Image via World Economic Forum

Summary:

- OPEC agrees to limit oil production in the range of 32.5 million – 33.0 million barrels

- Deal to be formalized at the next OPEC meeting in November

- US crude oil inventory report posts fourth consecutive week of declines

- WTI Crude Oil rallies to technical resistance of 47.50 – 47.00 as noted in last week’s report

Crude oil prices posted strong gains yesterday after Iran’s oil minister Bijan Zanganeh said that OPEC members had reached an agreement to cut production. WTI crude oil rose more than 5% on the day gaining over $2, closing at $47.05 a barrel while Brent crude oil rose over 5.90%. Despite the initial euphoria, many questions still remain on the actual impact the oil production cut will have and more importantly if the OPEC countries will reach an agreement to formalize the deal in a few months.

OPEC agrees to cut production

The Organization of Petroleum Exporting Countries reportedly reached an agreement to limit oil production in the range of 32.5 – 33.0 million barrels per day, which came after a series of informal talks held on the sidelines of the 26 – 28 September IEA forum in Algiers.

Iranian oil minister Bijan Zanganeh said, “We have decided to decrease the production around 700,000 bpd.” OPEC members said that it would agree to production levels for each country when it meets next in Vienna on November 30.

The deal came as a surprise to many which saw Iran and Saudi Arabia failing to reach an agreement. Ahead of the informal meeting, Saudi Arabia had agreed to cut production in return for Iran freezing its Oil production; the offer was rejected by Iran.

Phil Flynn from Price Futures Group said, “This is a historic deal. This is the first time OPEC and non-OPEC will agree together in over a decade. This should put a floor on oil and should see oil move back towards the $60’s.”

Oil prices were volatile yesterday with the headlines from OPEC meeting and the weekly crude oil inventory report as well.

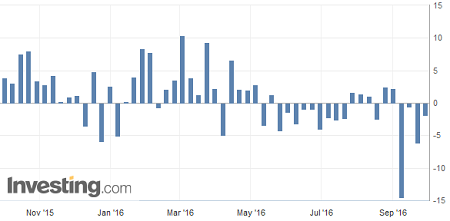

US Crude Oil inventories fall for a fourth consecutive week

Ahead of the OPEC’s announcement, Oil traders were focused on the weekly EIA crude oil inventory report. Data showed that inventories fell 1.9 million barrels for the week ending September 23 with the total US commercial crude oil inventory running at 502.7 million, a historical high by EIA’s standards.

The data beat estimates of a buildup of 3 million barrels and was higher than the API’s reported drawdown of 752,000 barrels. The latest weekly inventory report marks a fourth consecutive week of drawdown in oil inventories.

Still, looking beneath the surface data showed that despite the headline drawdown, gasoline inventories rose 2 million barrels last week and remained above the upper limit of the 5-year average. Oil prices initially rose on the headline release but soon gave up the gains awaiting the OPEC announcement.

Question linger on OPEC’s deal

While oil prices rallied on the OPEC news, many analysts questioned the details of the agreement which has more questions than answers.

In August, oil output was recorded at 33.2 million barrels per day. With the OPEC agreement to limit production within the range of 32.5 – 33 million, the production cut is likely to take a long time for the effects to be filtered down.

The OPEC announcement also said that Libya, Nigeria, and Iran were exempt from the OPEC quotas. A formal decision is expected to be taken at the next OPEC meeting Vienna in November.

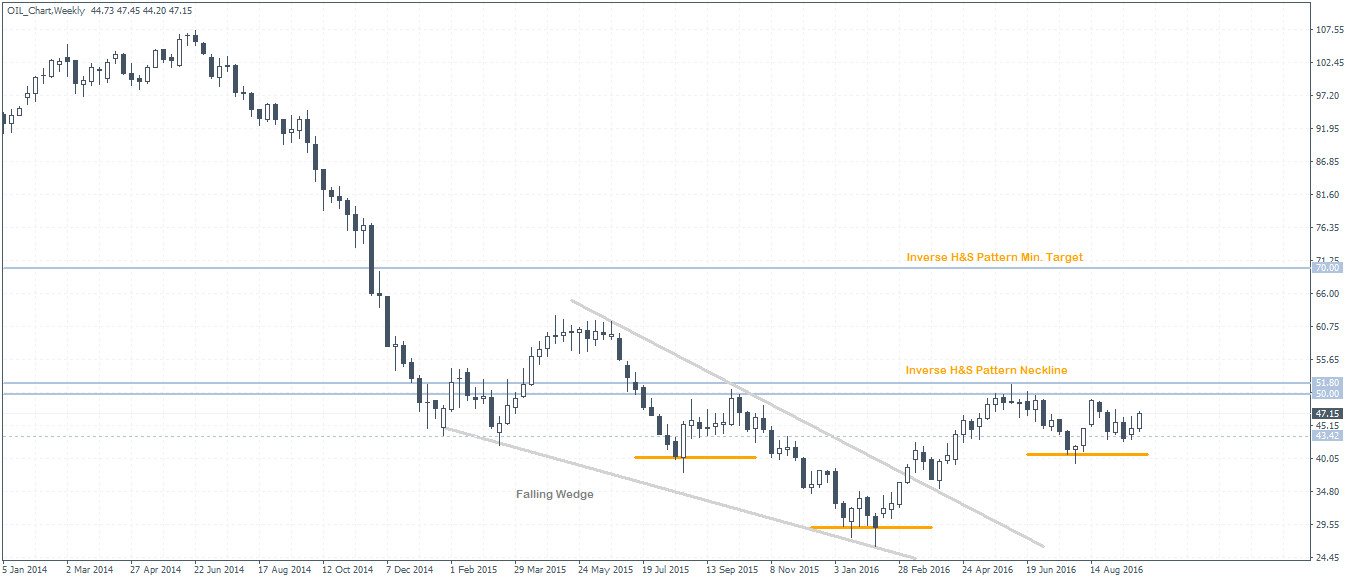

WTI – Next Target $50

Following up from last week’s oil report, the upside is likely to continue albeit a short-term pullback in prices.

The weekly chart for WTI crude oil currently shows a bullish candlestick. A weekly bullish close could confirm the view that oil prices could see further upside in the near term with the declines limited to $43.40. The weekly chart’s evolving head and shoulders pattern points to the next big technical resistance at $51.80 – $50.00 which will be a critical level that oil prices need to break out from. Only a convincing breakout above $50 can ascertain further bullish views towards the measured target of $70.00

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)