The week ahead will be marked by central bank meetings that include the BoC, the Swedish Riksbank, and the ECB. The ECB’s meeting will, however, dominate the wires. On the economic front, the US and the UK’s advance GDP reports will be coming out alongside the quarterly inflation data from Australia.

Here’s a quick recap into this week’s economic calendar for the currency markets.

ECB Tapering Announcement

The ECB’s meeting due this Thursday is expected to make headlines as the markets prepare for the announcement they have been eagerly anticipating for a while now. Following the September ECB meeting, the decision to taper (or not) was kicked down the road to the October monetary policy meeting.

The central bank is expected to announce a 20or 30 billion euro tapering to its quantitative easing program. Starting January 2018, this will bring the ECB’s bond purchases to half, if not more, and the second tapering since it first launched the QE program in January 2015 with 80 billion euro.

Amid widespread pickup in the economy, the markets have been expecting the tapering for quite a while. However, the ECB officials have remained cautious. Even just last week, some officials said that the pace of tightening would be very gradual. Officials said that there was still some monetary policy accommodation required.

Inflation was seen staying stable at 1.5% in September while core CPI was steady at 1.1% during the month. However, according to previous ECB estimates, inflation was expected to slow in the months ahead and especially early next year.

The markets are likely to remain volatile, and it all comes down to how Draghi will build the expectations. Hawkish comments on the monetary policy could potentially reinforce expectations of further tightening and could risk sending the euro higher.

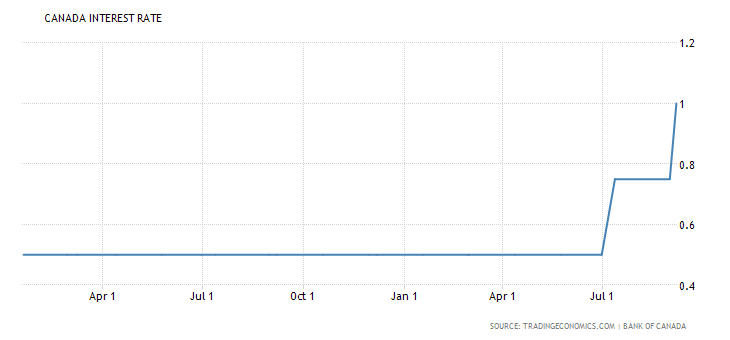

BoC expected to stay on the sidelines

The Bank of Canada will also be holding its monetary policy meeting this week on Wednesday. The BoC’s overnight rate is expected to remain unchanged at 1.0%. This comes after the BoC surprised the markets with two back to back rate hikes in the previous months.

Although the expectations call for no changes to interest rates this week, the BoC is still widely tipped to push with one more rate hike by the end of the year. However, recent developments, including the uncertainty surrounding the NAFTA trade agreement is expected to put the BoC in a wait and watch mode.

Furthermore, the BoC is said to hold back and wait for the Federal Reserve to hike interest rates in December. For the next year, expectations are very hawkish from the BoC which is expected to push rates to 1.75% by the end of 2018. This refers to three quarter basis point rate hikes for next year.

Although the GDP in recent months was seen to be slowing recent forecasts painted an optimistic picture for the exporters in Canada with growth pickup likely to see the momentum picking up the pace as far as the economic growth in concerned.

Advance GDP numbers from the US and the UK

This week will also see the advance GDP data coming out from the United States and the UK. For the US economists polled are forecasting a third-quarter GDP to rise 2.5% on an annualized basis.

This is somewhat slower compared to the 3.1% increase seen in the second quarter. The impact of the hurricanes is expected to play a role in the economic expansion during the period.

For the UK, the forecasts remain bleak with estimates putting a 0.3% increase on the quarter ending September. This would mark a second consecutive quarter of a 0.3% expansion in the economy. However, the downside risks loom for the UK’s economy. Unless the data posts a surprise, the markets will be digesting the impact of weaker GDP growth as the BoE prepares to hike rates.