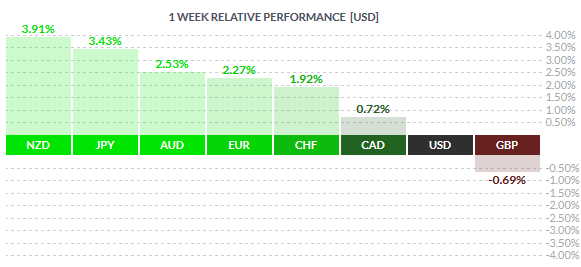

The US dollar was one the weakest currency last week, despite the dollar starting off on a firm footing on Monday. The dollar weakened sharply after Friday’s jobs report came out worse than expected to leave many to question whether the Fed will hike rates in June. This sent the US dollar to close Friday’s session at a 3-week low. The Pound Sterling also closed the week on a bearish note. Although this week was devoid of any Brexit opinion poll related news, the fundamentals were at play with the May PMI numbers coming out weaker than expected and clearly indicating that businesses were being impacted by the EU membership referendum uncertainty.

Among the commodity-linked currencies, the Kiwi was the top performer last week rising 3.91%, while the Aussie managed to rise 2.53% against the US dollar. The yen was also stronger this week, rising 3.43% gaining as some BoJ officials spoke out against the central bank’s policies.

Fundamentals for the Week 06/06 – 10/06

| Date | Time | Currency | Detail | Forecast | Previous |

| 06-Jun | 07:00 | EUR | German Factory Orders m/m | -0.40% | 1.90% |

| 09:10 | EUR | Retail PMI | 47.9 | ||

| 09:30 | EUR | Sentix Investor Confidence | 7.1 | 6.2 | |

| 17:30 | USD | Fed Chair Yellen Speaks | |||

| 07-Jun | 05:30 | AUD | Cash Rate | 1.75% | 1.75% |

| AUD | RBA Rate Statement | ||||

| 06:00 | JPY | Leading Indicators | 100.80% | 99.30% | |

| 07:00 | EUR | German Industrial Production m/m | 0.80% | -1.30% | |

| EUR | French Trade Balance | -4.2B | -4.4B | ||

| 10:00 | EUR | Revised GDP q/q | 0.50% | 0.50% | |

| 13:30 | USD | Revised Nonfarm Productivity q/q | -0.60% | -1.00% | |

| USD | Revised Unit Labor Costs q/q | 4.00% | 4.10% | ||

| 15:00 | CAD | Ivey PMI | 54.2 | 53.1 | |

| USD | IBD/TIPP Economic Optimism | 49.1 | 48.7 | ||

| 20:00 | USD | Consumer Credit m/m | 19.1B | 29.7B | |

| 23:45 | NZD | Manufacturing Sales q/q | -1.90% | ||

| 08-Jun | 00:50 | JPY | Current Account | 2.04T | 1.89T |

| JPY | Final GDP q/q | 0.50% | 0.40% | ||

| JPY | Bank Lending y/y | 2.20% | |||

| JPY | Final GDP Price Index y/y | 0.90% | 0.90% | ||

| 02:30 | AUD | Home Loans m/m | 2.60% | -0.90% | |

| Tentative | CNY | Trade Balance | 358B | 298B | |

| Tentative | CNY | USD-Denominated Trade Balance | 55.8B | 45.6B | |

| 06:00 | JPY | Economy Watchers Sentiment | 43.4 | 43.5 | |

| 08:15 | CHF | CPI m/m | 0.20% | 0.30% | |

| 09:30 | GBP | Manufacturing Production m/m | 0.10% | 0.10% | |

| GBP | Industrial Production m/m | 0.00% | 0.30% | ||

| 13:15 | CAD | Housing Starts | 194K | 192K | |

| 13:30 | CAD | Building Permits m/m | -7.00% | ||

| 22:00 | NZD | Official Cash Rate | 2.00% | 2.25% | |

| NZD | RBNZ Rate Statement | ||||

| NZD | RBNZ Monetary Policy Statement | ||||

| 09-Jun | 00:00 | NZD | RBNZ Press Conference | ||

| 00:50 | JPY | Core Machinery Orders m/m | -3.20% | 5.50% | |

| JPY | M2 Money Stock y/y | 3.30% | 3.30% | ||

| 02:10 | NZD | RBNZ Gov Wheeler Speaks | |||

| 02:30 | CNY | CPI y/y | 2.30% | 2.30% | |

| CNY | PPI y/y | -3.10% | -3.40% | ||

| 06:30 | EUR | French Final Non-Farm Payrolls q/q | 0.20% | 0.20% | |

| 06:45 | CHF | Unemployment Rate | 3.50% | 3.50% | |

| 07:00 | EUR | German Trade Balance | 21.4B | 23.6B | |

| JPY | Prelim Machine Tool Orders y/y | -26.30% | |||

| 08:00 | EUR | ECB President Draghi Speaks | |||

| 09:30 | GBP | Goods Trade Balance | -11.1B | -11.2B | |

| 13:30 | CAD | NHPI m/m | 0.30% | 0.20% | |

| CAD | Capacity Utilization Rate | 81.50% | 81.10% | ||

| USD | Unemployment Claims | 270K | 267K | ||

| 15:00 | USD | Wholesale Inventories m/m | -0.10% | 0.10% | |

| 15:30 | CAD | BOC Financial System Review | |||

| 16:15 | CAD | BOC Gov Poloz Speaks | |||

| 10-Jun | 00:50 | JPY | PPI y/y | -4.20% | -4.20% |

| 05:30 | JPY | Tertiary Industry Activity m/m | 0.70% | -0.70% | |

| 07:00 | EUR | German Final CPI m/m | 0.30% | 0.30% | |

| EUR | German WPI m/m | 0.20% | 0.30% | ||

| 07:45 | EUR | French Industrial Production m/m | 0.50% | -0.30% | |

| 10th-15th | CNY | M2 Money Supply y/y | 12.60% | 12.80% | |

| 10th-15th | CNY | New Loans | 750B | 556B | |

| 09:00 | EUR | Italian Industrial Production m/m | 0.30% | 0.00% | |

| 09:30 | GBP | Construction Output m/m | 1.50% | -3.60% | |

| GBP | Consumer Inflation Expectations | 1.80% | |||

| 13:30 | CAD | Employment Change | 1.1K | -2.1K | |

| CAD | Unemployment Rate | 7.10% | 7.10% | ||

| 15:00 | USD | Prelim UoM Consumer Sentiment | 94.1 | 94.7 | |

| USD | Prelim UoM Inflation Expectations | 2.40% |

Time: GMT+1

Currencies/Events to Watch this Week

AUD: The Australian central bank will be meeting on June 7th where expectations are that the central bank will be standing pat on policy, given the rate cut just last month in May. With an upbeat GDP in the first quarter, the RBA could maintain its accommodative stance but also re-iterate that it would be watching inflation expectations in the near term. Besides the RBA decision, consumer confidence from Westpac and home loans are other details to look forward to.

NZD: The Reserve Bank of New Zealand will be meeting for its monetary policy review on June 8th. While earlier expectations were for a rate cut, the changing economic landscape in New Zealand is now giving conviction that the RBNZ could hold off a rate cut at its meeting this week. The main premise behind this view is the fact that with higher oil prices and the New Zealand budget which is now expected to increase infrastructure spending, thus raising construction prices and excise duty on tobacco products all point to a potential increase in New Zealand inflation expectations. Holding off a rate hike at this week’s meeting will no doubt increase speculation for a rate cut in August.

JPY: Japan’s GDP will be once again in focus, but the final estimates are unlikely to point to any surprises. Japan’s first quarter GDP was recorded at 0.40% while the annualized GDP was recorded at 1.70%. With the BoJ’s meeting on the agenda the week later, the yen could be seen taking a back seat this week.

CNY: China will be released its export/import data alongside the trade balance numbers. Expectations are for exports to rise 1.70%, offsetting the previous month’s decline of 1.80%, while imports are expected to fall 7% following at 10.90% decline in May. Inflation numbers will be closed watched, due out on 9th June. In April, China’s annualized inflation was recorded at 2.30%, while producer price index was seen at -3.40%. Expectations for this week is for inflation to rise at a subdued pace of 2.20%, and PPI is expected to moderate its declines, falling 3.30%.

EUR: Data from the Eurozone this week will be limited to the first quarter final GDP report. No change is expected, confirming that the eurozone economy grew at a pace of 0.50% in the first quarter of this year while posting annualized GDP growth rate of 1.50%. German industrial production and factory orders are also due this week and expected to show some moderation following last month’s strong gains.

GBP: Data from the UK is relatively soft with only the industrial and manufacturing production numbers being the main event to watch for. Industrial production is expected to extend its declines, falling 0.20% for April, posting declines at the same pace as in March on a year over year basis. On a month over month basis, industrial production is expected to rise 0.20%. Manufacturing production is expected to remain flat on a month over month basis while showing a moderate decline of 1.20% on a year over year basis. Trade balance numbers are up on Thursday, June 9th.

CAD: A busy week for Canada starts from Tuesday’s Ivey PMI, which is expected to rise to 54.2 in May, up from April’s 53.1. Building permits and housing starts data will also be coming up this week. On Friday, Canada will be reporting its monthly labor market data. The unemployment rate is expected to hold steady at 7.10% while the net employment change in May is expected to rise a modest 0.9k.

USD: Fed Chair, Janet Yellen will be speaking at an event in Philadelphia on Monday and the markets will be watching her comments. Another FOMC voting member, Rosengren will also be speaking a few hours later. Data from the US this week is relatively quiet for the remainder of the week with only the weekly jobless claims and the UoM consumer confidence being the other major events to look forward to.