The currency markets will be looking to a slow start next week with Japan, US and Canada closed for business on Monday. However, the action kicked off early with the second US Presidential debate late Sunday (Eastern Standard Time). On the economic front, the FOMC meeting minutes and Fed Chair Janet Yellen’s speech on Friday will be the most anticipated events in an otherwise quiet trading week.

Second presidential debate

The second presidential debate concluded in the wee hours of Sunday/Monday with the markets seen giving Hillary Clinton another victory. The second presidential debate saw Clinton surge ahead in opinion polls after Republican nominee Trump was hit by scandals. Although Clinton’s campaign was also hit by scandals with the latest Wikileaks releasing private speeches from Hillary Clinton where she seemed to back Wall Street, the Democratic candidate walked away from the debate as a clear winner. In response, the USDMXN, which is now a proxy for the elections fell sharply as the Mexican peso surged on a disappointing performance from Trump.

Despite the initial volatility, the markets are likely to settle back into a range with not much of economic data to go by on Monday.

FOMC meeting minutes and Yellen speech

The minutes of September FOMC meeting will be released on Wednesday and investors are likely to gear up to hawkish meeting minutes, following three dissenting votes. With last Friday’s jobs report coming out with a soft print, Fed members, Mester and Fischer maintained an optimistic view in their comments given later on Friday. The coming week will see a lot more Fed speak and it is quite possible that Fed members will continue to maintain the hawkish rhetoric. The Fed-speak culminates with Friday’s speech by Janet Yellen.

On the economic front, US retail sales and producer price index numbers will be coming out this week on Friday. Expectations call for a 0.60% increase in headline retail sales following a 0.30% decline previously. Auto sales in September beat estimates, rising to a seasonally adjusted 17.76 million, well above the consensus estimates of 17.45. Although the September print was positive, auto sales remained weak compared to a year ago. Still, the better than expected print is likely to see some positive upside to retail sales this week. PPI data is expected to rise 0.20% after an unchanged print in August while core PPI is expected to rise 0.10%, the same pace as the month before.

Quiet week for the GBP

After last week’s strong currency moves in GBP, the week ahead is relatively quiet with no major economic releases of impact. The focus will, therefore, be back on the Brexit talks which could continue to put the GBP under pressure. After losing near 6% after Friday’s flash crash, the GBP managed to recover, closing above $1.24. The question is whether the GBP can see some more upside in the near term of if prices will simply remain flat during the week.

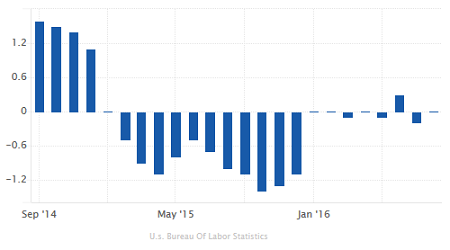

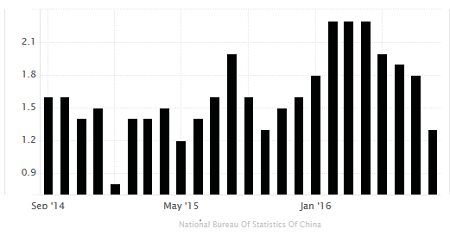

China inflation data on tap

The monthly consumer price index data from China will be coming out this week. Economists expect CPI to rise 1.60% year over year in September, following the 1.30% increase in August which was slower than the previous month’s 1.80% increase. The August CPI reading was also the weakest inflation print in over a year. Still, PPI continued to recover, falling only 0.40% in August, indicating higher prices at the factory gate. China’s PPI has been steadily improving for the past three months, and this continued trend could potentially throw an upside surprise in this week’s CPI report.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)