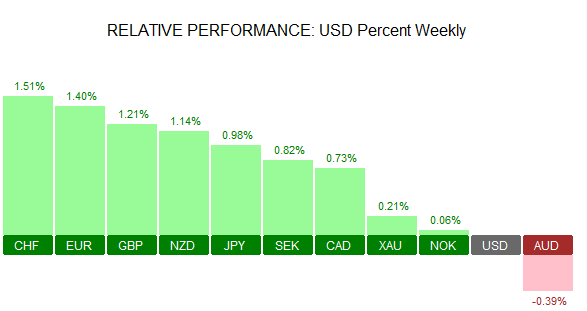

The Australian dollar was the weakest currency last week as the AUD gave up the gains logged earlier in the week after posting a weekly high to 0.7749. Following the AUD was the US dollar which continued to post steady declines for two straight weeks. With diminishing prospects of a rate hike for September the markets continues to bet against the dollar.

On the other end of the scale, the Swiss franc closed the strong gaining 1.51% against the US dollar. This was followed by the euro which closed the week 1.40% higher. Economic data from the euro zone was fairly quiet last week with most of the gains in the euro coming off a weaker greenback. The British pound came in third gaining 1.21% on the week but not before giving up some of its gains on Friday.

Economic Calendar for the Week 22/08 – 26/08

| Date | Time | Currency | Detail | Forecast | Previous |

| 22-Aug | 13:30 | CAD | Wholesale Sales m/m | 0.50% | 1.80% |

| 23-Aug | 03:00 | JPY | Flash Manufacturing PMI | 49.5 | 49.3 |

| 05:00 | JPY | BOJ Gov Kuroda Speaks | |||

| 07:00 | CHF | Trade Balance | 3.79B | 3.55B | |

| 08:00 | EUR | French Flash Manufacturing PMI | 49.1 | 48.6 | |

| EUR | French Flash Services PMI | 50.6 | 50.5 | ||

| 08:30 | EUR | German Flash Manufacturing PMI | 53.7 | 53.8 | |

| EUR | German Flash Services PMI | 54.3 | 54.4 | ||

| 09:00 | EUR | Flash Manufacturing PMI | 52.1 | 52 | |

| EUR | Flash Services PMI | 53 | 52.9 | ||

| 14:45 | USD | Flash Manufacturing PMI | 53.1 | 52.9 | |

| 15:00 | EUR | Consumer Confidence | -8 | -8 | |

| USD | New Home Sales | 575K | 592K | ||

| USD | Richmond Manufacturing Index | 6 | 10 | ||

| 23:45 | NZD | Trade Balance | -320M | 127M | |

| 24-Aug | 02:30 | AUD | Construction Work Done q/q | -1.90% | -2.60% |

| 07:00 | EUR | German Final GDP q/q | 0.30% | 0.40% | |

| 09:30 | GBP | BBA Mortgage Approvals | 38.5K | 40.1K | |

| USD | HPI m/m | 0.30% | 0.20% | ||

| 15:00 | USD | Existing Home Sales | 5.55M | 5.57M | |

| 25-Aug | 09:00 | EUR | German Ifo Business Climate | 108.5 | 108.3 |

| 13:30 | CAD | Corporate Profits q/q | -4.60% | ||

| USD | Core Durable Goods Orders m/m | 0.40% | -0.40% | ||

| USD | Unemployment Claims | 265K | 262K | ||

| USD | Durable Goods Orders m/m | 3.50% | -3.90% | ||

| 14:45 | USD | Flash Services PMI | 52.2 | 51.4 | |

| All Day | ALL | Jackson Hole Symposium | |||

| 26-Aug | 00:30 | JPY | Tokyo Core CPI y/y | -0.40% | -0.40% |

| JPY | National Core CPI y/y | -0.40% | -0.50% | ||

| 06:00 | JPY | BOJ Core CPI y/y | 0.80% | ||

| 07:00 | EUR | GfK German Consumer Climate | 10.2 | 10 | |

| 09:00 | EUR | M3 Money Supply y/y | 5.00% | 5.00% | |

| EUR | Private Loans y/y | 1.80% | 1.70% | ||

| 09:30 | GBP | Second Estimate GDP q/q | 0.60% | 0.60% | |

| GBP | Prelim Business Investment q/q | -0.90% | -0.60% | ||

| GBP | Index of Services 3m/3m | 0.40% | 0.30% | ||

| 13:30 | USD | Prelim GDP q/q | 1.10% | 1.20% | |

| USD | Goods Trade Balance | -62.3B | -63.3B | ||

| USD | Prelim GDP Price Index q/q | 2.20% | 2.20% | ||

| Tentative | USD | Fed Chair Yellen Speaks | |||

| 15:00 | USD | Revised UoM Consumer Sentiment | 90.6 | 90.4 | |

| USD | Revised UoM Inflation Expectations | 2.50% | |||

| All Day | ALL | Jackson Hole Symposium |

Time: GMT+1

Currencies/Events to Watch this Week

AUD: The week ahead is quiet for the Australian economy with Monday seeing the release of the leading index from conference board. On Wednesday, the quarterly report for the construction work done is expected to show a 1.90% decline following a 2.60% decline seen the month before.

JPY: Bank of Japan Governor Kuroda’s speech will be the main event next week. Kuroda is scheduled to speak on Tuesday. Yen strength, the upcoming September monetary policy assessments will be some of the points that are likely to be covered. Later in the week the monthly inflation figures are up for release. The National Core CPI is expected to continue its negative trend with forecasts showing a 0.40% decline albeit slightly better than June’s 0.50% decline. The Tokyo core CPI is also expected to fall 0.40% on the month.

EUR: From the euro area data next week will see the release of flash manufacturing PMI numbers, which will shed light on the Q3 growth. The PMI indices surprised to the positive in July despite the Brexit vote. Expectations for the flash PMI’s for August is expected to see the indices maintain the same pace of growth in the sectors. German Ifo business sentiment data is also up during the week.

GBP: In the UK, the markets are relatively quiet with no major releases in store. Save for the revised Q2 GDP data which is due on Friday. Expectations call for an unchanged print at 0.60% as previously reported in the first estimates. Other second tier data includes the CBI retail survey which is expected to show an improvement in the index falling to a four and half year low in July.

USD: The main event risk from the US the week ahead will be the speech from Fed Chair, Janet Yellen on Friday at the Jackson Hole symposium. Ms. Yellen is expected to prepare the markets for a rate hike later this year, although it remains an open question on whether the Fed will move in September or December. Yellen’s speech will be closely watched also for any references to San Francisco Fed President Williams who had earlier last week suggested that the Fed should consider scrapping the low inflation target for a higher inflation goal. Friday will also see the release of the US GDP report and the durable goods orders due on Thursday.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)