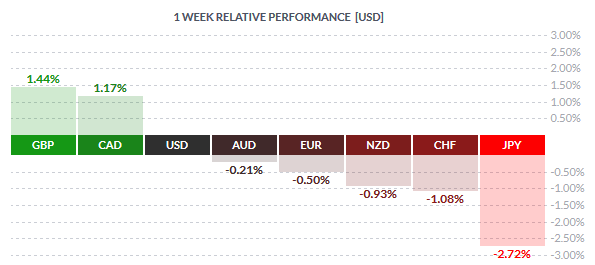

The yen fell sharply this week and on Friday following news reports that the Bank of Japan was considering an ECB-style TLTRO option to introduce negative rates for bank lending. The news report from Bloomberg came out early Friday and the yen slipped sharply losing over 2.72% for the week. The reports come ahead of the BoJ’s monetary policy meeting this coming week. The weak yen saw the Swiss franc losing ground as well.

The British pound and the Canadian dollar were the top gainers this week. While the CAD was supported by strong oil prices and broadly better than expected fundamentals, the British pound saw some weak set of data including retail sales that continued to decline and the UK’s unemployment situation which is showing signs of cooling down

Fundamentals for the Week 25/04 – 28/04

| Date | Time | Currency | Detail | Forecast | Previous |

| 25-Apr | 9:00 | EUR | German Ifo Business Climate | 107.1 | 106.7 |

| 15:00 | USD | New Home Sales | 521K | 512K | |

| 26-Apr | 13:30 | USD | Core Durable Goods Orders m/m | 0.60% | -1.30% |

| USD | Durable Goods Orders m/m | 1.90% | -3.00% | ||

| 13:55 | CAD | BOC Gov Poloz Speaks | |||

| 15:00 | USD | CB Consumer Confidence | 95.8 | 96.2 | |

| 23:45 | NZD | Trade Balance | 405M | 339M | |

| 27-Apr | 02:30 | AUD | CPI q/q | 0.20% | 0.40% |

| AUD | Trimmed Mean CPI q/q | 0.50% | 0.60% | ||

| 09:00 | EUR | M3 Money Supply y/y | 5.00% | 5.00% | |

| 09:30 | GBP | Prelim GDP q/q | 0.40% | 0.60% | |

| 15:00 | USD | Pending Home Sales m/m | 0.30% | 3.50% | |

| 15:30 | USD | Crude Oil Inventories | 2.1M | ||

| 19:00 | USD | FOMC Statement | |||

| USD | Federal Funds Rate | <0.50% | <0.50% | ||

| 22:00 | NZD | Official Cash Rate | 2.25% | 2.25% | |

| NZD | RBNZ Rate Statement | ||||

| 28-Apr | 00:30 | JPY | Household Spending y/y | -4.00% | 1.20% |

| JPY | Tokyo Core CPI y/y | -0.30% | -0.30% | ||

| 00:50 | JPY | Retail Sales y/y | -1.40% | 0.40% | |

| Tentative | JPY | Monetary Policy Statement | |||

| 06:00 | JPY | BOJ Outlook Report | |||

| All Day | EUR | German Prelim CPI m/m | -0.20% | 0.80% | |

| Tentative | JPY | BOJ Press Conference | |||

| 08:00 | EUR | Spanish Flash CPI y/y | -0.70% | -0.80% | |

| EUR | Spanish Unemployment Rate | 20.90% | 20.90% | ||

| 08:55 | EUR | German Unemployment Change | 1K | 0K | |

| 13:30 | USD | Advance GDP q/q | 0.70% | 1.40% | |

| USD | Unemployment Claims | 252K | 247K | ||

| USD | Advance GDP Price Index q/q | 0.50% | 0.90% | ||

| 29-Apr | 02:00 | NZD | ANZ Business Confidence | 3.2 | |

| 02:30 | AUD | PPI q/q | 0.20% | 0.30% | |

| 04:45 | AUD | RBA Assist Gov Debelle Speaks | |||

| 07:00 | EUR | German Retail Sales m/m | 0.30% | -0.40% | |

| 08:00 | CHF | KOF Economic Barometer | 102.9 | 102.5 | |

| EUR | Spanish Flash GDP q/q | 0.70% | 0.80% | ||

| 09:00 | CHF | SNB Chairman Jordan Speaks | |||

| 09:30 | GBP | Net Lending to Individuals m/m | 5.0B | 4.9B | |

| 10:00 | EUR | CPI Flash Estimate y/y | -0.10% | 0.00% | |

| EUR | Core CPI Flash Estimate y/y | 0.90% | 1.00% | ||

| 13:00 | GBP | MPC Member Cunliffe Speaks | |||

| 13:30 | CAD | GDP m/m | 0.60% | ||

| CAD | RMPI m/m | -2.60% | |||

| USD | Core PCE Price Index m/m | 0.10% | 0.10% | ||

| USD | Employment Cost Index q/q | 0.60% | 0.60% | ||

| USD | Personal Spending m/m | 0.20% | 0.10% | ||

| 14:45 | USD | Chicago PMI | 53.1 | 53.6 | |

| 15:00 | USD | Revised UoM Consumer Sentiment | 90.3 | 89.7 |

Time: GMT+1

Currencies/Events to Watch this Week

AUD: The Aussie is trading at 10-month high with prices briefly flirting near $0.7823 last week. The RBA’s meeting minutes revealed that the monetary policy committee was concerned on the exchange rate’s appreciation as it could hamper the delicate rebalancing of the Australian economy. Inflation was also one of the concerns raised by the RBA. This week the quarterly inflation report from Australia is due for release on April 27th. Economists expect the first quarter inflation to rise 0.20%, down from 0.40% in the fourth quarter of 2015. On a year over year basis, inflation is expected to remain unchanged at 1.70%. Weak inflation alongside rising AUD’s exchange rate could see the RBA tone up its dovish rhetoric on the exchange rate and could also open up room for another rate cut. The week will also see the export and import prices for the first quarter. Exports are expected to fall 1.50%, down from -5.40% in the fourth quarter, while import prices are expected to fall 0.90% down from 0.30% slump in the fourth quarter. Overall, Australia’s economic data this week could prove to be decisive on how the RBA will react at its next meeting.

[Tweet “Australia: Economists expect the first quarter inflation to rise 0.20%”]

NZD: The Kiwi is trading near a 10-month high with prices briefly trading above $0.70 last week before pulling back since Wednesday. The RBNZ’s interest rate meeting is due this week on April 27th. No changes are expected to interest rates after the RBNZ slashed rates by 25bps only last month, bringing the key lending rates to 2.25%. However, the monetary policy statement is likely to come down strongly on the Kiwi’s exchange rate which shows no signs of letting go. New Zealand’s import and export data is also due this week with March’s trade balance expected to show a surplus, rising 0.4 billion, softly higher from 0.34 billion in February. Exports are expected to increase 4.65 billion in March while imports are expected to rise 4.28 billion during the month.

JPY: The yen eased back mid week after early Friday Bloomberg reported that the BoJ was considering to cut its bank lending rates into negative. It currently stands at zero percent. Cutting the bank lending rates is being seen by some as a move to boost lending and induce consumer spending. The yen has been resilient this year and continues to remain as the top currency this week. While USDJPY has stabilized off its 17-month lows near 108/107, forecasters expect to see the yen strengthen even more. The big question this week will be whether the BoJ will ease its monetary policy after weeks of struggling to talk down the currency with both the BoJ and government officials warning speculators on the yen’s rapid and volatile moves. Besides the BoJ, Japan’s unemployment data is also due on 27th April, with expectations of an unchanged print at 3.30%.

[Tweet “EUR: Flash estimates on inflation is expected to show the headline CPI rise 0.10% in April”]

EUR: Data from the Eurozone this week is relatively light. Flash estimates on inflation is expected to show the headline CPI rise 0.10% in April, while the core CPI is expected to slowdown, rising 0.90% in April. Eurozone’s unemployment rate is also expected to be released on April 29th with estimates of an unchanged print at 10.30%. EURUSD attempted to rally last week, but the single currency fell after briefly trading near $1.137 on Thursday. France and Germany will be releasing the inflation data as well which is expected to see German CPI falling 0.10% in April while French CPI is expected to rise 0.10%.

GBP: It will be a slow week for the British Pound this week with the advance GDP estimates standing out in an otherwise quiet week. Q1 2016 GDP in the UK is expected to rise 0.40%, slower than 0.60% increase in Q4 of 2015. The slow start to the first quarter was seen in weak retail sales and lower PMI’s alongside weak manufacturing and industrial production growth figures. GBPUSD remains trading above the $1.43 handle.

CAD: The Canadian dollar continued to post strong gains supported by the strong rally in oil markets. USDCAD was trading near a 9-month low last week as prices fell to 1.259. The CAD was also supported by strong economic data in January. But as BoC Governor Stephen Poloz mentioned in the monetary policy statement few weeks ago, the initial gains could be short lived. Canada’s GDP data is due out on April 29th.

USD: While the US dollar managed to recover from the initial declines last week, the focus next week will be the FOMC meeting and the advance GDP data. Ahead of these main events, new home sales data is due out on Monday and is expected to rise 1.60% softly below the 2.0% increase see in February. Durable goods orders are due on 26th April and expected to recover with a 1.90% increase on the headline and 0.50% increase on the core, in March. Housing data continues with pending home sales expected to rise 0.20%, sharply lower compared to February’s 3.50% increase. On Wednesday, the FOMC statement is also due for release and is followed by the advance GDP report for Q1 the next day. Expectations show the US first quarter GDP to rise 0.70%, down from 1.40% increase in Q4 of 2015.