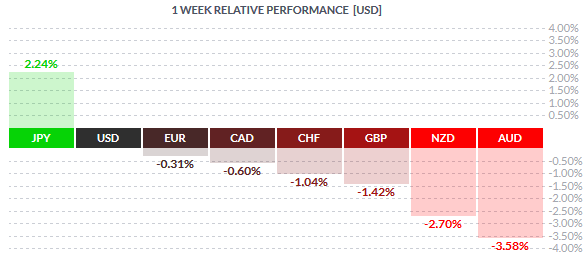

The Japanese Yen maintained its top position for the third consecutive week gaining 2.24% for the week. Market uncertainty surrounding the US Fed rate hikes as well as the China economic slowdown continues to play out on investors minds. The Swiss Franc gave up its gains has remains weaker against the stronger currencies including the Yen, US Dollar, the Euro and the Canadian Dollar. Last week’s important data included the US Non farm payrolls which despite falling short of estimates managed to pull down the US unemployment rate lower to 5.1%.

The commodity currencies, the Aussie and the Kiwi made up the tail end of the list, losing -3.58% and -2.7% respectively indicating that the market was in no mood to take on risk. A strong rebound in the US Dollar led to most of the currencies trading weaker with the exception of the safe haven Yen.

Fundamentals for the Week 07/09 – 11/09

| Date | Time | Currency | Detail | Forecast | Previous |

| 07-Sep | 02:30 | AUD | AIG Construction Index | 47.1 | |

| 04:30 | AUD | ANZ Job Advertisements m/m | -0.40% | ||

| 08:00 | JPY | Leading Indicators | 104.90% | 106.50% | |

| 09:00 | EUR | German Industrial Production m/m | 1.20% | -1.40% | |

| 10:00 | CHF | Foreign Currency Reserves | 532B | ||

| 11:30 | EUR | Sentix Investor Confidence | 16.2 | 18.4 | |

| 08-Sep | 01:45 | NZD | Manufacturing Sales q/q | -2.80% | |

| 02:01 | GBP | BRC Retail Sales Monitor y/y | 1.20% | ||

| 02:50 | JPY | Current Account | 1.25T | 1.30T | |

| JPY | Final GDP q/q | -0.40% | -0.40% | ||

| JPY | Bank Lending y/y | 2.60% | |||

| JPY | Final GDP Price Index y/y | 1.60% | 1.60% | ||

| 04:30 | AUD | NAB Business Confidence | 4 | ||

| 06:45 | JPY | 30-y Bond Auction | 1.44|3.3 | ||

| Tentative | CNY | Trade Balance | 48.6B | 43.0B | |

| 08:00 | JPY | Economy Watchers Sentiment | 52.1 | 51.6 | |

| 08:45 | CHF | Unemployment Rate | 3.30% | 3.30% | |

| 09:00 | EUR | German Trade Balance | 21.8B | 22.0B | |

| 09:45 | EUR | French Gov Budget Balance | -58.5B | ||

| EUR | French Trade Balance | -3.2B | -2.7B | ||

| 8th-10th | GBP | Halifax HPI m/m | 0.50% | -0.60% | |

| 12:00 | EUR | Revised GDP q/q | 0.30% | 0.30% | |

| Tentative | GBP | 30-y Bond Auction | 2.73|1.9 | ||

| 13:00 | USD | NFIB Small Business Index | 96 | 95.4 | |

| 17:00 | USD | Labor Market Conditions Index m/m | 1.1 | ||

| 22:00 | USD | Consumer Credit m/m | 18.4B | 20.7B | |

| 09-Feb | 02:01 | GBP | BRC Shop Price Index y/y | -1.40% | |

| 02:50 | JPY | M2 Money Stock y/y | 4.10% | 4.10% | |

| 03:30 | AUD | Westpac Consumer Sentiment | 7.80% | ||

| 04:30 | AUD | Home Loans m/m | 0.80% | 4.40% | |

| 05:00 | AUD | RBA Deputy Gov Lowe Speaks | |||

| 08:00 | JPY | Consumer Confidence | 40.6 | 40.3 | |

| 09:00 | JPY | Prelim Machine Tool Orders y/y | 1.70% | ||

| 11:30 | GBP | Manufacturing Production m/m | 0.20% | 0.20% | |

| GBP | Trade Balance | -9.5B | -9.2B | ||

| GBP | Industrial Production m/m | 0.10% | -0.40% | ||

| 12:00 | AUD | RBA Assist Gov Debelle Speaks | |||

| Tentative | EUR | German 10-y Bond Auction | 0.61|1.3 | ||

| 15:15 | CAD | Housing Starts | 194K | 193K | |

| 15:30 | CAD | Building Permits m/m | 14.80% | ||

| 17:00 | CAD | BOC Rate Statement | |||

| CAD | Overnight Rate | 0.50% | 0.50% | ||

| GBP | NIESR GDP Estimate | 0.70% | |||

| USD | JOLTS Job Openings | 5.30M | 5.25M | ||

| 10-Sep | 00:00 | NZD | Official Cash Rate | 2.75% | 3.00% |

| NZD | RBNZ Rate Statement | ||||

| NZD | RBNZ Monetary Policy Statement | ||||

| 00:05 | NZD | RBNZ Press Conference | |||

| 02:01 | GBP | RICS House Price Balance | 46% | 44% | |

| 02:50 | JPY | Core Machinery Orders m/m | 3.40% | -7.90% | |

| JPY | PPI y/y | -3.20% | -3.00% | ||

| 04:00 | AUD | MI Inflation Expectations | 3.70% | ||

| 04:30 | AUD | Employment Change | 5.2K | 38.5K | |

| AUD | Unemployment Rate | 6.20% | 6.30% | ||

| CNY | CPI y/y | 1.90% | 1.60% | ||

| CNY | PPI y/y | -5.60% | -5.40% | ||

| 08:30 | EUR | French Final Non-Farm Payrolls q/q | 0.20% | 0.20% | |

| 09:45 | EUR | French Industrial Production m/m | 0.30% | -0.10% | |

| 10th-14th | CNY | M2 Money Supply y/y | 13.30% | 13.30% | |

| 10th-14th | CNY | New Loans | 850B | 1480B | |

| 14:00 | GBP | MPC Official Bank Rate Votes | 1-0-8 | 1-0-8 | |

| GBP | Official Bank Rate | 0.50% | 0.50% | ||

| GBP | Asset Purchase Facility | 375B | 375B | ||

| GBP | MPC Asset Purchase Facility Votes | 0-0-9 | 0-0-9 | ||

| Tentative | GBP | MPC Rate Statement | |||

| 15:30 | CAD | NHPI m/m | 0.20% | 0.30% | |

| CAD | Capacity Utilization Rate | 82.70% | |||

| USD | Unemployment Claims | 279K | 282K | ||

| USD | Import Prices m/m | -1.70% | -0.90% | ||

| 17:00 | USD | Wholesale Inventories m/m | 0.20% | 0.90% | |

| 17:30 | USD | Natural Gas Storage | 94B | ||

| 18:00 | USD | Crude Oil Inventories | 4.7M | ||

| 11-Sep | 01:30 | NZD | Business NZ Manufacturing Index | 53.5 | |

| 01:45 | NZD | FPI m/m | 0.60% | ||

| 02:50 | JPY | BSI Manufacturing Index | -6 | ||

| 09:00 | EUR | German Final CPI m/m | 0.00% | 0.00% | |

| EUR | German WPI m/m | 0.20% | 0.10% | ||

| 11:00 | EUR | Italian Industrial Production m/m | 0.90% | -1.10% | |

| 11:30 | GBP | Construction Output m/m | 0.50% | 0.90% | |

| GBP | Consumer Inflation Expectations | 2.20% | |||

| Day 1 | EUR | ECOFIN Meetings | |||

| 15:30 | USD | PPI m/m | -0.10% | 0.20% | |

| USD | Core PPI m/m | 0.10% | 0.30% | ||

| 17:00 | USD | Prelim UoM Consumer Sentiment | 91.8 | 91.9 | |

| USD | Prelim UoM Inflation Expectations | 2.80% | |||

| 21:00 | USD | Federal Budget Balance | -83.5B | -149.2B |

Currencies/Events to Watch this Week

Australia Jobs Report: A relatively quiet week for the Aussie, Thursday will see the monthly jobs report from Australia. The currency has declined considerably in the past few weeks as economic data continues to fall below estimates. The monthly jobs numbers for Australia point to a median forecast estimates of the unemployment rate falling back to 6.2% after rising to 6.3% a month before. On the employment change, it is expected that the Australian economy added 5.2k jobs, down from 38.5k a month ago.

BoC Rate statement: The Canadian economy has so far managed to stay within the BoC’s expectations in terms of inflation and GDP. The most recent jobs report from Canada also showed a bit of promise despite the unemployment rate rising to 7%. The Bank of Canada will meet this Thursday and is expected to keep interest rates unchanged at 0.5%. An unchanged interest rate decision could see some bounce in the Canadian dollar in the near term.

China Inflation: China, which was closed for most of last week is back in business this week and the yearly CPI data is due for release on Thursday. Expectations are riding high for the inflation to have risen to 1.9%, against previous month’s modest rise to 1.6%. A miss on the estimates could potentially see the equity markets come under pressure again.

Eurozone Revised GDP: The quarterly revised GDP for the Eurozone is due for release on Tuesday with expectations of no change to the GDP which stands at 0.3% presently. Besides the GDP data there are no major market moving events from the Eurozone due this week.

BoE Meeting: The Bank of England meets on Thursday to discuss its monetary policy. While no change is expected, the markets will be eager to see the MPC vote count, which as of last month showed only one dissenter as the annual CPI in the UK started to show signs of bottoming. The British Pound has declined considerably and any shift to the MPC votes could see the Cable suffer larger setbacks.

Japan GDP: The final quarterly revised GDP numbers from Japan is due on Tuesday with expectations of a decline to -0.4%, unchanged from the previous release. Besides the GDP data there are no other major market moving events scheduled from Japan for the week.

RBNZ Monetary Policy: The Reserve Bank of New Zealand meets this week on Thursday for its monetary policy meeting. Expectations are for the RBNZ to cut rates by 25bps in light of subdued economic growth from the country. The rate cut would be a straight back to back cut for the RBNZ. In its previous monetary policy meeting, the Kiwi reacted bullishly and we could probably expect to see the same reaction at this meeting as well.

US PPI and UoM Inflation expectations: It will be a quiet and a short week for the US Markets, which are closed on Monday due to Labour Day holiday. The week is marked with only minor releases with the most important of all due on Friday. The University of Michigan’s inflation expectations will be one to watch out for. UoM’s inflation expectation stands at 2.8% currently.