Market Summary

- Fed member, Lael Brainard delivered a speech at the Chicago Council of Global Affairs yesterday

- Brainard’s comments were dovish as she maintained that the case for rate hikes was less compelling

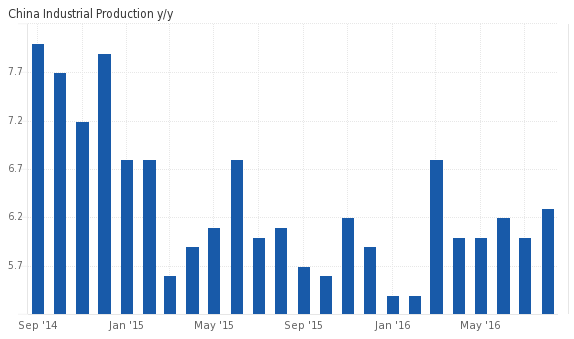

- China industrial production and retail sales improve in August

- Germany inflation flat in August, HICP unchanged at 0.30%

- Sweden inflation rate steady at 1.10% in August

- UK consumer prices remain steady in August at 0.60%

- UK PPI output rises 0.80% in August

Today’s Economic events

- Japan BSI manufacturing index 2.9 vs. -6.5

- Australia NAB business confidence 6 vs. 4 previously

- China industrial production y/y 6.30% vs. 6.20%

- China fixed asset investment ytd/y 8.10% vs. 7.90%

- China retail sales y/y 10.60% vs. 10.20%

- Germany Final CPI m/m 0.0% vs. 0.0%

- German WPI m/m -0.70% vs. 0.10%

- Switzerland PPI m/m -0.30% vs. -0.20%

- Italy industrial production m/m 0.40% vs. 0.20%

- UK CPI y/y 0.60% vs. 0.70%; Core CPI y/y 1.30% vs. 1.40%

- UK PPI input m/m 0.20% vs. 0.60%; PPI output m/m 0.10% vs. 0.30%

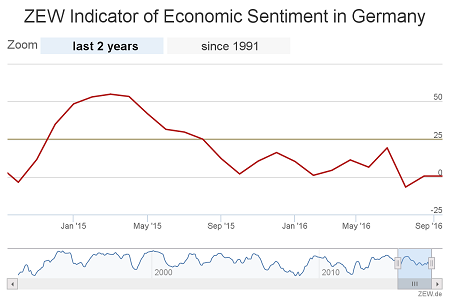

- Germany ZEW economic sentiment 5.4 vs. 6.7

- Eurozone employment change q/q 0.40% vs. 0.20%

- ECB President Mario Draghi speaks

Coming Up

- (NZD) Current Account

Brainard remains a staunch dove

The US dollar fell on late Monday, giving up most of the gains from last Friday after Fed Governor, Lael Brainard’s dovish comments at the Chicago Council on Global Affairs.

The Fed member, known to be dovish in her views on interest rates, reiterated that “the case to tighten monetary policy pre-emptively is less compelling, and the improvement in the labor market hasn’t had the desired effect on inflation.”

Her comments saw the markets re-adjust from last week which saw some of the Fed members coming out hawkish and supporting a rate hike in the near-term. Joe Manimbo from the Western Union said, “Ms. Brainard was true to form, in a dovish sense, reinforcing the case for the Fed to move later rather than sooner. The dollar has tripped, but a lot still hinges on the Fed’s message next week.”

In her prepared text entitled, “The “New Normal” and What It Means for Monetary Policy” Brainard made the following key points.

- Inflation Has Been Undershooting, and the Phillips Curve Has Flattened

- Labor Market Slack Has Been Greater than Anticipated

- Foreign Markets Matter, Especially because Financial Transmission is Strong

- The Neutral Rate Is Likely to Remain Very Low for Some Time

- Policy Options Are Asymmetric

Click here to read the full copy of the text.

Brainard’s comments bolstered the case that the Fed could keep rates on hold at its meeting next week, although some expected the Fed member to warm up to the idea of hiking interest rates as early as next week.

Brainard is the last FOMC member to speak ahead of the one-week blackout period before the Fed decision on September 21. Later this week, the final pieces to the puzzle could likely shape the sentiment with US import prices, retail sales, industrial production and finally consumer price index data on Friday could shift the markets closer to pricing in a rate hike if the data is encouraging.

China industrial production, retail sales better than expected

Economic indicators tracking different sections of the economy in China fared better than expected in August as consumer retail spending and industrial output showed a slight but encouraging pickup in activity.

Industrial production in China increased 6.30% on the year in August, data from the National Bureau of Statistics showed on Tuesday. The headline print beat forecasts of a 6.20% gain and was higher than the 6.0% growth registered in July. On a month over month basis, industrial production rose 0.50%.

“In August, the total value added of the industrial enterprises above designated size was up by 6.3 percent year-on-year at comparable prices,” the statement from NBS showed, noting that pick up in financial indicators stemmed from deeper supply side structural reforms and growth oriented macroeconomic policies.

The NBS data also showed that retail sales advanced 10.60% on an annualized basis, rising above forecasts of 10.20%, which was the same pace of growth in retail sales a month ago. Fixed asset investment grew at the rate of 8.10% on the year on year basis in August and was above forecasts of 7.90%. Fixed asset investment is seen as a proxy for long-term spending. Growth in government spending on fixed assets fell 0.40% to show 21.40% growth on the year in the first eight months of 2016. Private investment growth was, however, unchanged at 2.10%.

The markets, which are already spooked by the Fed rate hike jitters, saw the data as encouraging.

UK CPI steady in August while PPI accelerates

Consumer prices in the UK are expected to rise in the foreseeable future, although the data from August showed that UK’s CPI was steady at 0.60%. Data from the Office for National Statistics showed on Tuesday that consumer prices advanced 0.60% on a year over year basis in August, rising at the same pace as July. Economists expected inflation to rise 0.70%. Core inflation, which strips the volatile food and energy prices, was also steady at 1.30%, slightly below forecasts of 1.40%.

On a month over month basis, consumer prices gained 0.30%, lower than forecasts of 0.40% increase but managed to offset the 0.10% declines seen in July.

In a separate report from the ONS, factory gate prices were however seen rising. PPI output edged higher, rising 0.80% on a year over year basis, accelerating from July’s 0.30% increase. The headline print was, however, lower than the forecasts of 1.0%, indicating a slower than expected pace of increase. On a month over month basis, PPI output rose only 0.10%, slower than July’s 0.30% and missed forecast of a 0.30% increase. Input price inflation, however, increased significantly, rising 7.60% in August from July’s 4.10%.

Reaction to the inflation data was mixed. While some economists expect to see the effects of a weaker exchange rate rub into higher input costs at the factory gates, others are convinced that the EU referendum vote isn’t causing as much of a financial chaos as initially expected.

Mike Prestwood, head of inflation at ONS said, “Fuel costs falling more slowly than a year ago as well as rising food prices and air fares all pushed up CPI in August, but these were offset by hotels, wine, and clothing leaving the headline rate of inflation unchanged. Raw material costs have risen for the second month running, partly due to the falling value of the pound, though there is little sign of this feeding through to consumer prices yet.”

German inflation steady in August

Consumer prices in Germany rose at a pace of 0.40% in August, compared to the same month a year ago. Data from the German statistics office, Destatis showed on Tuesday. On a month over month basis, headline inflation was unchanged indicating no inflation pressures.

Continuing the downward trend, the low inflation rate in August was attributed to declining energy prices and prices of mineral oil products. Energy prices fell 4.20% year on year, but slower than the 4.70% declines registered in July. Food prices rose 0.90% compared to a year ago while prices of goods fell 0.60%.

Claus Vistesen from Pantheon Economics said, “Overall, we think inflation pressures in Germany are rising modestly and that the headline rate will increase to about 1.5% in the next six-to-12 months, mainly as base effects reduce the year-over-year drag from energy prices.”

In a separate report, economic sentiment in Germany was unchanged in September. The ZEW economic sentiment was at 0.5 points with the long-term average at 24.4. The index of assessment of the current situation fell 2.5 points from August, coming in at 5.4 points in September.

The economic development in the eurozone was slightly higher than expected, rising 0.8 points to show 5.4 in September. The assessment indicator for the current situation fell 0.2 points to -10.5 points.

ZEW’s Achim Wambach said, “German exports, particularly to non-EU countries as well as industrial production have disappointed. By contrast, the economic environment in the European Union is improving. Overall, the ZEW Indicator of Economic Sentiment suggests that the economic situation in Germany will remain favourable in the coming six months”