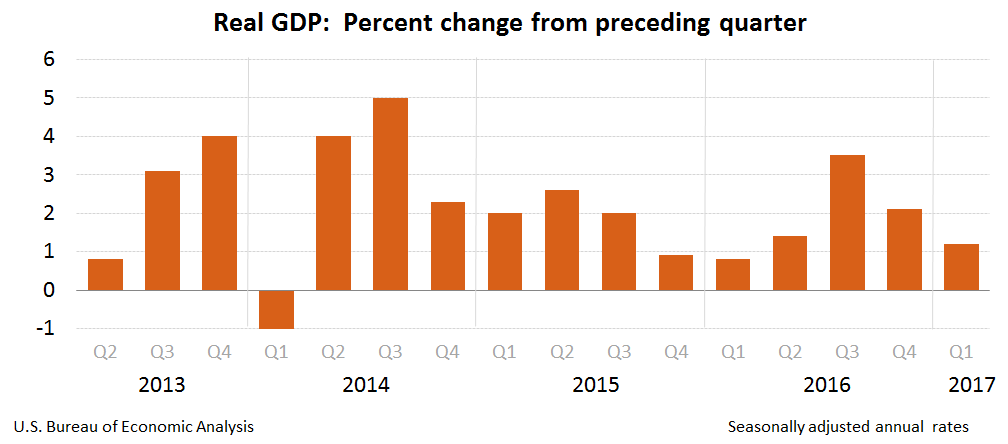

The final revised first quarter gross domestic product (GDP) for the United States will be released today. The data is the third and final revision to be released by the US Department of Commerce for the period ending March 2017.

At the second estimate, the GDP data saw an upside revision to 1.2%, up from 0.9% from the preliminary release. While the data did help to boost the US dollar, the final revision, according to economists polled is widely expected to stay unchanged.

Even if there are any upside revisions to the data, considering that the GDP covers the first quarter, the markets are likely to shrug aside the positivity.

This is because the markets will be already focusing on the upcoming GDP numbers coming out later in July for the second quarter ending June. In the meantime, monetary policy outlook from the Federal Reserve comes under question.

Data released yesterday showed that the advance estimate on the US foreign trade gap in goods during May was at $65.9 billion. This managed to reverse the trade widening in April.

Still, the overall outlook shows that trade could remain a drag on the second quarter GDP, although data for June is yet to come out which is likely to be in time for the second revision to the Q2 GDP.

US Pending Home Sales fall for the third consecutive month

The latest data point to hit the wires was the pending home sales released by the National Association of Realtors (NAR) on Wednesday, 28 June.

According to the data, the number of homes in the US that went into a contract for sale declined in the month of May.

The NAR, which tracks the signing of purchase contracts of a previously owned home fell 0.8% on the month to 108.5. This was in stark contrast to the expectations of a 0.8% increase.

The decline in May puts the year over year pending home sales down 1.7%.

Lawrence Yun, the chief economists from NAR, attributed the decline to both limited choices and house prices that were rising too fast.

However, the data remains conflicting with another measure, called the existing home sales rising 1.1% in May on a month over month basis.

Housing prices remain one of the key indicators for gauging the economic activity. Earlier this week, the Case/Shiller home price index showed that despite an early spring, home prices did not benefit from it. The S&P Case/Shiller HPI rose just 0.3% on the month. Demand for auto sales was also seen falling alongside slower consumer spending.

Besides the home prices, inflation has also slipped back in the past few months. This has prompted some of the key FOMC members to comment that the Fed could look at pausing its rate hike cycle. However, the Fed Chair Janet Yellen commented earlier this week, although not much on monetary policy.

Ms. Yellen said that the US economy is unlikely to face another economic crisis “in our lifetime.” Her comments were taken with a pinch of salt considering that one can never pinpoint the onset of a financial crisis. There is ample evidence from previous Federal Reserve presidents who have given hawkish statements just months or a year ahead from an economic slowdown.

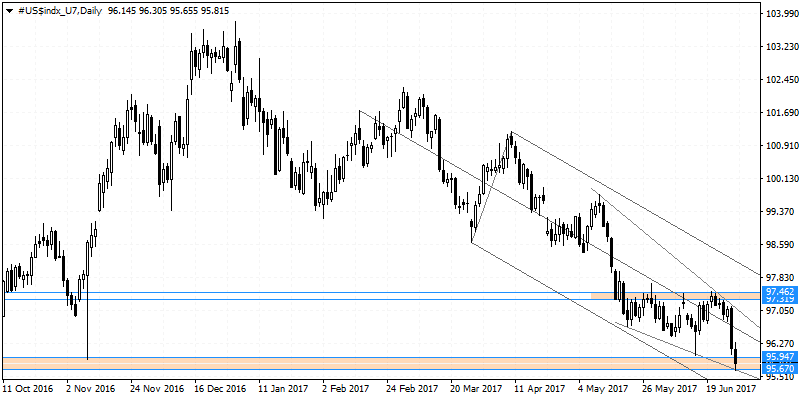

The US dollar continues to come under pressure with the markets slowly being convinced on whether the Fed will be able to maintain and justify its current tightening policy. Still, economists are hopeful that the Fed could get away with one more rate hike this year.

In the near term, the US dollar will need to recover off the current support zone it has entered at 95.95 – 95.67. A reversal off this support could keep the US dollar index range bound within the upper resistance level seen at 97.46 – 97.32.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)