Summary:

- Eurozone flash GDP estimates show economic activity expanded 0.6% on the quarter in Q3 2017

- Second quarter GDP was revised higher to 0.7% from 0.6%

- Inflation weakened in October as flash inflation data showed core CPI rising 0.9% and headline CPI rising 1.4%

- December ECB meeting will see release of the economic projections

- Inflation downgrades could be possible if consumer prices remain muted in the next month or two

- Overall activity in the Eurozone suggests ECB’s view on extending QE until September 2018

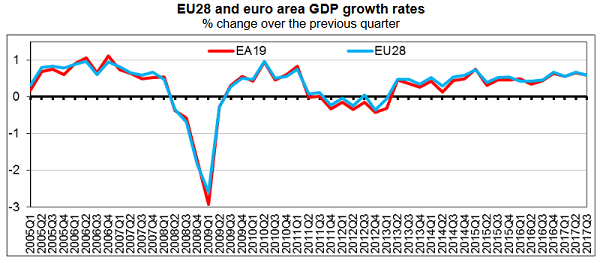

Eurozone Q3 GDP rises 0.6%

The preliminary estimates for the third quarter GDP from the Eurozone released last week showed that the real GDP rose 0.6% on a quarterly basis. The third quarter GDP slowed rather marginally compared to the revised 0.7% quarterly GDP growth in the second quarter.

Further data is expected which will show the expenditure components which could provide key insights into the GDP data. However, domestic demand is expected to stay robust underlining the solid growth momentum.

On a regional basis, France and Spain GDP numbers released showed that real GDP rose 0.5% and 0.8% respectively during the quarter. The data suggested that annual GDP growth in France was in line with government estimates at 1.8%.

The leading indicators in the euro area such as the PMI activity showed that overall economic growth remains consistent with the preliminary GDP data although growth is expected to marginally fall towards the end of this quarter.

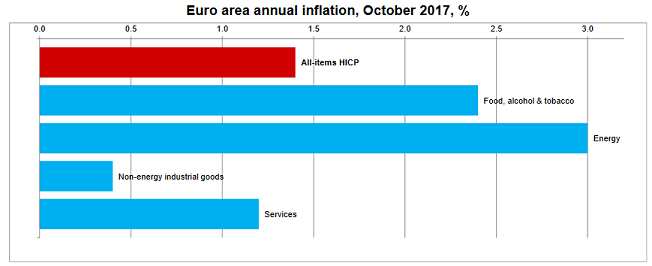

Inflation weakens in October

On the inflation front, the latest flash inflation figures showed that consumer prices eased during the month of October. Core inflation rate posted a large drop, rising just 0.9% on an annual basis for the period ending October.

This was the annual low in core inflation in May this year. Although the ECB does not look at the core inflation data, this is expected to be a significant component that can signal the underlying price pressures.

Headline consumer prices also eased, rising just 1.4% on a year over year basis. This was slower than the September inflation figures which showed a 1.1% increase on the core inflation and 1.5% increase on the headline figures.

The decline in the inflation numbers comes due to a drop in the energy prices. This is expected to continue into the following months as well. Although details remain scarce for the moment, services inflation was seen to be particularly affected. This came due to the temporary factors from the regional inflation numbers. Germany and Italy inflation was weaker.

Despite the weaker than expected inflation figures, consumer prices in the eurozone are expected to pick up on a gradual basis. This falls in line with the ECB’s decision to taper its QE purchases but extending it for nine months starting January 2018.

In December, the ECB’s meeting will be publishing the staff economic projections. If consumer prices fail to stabilize by November, we could expect to see inflation numbers being downgraded. This could be a disappointing fact for the ECB’s governing council despite a pick-up in economic activity and employment figures.

EU Commission Economic Forecasts

Looking ahead, the EU Commission will be releasing the economic forecasts. The previous report was released in May. Back then, the EU commission raised the growth forecasts noting that economic activity would increase during the year but at the same time forecasted that inflation could be weaker.

The EU commission projected GDP to rise 1.7% this year and 1.8% next year which was higher than its previous estimates. However, inflation figures were lowered to show a 1.5% increase in consumer prices which is most likely to be missed. Inflation for next year was forecast to slow to 1.3%.

The revised estimates could be coming out lower. However, within the larger context, this remains supportive of the fact that the ECB’s decision to extend QE by nine months was probably the right choice.