% | ||

| 13:00 | GBP | CBI Realized Sales | 16 | 16 | |

| 16:45 | USD | Flash Services PMI | 53.6 | 53.2 | |

| 17:00 | USD | New Home Sales | 522K | 544K | |

| 17:30 | USD | Crude Oil Inventories | 2.1M | ||

| 19:50 | CAD | Gov Council Member Schembri Speaks | |||

| 23:45 | NZD | Visitor Arrivals m/m | -1.30% | ||

| 25-Feb | 02:00 | USD | FOMC Member Bullard Speaks | ||

| 02:30 | AUD | Private Capital Expenditure q/q | -3.00% | -9.20% | |

| 09:00 | EUR | GfK German Consumer Climate | 9.2 | 9.4 | |

| EUR | Private Loans y/y | 1.50% | 1.40% | ||

| 11:30 | GBP | Second Estimate GDP q/q | 0.50% | 0.50% | |

| GBP | Prelim Business Investment q/q | 0.60% | 2.20% | ||

| GBP | Index of Services 3m/3m | 0.70% | 0.60% | ||

| 12:00 | EUR | Final CPI y/y | 0.40% | 0.40% | |

| EUR | Final Core CPI y/y | 1.00% | 1.00% | ||

| EUR | Italian Retail Sales m/m | 0.50% | 0.30% | ||

| 15:30 | CAD | Corporate Profits q/q | -5.40% | ||

| USD | Core Durable Goods Orders m/m | 0.10% | -1.00% | ||

| USD | Unemployment Claims | 271K | 262K | ||

| USD | Durable Goods Orders m/m | 2.60% | -5.00% | ||

| 16:00 | USD | HPI m/m | 0.50% | 0.50% | |

| 26-Feb | 07:00 | JPY | BOJ Core CPI y/y | 1.20% | 1.30% |

| All Day | EUR | German Prelim CPI m/m | 0.60% | -0.80% | |

| 09:45 | EUR | French Consumer Spending m/m | 0.60% | 0.70% | |

| 10:00 | EUR | Spanish Flash CPI y/y | -0.50% | -0.30% | |

| 15:30 | USD | Prelim GDP q/q | 0.50% | 0.70% | |

| USD | Core PCE Price Index m/m | 0.10% | 0.00% | ||

| USD | Goods Trade Balance | -61.1B | -61.5B | ||

| USD | Personal Spending m/m | 0.30% | 0.00% | ||

| USD | Personal Income m/m | 0.40% | 0.30% | ||

| USD | Prelim GDP Price Index q/q | 0.80% | 0.80% | ||

| 17:00 | USD | Revised UoM Consumer Sentiment | 91.1 | 90.7 | |

| USD | Revised UoM Inflation Expectations | 2.50% |

Time: GMT+2

Currencies/Events to Watch this Week

AUD: Economic data from Australia this week is limited with data mostly on construction work done and the quarterly wage price index. The Aussie is likely to remain muted for the most part of the week, following last week’s comments from RBA economist who noted the downside risks to the AUD and that $0.65 was a more preferred exchange rate for the Australian Dollar.

JPY: The focus for the Yen this week will be the Bank of Japan’s inflation data. Expectations are for the core CPI to rise at a slower pace of 1.20%. The BoJ has a target inflation rate of 2.0% and is under pressure to do more to stoke inflation. In January, the BoJ cut interest rates to the negative which had little to no effect as far as the Yen’s exchange rate was concerned. Another weak reading in inflation combined with a contraction in the fourth quarter of 2015 could clearly put the BoJ officials on the edge.

EUR: The week ahead is marked with flash PMI data but more importantly, focus turns to the Eurozone inflation numbers. Taking a cue from inflation data across other economies, there is a possibility that Eurozone inflation might have either risen strongly or stayed flat/unchanged. The Euro is likely to remain flat for the most part of the week, taking a cue mostly from the US Dollar.

GBP: The UK’s second estimates for the fourth quarter GDP is due this week with expectations staying flat at 0.50%. However, more importantly the British Pound comes at risk as EU and UK leaders negotiate a deal in order for the UK to remain in the EU. On Friday, the Pound fell sharply as negotiations continued with no clear break through.

CHF: The Swiss Franc comes under risk this week as SNB Chairman; Thomas Jordan is due to speak. The SNB has not ruled out further rate cuts and it is likely that the SNB would prefer to wait and watch on how the ECB decides in March. Regardless, dovish comments from the SNB Chairman could pose a significant risk to the CHF crosses this week.

USD: Data from the US this week includes the existing and new home sales data. However, focus will likely be on the durable goods orders numbers followed by the second revision to the fourth quarter GDP, which is estimated to be weaker at 0.50% against initial estimates of 0.70%. While the markets are tuned in for a weak GDP release, any surprise to the estimates could reflect into the US Dollar’s direction in the near term.