Image via Caribb / Flickr

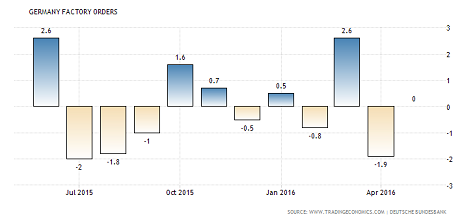

German factory orders slid 0.20% on a year over year basis in May, while staying flat compared to April. Sweden’s Riksbank left interest rates and QE unchanged at today’s monetary policy meeting. Brexit risk off continues with Gold posting new 2-year highs while bond yields continue to fall. Markets await FOMC meeting minutes later today.

Today’s Economic events

- Germany factor orders m/m 0.00% vs. 1.0%; y/y -0.20% vs. 0.90%

- SRB leaves rates unchanged at -0.50%

- Eurozone retail PMI 48.5 vs. 50.6 previously

- The UK housing equity withdrawal q/q 4.9bn vs. -10.1bn

- Canada trade balance -3.28bn vs. -2.6bn

- US trade balance -41.1bn vs. -40.0bn

Coming Up

- US Final services PMI

- US ISM non-manufacturing PMI

- FOMC meeting minutes

German factory orders unchanged in May

Factory orders in Germany for May came out flat, following April’s revised declines of 1.90% and lower than analyst estimates of a 1.0% increase. The German statistics office Destatis released the data earlier today. On a year over year basis, German factory orders fell by 0.20% in May, following up the declines of 0.40% from April and well below the 0.90% annualized increase that was expected.

Domestic orders were down 1.90% on the month while foreign orders increased 1.40% with demand from eurozone countries. Excluding the euro zone countries, new orders fell 0.30%. In terms of sectors, manufacturers of intermediate goods and consumer goods declined the most, while capital goods sector recorded a modest growth.

ING economist, Carsten Brzeski said, “new orders in Europe’s biggest economy have been slipping an average 0.1 percent since the beginning of last year. Even allowing for volatility in monthly readings “the trend is obvious: the German industry is treading water.” Pantheon Macroeconomics called the report “poor” but remained optimistic that the headline number would pick up in the coming months saying “Over the second quarter as a whole, new orders likely fell about 0.2% quarter-on-quarter, following a 0.8% jump in Q1.”

In other news from Germany, the cabinet approved the government’s 2017 spending and medium term goals for the 4-year period, after pledging to keep a balanced budget despite rising costs linked to migration. The new spending plan that was unveiled today following a draft budget from March accounts for higher tax revenue which is estimated to be around 2.4 billion euro. The budget aims to avoid taking on more debt in the four years through 2020. Planned spending of 77.6 billion euros is expected on migration related costs which includes housing and integration. Germany’s debt to GDP ratio stands at 71.02% as of 2015, and the ministry of finance forecasts Germany’s debt ratio to fall below 60% of GDP by 2020.

Swedish Central Bank keeps interest rate on hold

Sweden’s central bank, Riksbank left both the report rate and QE program unchanged at its meeting earlier today, citing that there was no change to inflation outlook since its last meeting in April. Brushing aside the Brexit risks, the central bank kept its short-term easing bias while forecasting that the first rate hike to be in Q3 of 2017, delayed from previous estimates of Q2, 2017. Sweden’s main interest rate is at -0.50%.

The central bank released its monetary policy statement, where it said, “economic activity in Sweden is continuing to strengthen, but there is considerable uncertainty over economic developments abroad, and this has increased as a consequence of the result of the British referendum on the EU… The Executive Board of the Riksbank has therefore decided to hold the repo rate unchanged at -0.5 per cent and now assesses that there will be a longer delay until the repo rate begins to be raised.”

The central bank also revised its projections for inflation and growth for 2017. CPIF inflation is now forecast to average 1.50% in 2016 and 1.80% in 2017, compared to previous estimates of 1.40% and 2.0% respectively. GDP growth is expected to average 3.60% in 2016 and 2.20% in 2017.

Brexit fallout continues – GBPUSD at new 31 year lows

The risk aversion sentiment continues for the second consecutive day with the Sterling seen extending its declines. GBPUSD took a beating in the Asian session after the British pound fell below $1.30 to trade at a new 31-year low at $1.2798 before pulling back strongly during the European session. Sentiment soured as news broke of three UK retail estate investment funds suspending investor redemptions as UK’s housing market, and the economy comes under investor scrutiny.

While the UK is yet to invoke Article 50, many continue to express doubts. Stefan Kraus, from the British Chamber of Commerce in Germany, said, “I find it difficult to imagine that all parliaments will pass it,” talking in the context of a Brexit agreement that needs to be ratified by all national parliaments in the EU. He expressed doubts whether the EU and the UK will reach a deal within the two-year timeframe.

USDJPY was also seen inching closer to the psychological round number of 100Yen as speculators continued to build into long yen positions with some saying the current flows likely to impact Japan’s economy negatively, while prospects of yen intervention remain. Rabobank analysts said, “[Yen appreciation] doesn’t just threaten Japanese deflation, it threatens profitability for major exporters, the one real achievement of Abenomics to date.” while RBC forecasts USDJPY to trade at 92Yen by 2017.

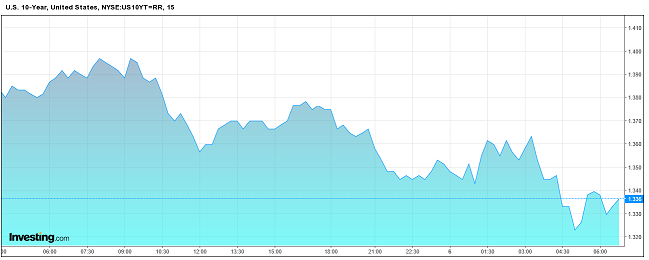

Besides gold and yen, investors also flocked to the safe haven of US Treasuries. The 10-year bond yield was seen down 2.24% trading at 1.33%, which is an all-time low.

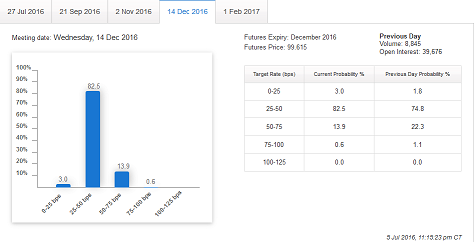

FOMC meeting minutes due later today

The US Federal Reserve will be releasing the meeting minutes from the June policy meeting today at 1800 GMT. The minutes will likely gain investor attention despite the fact that the Fed met before the referendum verdict with some analysts expecting to see some interesting revelations, on questions such as the long-term health of the US economy. The Fed had opted to leave rates unchanged at the June meeting while also lowering rate hike expectations. The Fed’s meeting came after the May’s disappointing jobs report which saw only 38k jobs being added to the economy during the month while previous month’s jobs were revised lower as well.

The CME Futures FedWatch currently shows the probability for a 25bps rate hike at 13.90% in December 2016, meaning that the probability for a Fed rate hike this year is very low. Of course, the view is likely to change as the markets look forward to this Friday’s payrolls report for June.