The Japanese yen has been the most consistent currency this year in maintaining a sustained move. While the Canadian dollar and the Kiwi still maintain the second and third position, the Aussie got toppled off mid-way with the weak Q1 inflation being the catalyst that eventually led to the RBA’s 25bps rate cut.

In February, the USDJPY was seen trading at 115 when we forecasted the potential decline to 104.5 with the possibility of a move to as low as 92. Last week’s Brexit shock sent USDJPY to test 99.01 before recovering to close modestly higher at 102.40Yen.

Here are some of the fundamentals that shaped the forecast over the four month period.

In March, the Bank of Japan left monetary policy unchanged with the board voting 7 – 2 to keep interest rates at -0.10% and 8 – 1 to keep the monetary base unchanged. In its March meeting, the BoJ communicated that it would add more easing if necessary in its policy statement.

As the BoJ stood on the sidelines, the yen continued its gradual appreciation against the US dollar. A few days later the Federal Reserve kept its monetary policy on hold citing the global economic headwinds and projected two rate hikes in the year. Janet Yellen, in her speaking engagements, used the opportunity to send a dovish signal to the markets as well. There were also rumors about the secret G20 Shanghai Pact to weaken the greenback, which further emboldened yen speculations to hold on to their longs.

By April the USDJPY continued to descend gradually and it was the BoJ’s meeting in April that saw the downside momentum increase. Prior to the April 28th meeting, the previous week, Bloomberg reported, citing unnamed sources that the BoJ was likely to ease at its policy meeting in April. However, the BoJ again remained on the sidelines. It was a perfect buy the rumor sell the fact trade as the USDJPY initially jumped from 108 to 112 on the rumors before finally crashing below the 108 levels again. The US dollar around this time was also weaker as the Fed remained on the sidelines and the Q1 GDP figures alongside other economic data remained bleak, prompting many to doubt the prospects of rate hikes bring recession talks back on the table.

May was relatively quiet for the markets but not before the US dollar fell to 16-month lows with the dollar testing the 106Yen level. US economic data in May started to turn the corner with retail sales showing strong gains in the prior months while US inflation was also seen picking up. Meanwhile, Japanese officials continued with their verbal threats which sort of helped to slow the yen’s appreciation. But at the same time, the US Treasury’s Semiannual Report on International Economic and Exchange Rate Policies dealt another blow to Japan, naming the country among five others for being actively engaging in the Fx markets and using unfair trade practices to keep their exchange rates lower. By late-May/early-June, there was a clear verbal duel between Washington and Tokyo officials as the yen continued to post a steady decline since the start of the month.

By early June, the markets were all on about Brexit and the yen gained as a result of the prevailing uncertainty. Both the Fed and the BoJ remained on the sidelines during their respective monetary policy meetings which came just a week before the EU referendum vote in the UK.

On June 23rd, as the UK surprised the world with its vote to exit the EU, the risk off sentiment took a strong hold sending the dollar to lows of 99.01.

USDJPY – What comes next?

With the Brexit outcome and the uncertainty that it has brought, the prospects of dovish central banking policies trump any potential tightening. While the Federal Reserve is expected to keep rates steady in the near term with only one rate hike now expected in 2016, for the Bank of Japan, the July meeting is very likely to be an ideal time for policy easing.

On Friday, the official consumer price index data is expected. In April, core consumer prices fell 0.30% on the year. The BoJ’s core CPI logged 0.90% in April. A weak inflation print could potentially indicate that the underlying inflation trend was most likely to be weakening. Following this Friday’s inflation number the Bank of Japan will be releasing its inflation outlook next week. This could be an important report as a weak inflation expectation from the report could potentially increase the bets for a BoJ policy easing in July. Japan will also be holding elections to the upper house on July 10th, and many claim that the BoJ could proceed with more expansion following a favorable verdict for Abe.

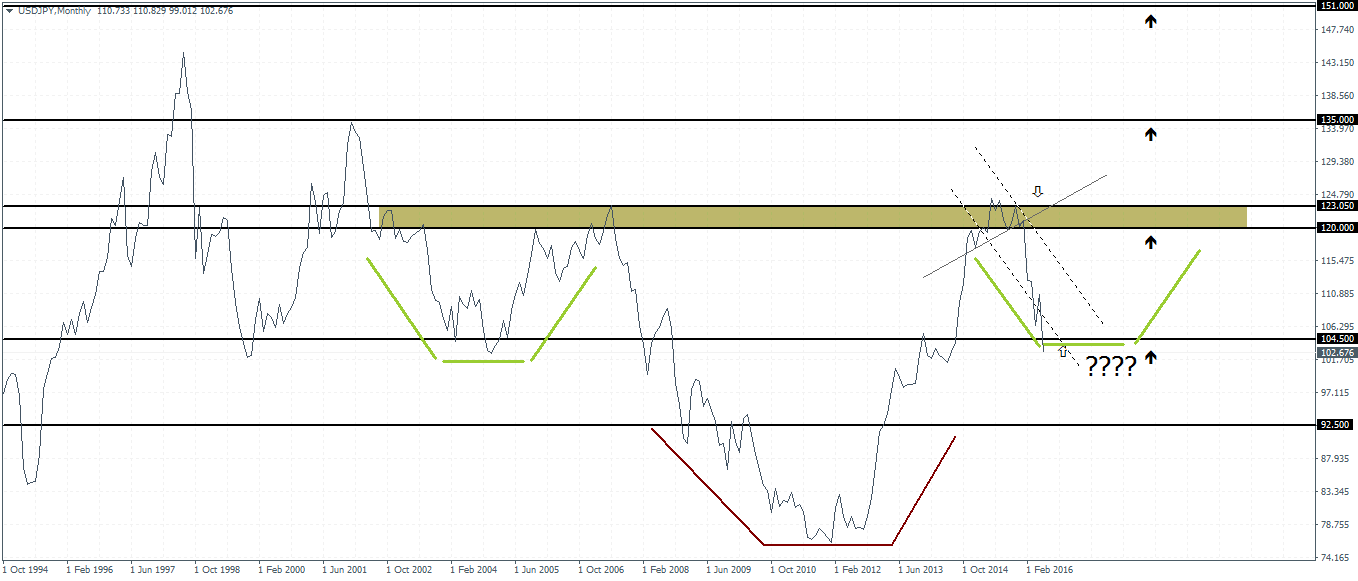

Technical Forecast – USDJPY

The dollar is likely to remain to hover around the 105 – 98 levels and with the Brexit fears abating, further downside is unlikely at this point in time. Support is seen coming near 100.4 – 101.45. A weekly bullish reversal at this level could potentially signal a move to the upside with 104.5 level essential to give way for further gains. Above 104.5, USDJPY is very likely to continue its gains towards 120 – 123 levels marking the inverse head and shoulder pattern’s neckline resistance.

Alternately, in the event that the support at 100.4 – 101.45 fails, USDJPY could extend its declines to 92.50 where the next main support comes into play.