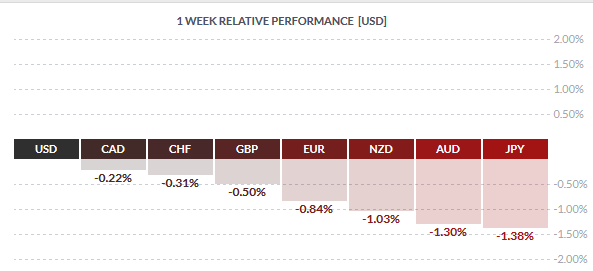

The US dollar emerged on the top of the charts this week supported largely by the verbal intervention threats from Japan. The dollar got a boost by Friday as retail sales posted the biggest monthly jump which helped the dollar to make strong gains on the day. The Canadian dollar was the close next which was supported mostly by Oil prices.

The yen was of course the weakest currency this week only next to the Australian dollar which continued to weaken as sentiment in the Australia dollar soured with markets pushing prices lower in anticipation of more rate cuts from the RBA later in the year.

Fundamentals for the Week 16/05 – 20/05

| Date | Time | Currency | Detail | Forecast | Previous |

| 16-May | 00:01 | GBP | Rightmove HPI m/m | 1.30% | |

| 00:50 | JPY | PPI y/y | -3.70% | -3.80% | |

| 07:00 | JPY | Prelim Machine Tool Orders y/y | -21.20% | ||

| 13:30 | USD | Empire State Manufacturing Index | 7.2 | 9.6 | |

| 15:00 | USD | NAHB Housing Market Index | 59 | 58 | |

| 15:30 | CAD | BOC Review | |||

| 17-May | 02:30 | AUD | Monetary Policy Meeting Minutes | ||

| 04:00 | NZD | Inflation Expectations q/q | 1.60% | ||

| 05:30 | JPY | Revised Industrial Production m/m | 3.60% | 3.60% | |

| 08:15 | CHF | PPI m/m | 0.10% | 0.00% | |

| 09:30 | GBP | CPI y/y | 0.50% | 0.50% | |

| GBP | PPI Input m/m | 1.10% | 2.00% | ||

| GBP | RPI y/y | 1.60% | 1.60% | ||

| GBP | Core CPI y/y | 1.50% | 1.50% | ||

| GBP | HPI y/y | 7.90% | 7.60% | ||

| GBP | PPI Output m/m | 0.20% | 0.30% | ||

| 10:00 | EUR | Trade Balance | 23.1B | 20.2B | |

| 13:30 | CAD | Manufacturing Sales m/m | -0.70% | -3.30% | |

| USD | Building Permits | 1.13M | 1.09M | ||

| USD | CPI m/m | 0.40% | 0.10% | ||

| USD | Core CPI m/m | 0.20% | 0.10% | ||

| USD | Housing Starts | 1.12M | 1.09M | ||

| 14:15 | USD | Capacity Utilization Rate | 75.10% | 74.80% | |

| USD | Industrial Production m/m | 0.30% | -0.60% | ||

| 23:45 | NZD | PPI Input q/q | 0.30% | -1.20% | |

| NZD | PPI Output q/q | 0.40% | -0.80% | ||

| 18-May | 00:50 | JPY | Prelim GDP q/q | 0.10% | -0.30% |

| JPY | Prelim GDP Price Index y/y | 1.00% | 1.50% | ||

| 01:30 | AUD | MI Leading Index m/m | -0.10% | ||

| 02:00 | AUD | RBA Assist Gov Debelle Speaks | |||

| 02:30 | AUD | Wage Price Index q/q | 0.50% | 0.50% | |

| 09:30 | GBP | Average Earnings Index 3m/y | 1.70% | 1.80% | |

| GBP | Claimant Count Change | 4.1K | 6.7K | ||

| GBP | Unemployment Rate | 5.10% | 5.10% | ||

| 10:00 | EUR | Final CPI y/y | -0.20% | -0.20% | |

| EUR | Final Core CPI y/y | 0.70% | 0.80% | ||

| 15:30 | USD | Crude Oil Inventories | -3.4M | ||

| 19:00 | USD | FOMC Meeting Minutes | |||

| 19-May | 00:50 | JPY | Core Machinery Orders m/m | -1.90% | -9.20% |

| 02:30 | AUD | Employment Change | 12.3K | 26.1K | |

| AUD | Unemployment Rate | 5.80% | 5.70% | ||

| 05:30 | JPY | All Industries Activity m/m | 0.70% | -1.20% | |

| 09:00 | EUR | Current Account | 19.6B | 19.0B | |

| 09:30 | GBP | Retail Sales m/m | 0.70% | -1.30% | |

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | |||

| 13:30 | CAD | Wholesale Sales m/m | 0.50% | -2.20% | |

| USD | Philly Fed Manufacturing Index | 3.2 | -1.6 | ||

| USD | Unemployment Claims | 276K | 294K | ||

| 20-May | 07:00 | EUR | German PPI m/m | 0.20% | 0.00% |

| All Day | ALL | G7 Meetings | |||

| 13:30 | CAD | Core CPI m/m | 0.20% | 0.70% | |

| CAD | Core Retail Sales m/m | -0.40% | 0.20% | ||

| CAD | CPI m/m | 0.40% | 0.60% | ||

| CAD | Retail Sales m/m | -0.70% | 0.40% | ||

| 14:00 | USD | FOMC Member Tarullo Speaks | |||

| 15:00 | USD | Existing Home Sales | 5.39M | 5.33M |

Time: GMT+1

Currencies/Events to Watch this Week

AUD: The RBA’s monetary policy meeting will kick off the week from Tuesday. The meeting minutes might be important in light of the 25bps rate cut in early May. Later in the week, the monthly employment report from Australia is expected to show net monthly job gains of 12.3k, lower than the previous month’s 26.1k gains. The Australian unemployment rate is expected to tick higher to 5.80% from 5.70%. A beat on the estimates could, however, stem the declines in the Australian dollar, which has been steadily declining since the weak quarterly inflation and the RBA rate cut that followed.

NZD: Not much of data is due from New Zealand this coming week with inflation expectations for the quarter being the main data to watch for. Previously, quarterly inflation expectations were at 1.60%, falling from 1.90% prior. Quarterly producer prices are also expected to come out later on Tuesday, which is expected to rise 0.30% slower than the previous quarter’s 1.20% declines.

JPY: Preliminary GDP data will be dominating the news next week with expectations that the first quarter GDP in Japan was improved at 0.10% growth compared to 0.30% declines previously. The bullish estimates come in the backdrop of a better than expected trade balance data from Japan last week. The G7 meetings will also be important as Japanese officials continue to talk down the yen, in conflict with the US.

EUR: Data from Eurozone is fairly limited next week with the exception of the final CPI estimates. Expectations call for inflation to have fallen 0.20% on a yearly basis while core CPI is also expected to rise at a slower pace of 0.70%, down from 0.80% previously.

GBP: A busy week for the British pound data includes inflation numbers on Tuesday, which is expected to show a 0.50% increase yearly while core inflation is expected to remain unchanged at 1.50%. Following the inflation data, the monthly jobs report is due on Wednesday which is expected to show the unemployment rate staying unchanged at 5.10%. Average earnings are expected to rise at a slower pace of 1.70% compared to 1.80% previously. On Thursday, retail sales numbers from the UK is expected to moderate, rising 0.70% in April following March’s 1.30% declines.

CAD: Data from Canada over the week starts with manufacturing sales which is expected to fall 0.70% extending the 3.30% declines from the prior month. Inflation data is due on Friday and is expected to show a 0.40% increase, slower than the previous month’s 0.60% increase while core CPI is expected to rise 0.20% compared to 0.70% previously. Retail sales will also be released and is expected to show a contraction of 0.70% for the month.

USD: Data from the US will focus on Tuesday’s inflation report. Expectations call for a modest rebound with US inflation expected to rise 0.40% to the headline and 0.20% on the core. On Wednesday, FOMC meeting minutes will be out and is expected to bring some volatility to the markets.