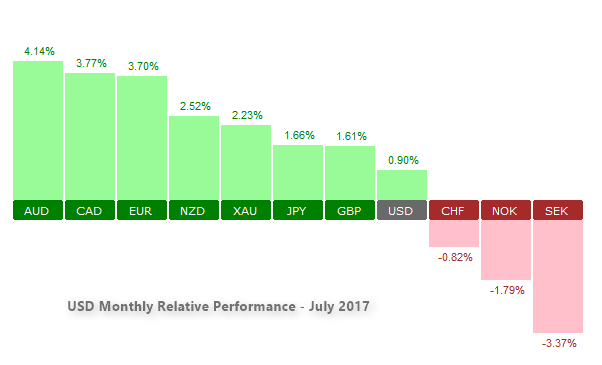

The month of July saw the investor sentiment in the US dollar continue to deteriorate. The greenback came under pressure on both fronts that included economic and political developments. Inflation remained a major concern among policymakers.

While the uncertainty about the stability of the Donald Trump government continued to play in the background.

As expected, the European Central Bank refrained from making any major policy changes. In regards to the ECB’s plans for tapering its QE, the central bank remained non-committal but noted that a decision on tapering could come sometime in autumn.

No specific date has been given but the markets are expecting to hear from the ECB as early as the September meeting. The fact that there is no ECB meeting scheduled this month suggests that the euro currency could remain trading flat for the most part.

The Federal Reserve Chair, Janet Yellen gave her two-day semi-annual testimony on the US Congress last month. The Fed chair commented that the central bank was in no rush to hike interest rates with the current short term rates near the neutral level. The FOMC meeting was held just last week where the central bank kept monetary policy steady.

The month ahead: August 2017

The month of August is expected to remain light with most of the traders taking a summer break on both sides of the Atlantic. Regardless, economic data continues that includes monetary policy decisions from some of the G7 economies.

RBNZ Monetary policy – OCR to remain unchanged (Aug 9th)

The Reserve Bank of New Zealand (RBNZ) will be holding its monetary policy meeting this month. No changes are expected to the Official Cash Rate (OCR) which currently stands at 1.75%.

A week ago, RBNZ official McDermott gave a speech which underlined the fact that the central bank will keep interest rates on hold for a longer period of time. McDermott gave a brief examination of how the central bank viewed the longer-term macro-economic developments while shifting monetary policy.

The RBNZ’s assessment was that the neutral interest rate level had slipped further to 3.5%, down from 4% that it expected previously. The lower neutral rate suggests that the current OCR at 1.75% offered less accommodative monetary policy.

Inflation also continues to remain a concern, something which the RBNZ has been repeatedly highlighting. Headline inflation in New Zealand has increased, close to 2% but as the central bank noted, most of the inflationary gains were only temporary.

While the central bank’s meeting could very well pass off as non-event, further dovish remarks and especially references to the strength of the Kiwi dollar could potentially hit the NZD in the near term.

FOMC Meeting Minutes (Aug 16th)

The FOMC meeting minutes could remain the highlight during the middle of August. The minutes will cover the recently concluded FOMC meeting on July 26. Fed officials voted to keep interest rates unchanged, but noted that it could begin the balance sheet normalization relatively soon.

There was also a hint of optimism as officials expected to push forward with one more rate hike. Investors however are starting to think otherwise. The fact that inflation concerns was mentioned in the statement hit the sentiment in the U.S. dollar quite hard.

The FOMC meeting minutes could likely offer more clues on the deliberations made and could potentially signal that the Fed could begin to unwind the balance sheet starting as early as September.

UK GDP – Second estimate (Aug 24th)

The UK’s Office for National Statistics (ONS) will release the second GDP estimate for the second quarter ending June 2017 on August 24. The data could see some modest revisions.

The first GDP estimate showed that the UK’s economy expanded at a pace of 0.3% during the quarter. On a year over year basis, economic activity in the UK was seen at a rate of 1.7%. This was a slower pace of growth after the economy posted a 2% expansion in the first quarter.

Ahead of the GDP estimates, the Bank of England’s meeting is scheduled this week. During the last monetary policy meeting, three officials voted to hike interest rates. Inflation however has remained stable in the previous month, which could suggest that the BoE could seek more time.

The British pound however continues to remain volatile on a host of factors that include the Brexit storyline as well as the ongoing economic developments in the nation.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)