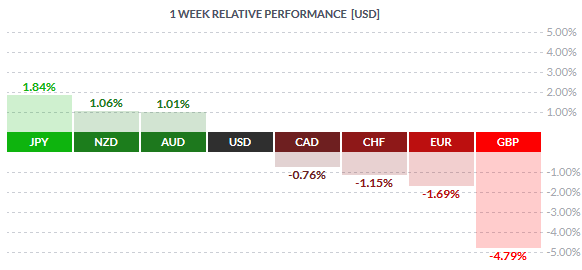

The Pound Sterling was the weakest currency last week losing 4.79% against the US dollar. The declines in GBPUSD came as the UK shocked the world by voting to leave the EU membership which sent ripples across the financial markets. GBPUSD fell to multi-decade lows on the news but managed to recover following the initial reaction. The shocking outcome saw investors flocking to safe haven assets with the Yen rising 1.84% on a week over week basis with USDJPY briefly breaking below the 100Yen psychological level.

The euro was also hit by the Brexit verdict, losing 1.69% from a week ago. The Swiss franc was down 1.15% on the week, but this was mostly due to the SNB’s intervention in the financial markets which saw the CHF stabilize. The US dollar managed to gain in the turmoil as one of the preferred safe haven assets.

Fundamentals for the Week 27/06 – 01/07

| Date | Time | Currency | Detail | Forecast | Previous |

| 27-Jun | 09:00 | EUR | M3 Money Supply y/y | 4.80% | 4.60% |

| EUR | Private Loans y/y | 1.60% | 1.50% | ||

| 13:30 | USD | Goods Trade Balance | -59.5B | -57.5B | |

| 14:45 | USD | Flash Services PMI | 52 | 51.3 | |

| 28-Jun | 07:00 | EUR | German Import Prices m/m | 0.60% | -0.10% |

| 11:00 | GBP | CBI Realized Sales | 9 | 7 | |

| 13:30 | USD | Final GDP q/q | 1.00% | 0.80% | |

| USD | Final GDP Price Index q/q | 0.60% | 0.60% | ||

| 14:00 | USD | S&P/CS Composite-20 HPI y/y | 5.50% | 5.40% | |

| 15:00 | USD | CB Consumer Confidence | 93.2 | 92.6 | |

| USD | Richmond Manufacturing Index | 2 | -1 | ||

| 17:00 | CHF | Gov Board Member Zurbrugg Speaks | |||

| 29-Jun | 00:50 | JPY | Retail Sales y/y | -1.60% | -0.90% |

| 02:00 | AUD | HIA New Home Sales m/m | -4.70% | ||

| 07:00 | CHF | UBS Consumption Indicator | 1.47 | ||

| EUR | GfK German Consumer Climate | 9.8 | 9.8 | ||

| All Day | EUR | Italian Bank Holiday | |||

| 07:00 | GBP | Nationwide HPI m/m | 0.10% | 0.20% | |

| All Day | EUR | German Prelim CPI m/m | 0.10% | 0.30% | |

| 08:00 | EUR | Spanish Flash CPI y/y | -0.90% | -1.00% | |

| 09:30 | GBP | Net Lending to Individuals m/m | 2.9B | 1.6B | |

| GBP | M4 Money Supply m/m | 0.10% | -0.10% | ||

| GBP | Mortgage Approvals | 65K | 66K | ||

| 13:30 | USD | Core PCE Price Index m/m | 0.20% | 0.20% | |

| USD | Personal Spending m/m | 0.30% | 1.00% | ||

| USD | Personal Income m/m | 0.30% | 0.40% | ||

| 15:00 | USD | Pending Home Sales m/m | -0.90% | 5.10% | |

| 15:30 | USD | Crude Oil Inventories | -0.9M | ||

| 21:30 | USD | Bank Stress Test Results | |||

| 23:45 | NZD | Building Consents m/m | 6.60% | ||

| 30-Jun | 00:05 | GBP | GfK Consumer Confidence | -3 | -1 |

| 00:50 | JPY | Prelim Industrial Production m/m | -0.10% | 0.50% | |

| 02:00 | NZD | ANZ Business Confidence | 11.3 | ||

| 02:30 | AUD | Private Sector Credit m/m | 0.50% | 0.50% | |

| 06:00 | JPY | Housing Starts y/y | 4.90% | 9.00% | |

| 07:00 | EUR | German Retail Sales m/m | 0.60% | -0.90% | |

| 07:45 | EUR | French Consumer Spending m/m | -0.10% | -0.10% | |

| EUR | French Prelim CPI m/m | 0.20% | 0.40% | ||

| 08:00 | CHF | KOF Economic Barometer | 103.4 | 102.9 | |

| 08:55 | EUR | German Unemployment Change | -5K | -11K | |

| 09:30 | GBP | Current Account | -28.1B | -32.7B | |

| GBP | Final GDP q/q | 0.40% | 0.40% | ||

| GBP | Index of Services 3m/3m | 0.40% | 0.60% | ||

| GBP | Revised Business Investment q/q | -0.40% | -0.50% | ||

| 10:00 | EUR | CPI Flash Estimate y/y | 0.00% | -0.10% | |

| EUR | Core CPI Flash Estimate y/y | 0.80% | 0.80% | ||

| EUR | Italian Prelim CPI m/m | 0.20% | 0.30% | ||

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | |||

| 13:30 | CAD | GDP m/m | 0.10% | -0.20% | |

| CAD | RMPI m/m | 0.70% | |||

| CAD | IPPI m/m | -0.50% | |||

| USD | Unemployment Claims | 269K | 259K | ||

| 14:45 | USD | Chicago PMI | 50.4 | 49.3 | |

| 01-Jul | 00:30 | AUD | AIG Manufacturing Index | 51 | |

| JPY | Household Spending y/y | -0.90% | -0.40% | ||

| JPY | Tokyo Core CPI y/y | -0.50% | -0.50% | ||

| JPY | National Core CPI y/y | -0.40% | -0.30% | ||

| JPY | Unemployment Rate | 3.20% | 3.20% | ||

| 00:50 | JPY | Tankan Manufacturing Index | 4 | 6 | |

| JPY | Tankan Non-Manufacturing Index | 19 | 22 | ||

| 02:00 | CNY | Manufacturing PMI | 50 | 50.1 | |

| CNY | Non-Manufacturing PMI | 53.1 | |||

| 02:45 | CNY | Caixin Manufacturing PMI | 49.1 | 49.2 | |

| 03:00 | JPY | Final Manufacturing PMI | 47.9 | 47.8 | |

| 06:00 | JPY | BOJ Core CPI y/y | 0.80% | 0.90% | |

| JPY | Consumer Confidence | 41.1 | 40.9 | ||

| 07:30 | AUD | Commodity Prices y/y | -10.00% | ||

| 08:15 | CHF | Retail Sales y/y | -1.70% | -1.90% | |

| EUR | Spanish Manufacturing PMI | 52.1 | 51.8 | ||

| 08:30 | CHF | Manufacturing PMI | 54.9 | 55.8 | |

| 08:45 | EUR | Italian Manufacturing PMI | 52.7 | 52.4 | |

| 08:50 | EUR | French Final Manufacturing PMI | 47.9 | 47.9 | |

| 08:55 | EUR | German Final Manufacturing PMI | 54.5 | 54.4 | |

| 09:00 | EUR | Final Manufacturing PMI | 52.6 | 52.6 | |

| 09:30 | GBP | Manufacturing PMI | 50.2 | 50.1 | |

| 10:00 | EUR | Unemployment Rate | 10.10% | 10.20% | |

| 14:45 | USD | Final Manufacturing PMI | 51.4 | 51.4 | |

| 15:00 | USD | ISM Manufacturing PMI | 51.6 | 51.3 | |

| USD | Construction Spending m/m | 0.70% | -1.80% | ||

| USD | ISM Manufacturing Prices | 63.9 | 63.5 |

Time: GMT+1

Currencies/Events to Watch this Week

AUD: Economic data from Australia for the week ahead is light with the AIG manufacturing index and new home sales data on the tap. The broader market theme following the Brexit is, however, likely to dominate the AUD in the coming week as investors continue to remain in a risk-off sentiment, which could see the AUD remain weaker.

NZD: New Zealand looks towards a quiet week with no major releases coming out with building consents and ANZ business confidence being the exception. Similar to the Aussie dollar, the Kiwi could also remain tied to the Brexit and the risk-off theme in the market.

JPY: Data from Japan next week will see the all-important Tankan manufacturing and non-manufacturing quarterly surveys, which were weaker at the start of the second quarter. The Bank of Japan’s Core CPI data is also expected to be coming out later in the week and is expected to

EUR: Data from the Eurozone is busy starting with the German inflation data for June. Estimates point to a 0.20% increase in headline inflation on a month over month basis, lower than May’s 0.30% increase. In France, inflation is also poised to rise at a weaker pace of 0.20% in June, down from 0.40% a month ago. The Eurozone inflation is expected to stay flat, unchanged for the month on a year over year basis.

GBP: Data from the UK will see the final revision to the first quarter GDP, which is expected to confirm that the UK’s economy expanded at a pace of 0.40%. Later in the week, manufacturing PMI is expected to be released. However, the sterling is likely to take its cues from the Brexit developments than focus on the economic fundamentals.

CAD: Canadian economic calendar is quiet for the most of the week with the exception of June 30th where the monthly GDP numbers are expected to be released. On a month over month basis, Canadian GDP is expected to rise 0.20%, following the -0.20% contraction a month ago.

USD: A busy week for the US dollar gets off with the final revision to the GDP. Q1 GDP is projected to be revised higher to 1.0%, up from the second revision at 0.80%. Later in the week, PCE data is also expected to show moderation with the core PCE expected to rise 0.20% on a month over month basis. Fed Chair, Janet Yellen’s speech is expected later in the week on June 29th. On Friday, US manufacturing ISM data is expected to show a soft print of 51.2 compared to 51.3 a month ago

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)