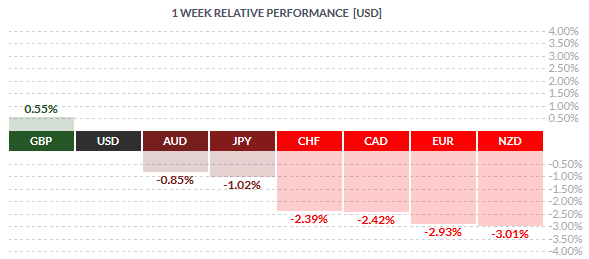

The British Pound Sterling emerged on the top last week, gaining 0.55% for the week. Despite a few hiccups in the economic data such as weaker than expected average earnings index and a relatively flat CPI numbers, the GBP got a boost as the BoE Governor, Mark Carney, in his speech last week noted that the time for lower interest rates was ending, signaling a shift in the BoE’s policy towards hiking interest rates. The markets took this as a signal that the BoE would start to hike rates in the coming months. Currently, the markets are pricing in a rate hike in the first half of 2016. The US Dollar came a close second and again it was largely due to Janet Yellen who testified to the Senate Banking Committee, where she reiterated the Fed’s optimistic view for rate hikes this year.

The New Zealand Dollar was the weakest performing currency last week losing over -3%. The Kiwi was under pressure as the CPI data failed to rise as expected and the Global dairy trade index continued to post in the negative. The weak economic data alongside a lackluster inflation numbers is likely to keep the NZD under pressure as the RBNZ could potentially cut rates even further. Overall, last week saw a return to the fundamentals as monetary policy divergence took over the markets as the Greek headline started to recede.

Fundamentals for the Week July 20 – 24

| Date | Time | Currency | Detail | Forecast | Previous |

| 20-Jul | 02:01 | GBP | Rightmove HPI m/m | 3.00% | |

| All Day | JPY | Bank Holiday | |||

| 09:00 | EUR | German PPI m/m | 0.00% | 0.00% | |

| 11:00 | EUR | Current Account | 23.1B | 22.3B | |

| 13:00 | EUR | German Buba Monthly Report | |||

| 15:30 | CAD | Wholesale Sales m/m | 0.10% | 1.90% | |

| 21-Jul | 01:45 | NZD | Visitor Arrivals m/m | 0.10% | |

| 04:30 | AUD | Monetary Policy Meeting Minutes | |||

| 06:00 | NZD | Credit Card Spending y/y | 7.10% | ||

| 21st-24th | CNY | Foreign Direct Investment ytd/y | 10.10% | ||

| 09:00 | CHF | Trade Balance | 2.78B | 3.43B | |

| 21st-24th | CNY | New Loans | 1050B | 901B | |

| 11:30 | GBP | Public Sector Net Borrowing | 8.6B | 9.4B | |

| 22-Jul | 03:30 | AUD | MI Leading Index m/m | -0.10% | |

| 04:30 | AUD | CPI q/q | 0.80% | 0.20% | |

| AUD | Trimmed Mean CPI q/q | 0.60% | 0.60% | ||

| 06:05 | AUD | RBA Gov Stevens Speaks | |||

| 07:30 | JPY | All Industries Activity m/m | -0.50% | 0.10% | |

| 11:30 | GBP | MPC Official Bank Rate Votes | 0-0-9 | 0-0-9 | |

| GBP | MPC Asset Purchase Facility Votes | 0-0-9 | 0-0-9 | ||

| 12:00 | EUR | Italian Retail Sales m/m | 0.20% | 0.70% | |

| 16:00 | USD | HPI m/m | 0.50% | 0.30% | |

| 17:00 | USD | Existing Home Sales | 5.40M | 5.35M | |

| 17:30 | USD | Crude Oil Inventories | -4.3M | ||

| 23-Jul | 00:00 | NZD | Official Cash Rate | 3.25% | 3.25% |

| NZD | RBNZ Rate Statement | ||||

| 02:50 | JPY | Trade Balance | -0.25T | -0.18T | |

| 05:00 | CNY | CB Leading Index m/m | 1.10% | ||

| 10:00 | EUR | Spanish Unemployment Rate | 22.90% | 23.80% | |

| 11:30 | GBP | Retail Sales m/m | 0.40% | 0.20% | |

| GBP | BBA Mortgage Approvals | 43.5K | 42.5K | ||

| 15:30 | CAD | Core Retail Sales m/m | 0.70% | -0.60% | |

| CAD | Retail Sales m/m | 0.40% | -0.10% | ||

| USD | Unemployment Claims | 285K | 281K | ||

| 17:00 | EUR | Consumer Confidence | -6 | -6 | |

| USD | CB Leading Index m/m | 0.10% | 0.70% | ||

| 17:30 | USD | Natural Gas Storage | 99B | ||

| 24-Jul | 01:45 | NZD | Trade Balance | 100M | 350M |

| 04:35 | JPY | Flash Manufacturing PMI | 50.5 | 50.1 | |

| 04:45 | CNY | Markit Flash Manufacturing PMI | 49.8 | 49.4 | |

| 10:00 | EUR | French Flash Manufacturing PMI | 51.1 | 50.7 | |

| EUR | French Flash Services PMI | 53.9 | 54.1 | ||

| 10:30 | EUR | German Flash Manufacturing PMI | 52.1 | 51.9 | |

| EUR | German Flash Services PMI | 54.1 | 53.8 | ||

| 11:00 | EUR | Flash Manufacturing PMI | 52.5 | 52.5 | |

| EUR | Flash Services PMI | 54.2 | 54.4 | ||

| 16:00 | EUR | Belgian NBB Business Climate | -4 | -3.9 | |

| 16:45 | USD | Flash Manufacturing PMI | 53.7 | 53.6 | |

| 17:00 | USD | New Home Sales | 543K | 546K |

Currencies/Events to Watch this Week

RBA Monetary Policy Minutes: The RBA will be releasing its monetary policy minutes this week as market participants look for clues into the various board members’ view of the Australian economy. Although the RBA left rates unchanged, the minutes could potentially reveal the future course of action. Also on the tap will be the quarterly CPI data from Australia, which is expected to rise to 0.8% for the quarter, after a soft print at 0.2% a quarter before.

Canada Sales: The week ahead is quiet for the Canadian dollar which weakened significantly as a result of a rate cut from the BoC last week. The week ahead will see the wholesale sales and retail sales numbers from Canada. It is expected that the retail sales for the month will rise 0.7% on the core and 0.4% on the headline. A miss of estimates is likely to see the Canadian dollar weaken even more.

Europe PMI’s: The week ahead will see quite a bit of data from the Eurozone including flash services and manufacturing PMI data. For the Eurozone the markets expect to see a flat reading. With Greece talks now showing signs of progress as the government managed to quickly pass the new reforms bill, the onus is on the regional Eurozone parliaments that are expected to pass the legislation. We already saw the Euro weaken last week after the fears of a Grexit dissipated, thus showing the markets returning back to the fundamentals.

BoE Minutes: The markets will be keen to see how the BoE members voted at its last policy setting meeting. With hawkish comments from BoE’s Carney, a change in the voting structure which currently sees all members unanimous to keeping policy unchanged could pose significant upside risks for the British Pound. This week will also see the UK retail sales data, which is expected to stabilize to 0.4% after posting a weak gain of 0.2% last month.

RBNZ Monetary Policy: Will the RBNZ cut rates yet again or will they put policy on hold until more data comes through for scrutiny? The markets no matter what are bearish on the Kiwi Dollar and with the recent quarterly CPI showing no major signs of a rebound; it would be a close call. Expectations, heading into the RBNZ policy meeting are for the New Zealand Central Bank to leave rates unchanged at 3.25%.

Slow week for the Greenback: There are no major market moving economic events for the week ahead from the US with only the existing home sales, new home sales and flash manufacturing data on the tap. The Greenback is likely to continue to drift higher from last week.