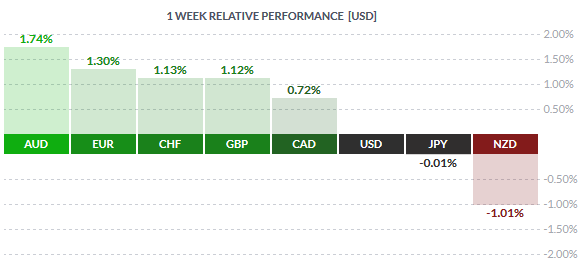

Last week saw the Australian dollar post strong gains, rising 1.74%. The gains came about as the AUDUSD closed a second week with strong gains. Overall, the Aussie is up nearly 10% since the start of 2016 trading near the 0.755 handle. The Kiwi was the weakest as the RBNZ’s surprise rate cut sent the currency to close lower for the week. However, by Friday, NZDUSD was seen recovering most of those losses. The Euro, which initially as trading weaker also managed to trim its declines and in fact closed the week on a stronger note, gaining close to 1.30% for the week against the US Dollar. The Euro gained despite the ECB cutting rates and expanding its QE purchases.

The US Dollar and the Yen were the weakest as the Federal Reserve and the BoJ are due to meet next week.

Fundamentals for the Week 14/03 – 18/03

| Date | Time | Currency | Detail | Forecast | Previous |

| 14-Mar | 01:50 | JPY | Core Machinery Orders m/m | 2.00% | 4.20% |

| 12:00 | EUR | Industrial Production m/m | 1.70% | -1.00% | |

| 21:00 | NZD | RBNZ Gov Wheeler Speaks | |||

| 15-Mar | 02:30 | AUD | Monetary Policy Meeting Minutes | ||

| AUD | New Motor Vehicle Sales m/m | 0.50% | |||

| Tentative | JPY | Monetary Policy Statement | |||

| 06:30 | JPY | Revised Industrial Production m/m | 3.70% | 3.70% | |

| JPY | Tertiary Industry Activity m/m | 0.40% | -0.60% | ||

| Tentative | JPY | BOJ Press Conference | |||

| 09:45 | EUR | French Final CPI m/m | 0.20% | 0.20% | |

| 12:00 | EUR | Employment Change q/q | 0.20% | 0.30% | |

| 14:30 | USD | Core Retail Sales m/m | -0.20% | 0.10% | |

| USD | PPI m/m | -0.10% | 0.10% | ||

| USD | Retail Sales m/m | -0.10% | 0.20% | ||

| USD | Core PPI m/m | 0.10% | 0.40% | ||

| USD | Empire State Manufacturing Index | -10.1 | -16.6 | ||

| 16:00 | USD | Business Inventories m/m | 0.00% | 0.10% | |

| USD | NAHB Housing Market Index | 59 | 58 | ||

| Tentative | NZD | GDT Price Index | 1.40% | ||

| 22:00 | USD | TIC Long-Term Purchases | -29.4B | ||

| 23:45 | NZD | Current Account | -2.90B | -4.75B | |

| 16-Mar | 01:30 | AUD | MI Leading Index m/m | 0.00% | |

| 11:30 | GBP | Average Earnings Index 3m/y | 2.00% | 1.90% | |

| GBP | Claimant Count Change | -9.0K | -14.8K | ||

| GBP | Unemployment Rate | 5.10% | 5.10% | ||

| Tentative | EUR | German 10-y Bond Auction | 0.26|1.2 | ||

| 14:30 | CAD | Manufacturing Sales m/m | 1.20% | ||

| CAD | Foreign Securities Purchases | -1.41B | |||

| GBP | Annual Budget Release | ||||

| USD | Building Permits | 1.20M | 1.20M | ||

| USD | CPI m/m | -0.20% | 0.00% | ||

| USD | Core CPI m/m | 0.10% | 0.30% | ||

| USD | Housing Starts | 1.15M | 1.10M | ||

| 15:15 | USD | Capacity Utilization Rate | 77.00% | 77.10% | |

| USD | Industrial Production m/m | -0.10% | 0.90% | ||

| 15:30 | GBP | CB Leading Index m/m | 0.40% | ||

| 16:30 | USD | Crude Oil Inventories | 3.9M | ||

| 20:00 | USD | FOMC Economic Projections | |||

| USD | FOMC Statement | ||||

| USD | Federal Funds Rate | <0.50% | <0.50% | ||

| 20:30 | USD | FOMC Press Conference | |||

| 23:45 | NZD | GDP q/q | 0.70% | 0.90% | |

| 17-Mar | 00:05 | AUD | RBA Assist Gov Debelle Speaks | ||

| 01:50 | JPY | Trade Balance | 0.24T | 0.12T | |

| 02:30 | AUD | Employment Change | 12.3K | -7.9K | |

| AUD | Unemployment Rate | 6.00% | 6.00% | ||

| AUD | RBA Bulletin | ||||

| 08:45 | CHF | SECO Economic Forecasts | |||

| 10:15 | CHF | PPI m/m | 0.20% | -0.40% | |

| 10:30 | CHF | Libor Rate | -0.75% | -0.75% | |

| CHF | SNB Monetary Policy Assessment | ||||

| 11:00 | EUR | Italian Trade Balance | 4.33B | 6.02B | |

| 12:00 | EUR | Final CPI y/y | -0.20% | -0.20% | |

| EUR | Final Core CPI y/y | 0.70% | 0.70% | ||

| EUR | Trade Balance | 20.2B | 21.0B | ||

| Tentative | EUR | Spanish 10-y Bond Auction | |||

| 14:00 | GBP | MPC Official Bank Rate Votes | 0-0-9 | 0-0-9 | |

| GBP | Monetary Policy Summary | ||||

| GBP | Official Bank Rate | 0.50% | 0.50% | ||

| GBP | Asset Purchase Facility | 375B | 375B | ||

| GBP | MPC Asset Purchase Facility Votes | 0-0-9 | 0-0-9 | ||

| 14:30 | CAD | Wholesale Sales m/m | 2.00% | ||

| USD | Philly Fed Manufacturing Index | -1.1 | -2.8 | ||

| USD | Unemployment Claims | 267K | 259K | ||

| USD | Current Account | -115B | -124B | ||

| 16:00 | USD | JOLTS Job Openings | 5.60M | 5.61M | |

| USD | CB Leading Index m/m | 0.20% | -0.20% | ||

| 16:30 | USD | Natural Gas Storage | |||

| 18-Mar | 01:50 | JPY | Monetary Policy Meeting Minutes | ||

| 09:00 | EUR | German PPI m/m | -0.20% | -0.70% | |

| 14:00 | GBP | BOE Quarterly Bulletin | |||

| 14:30 | CAD | Core CPI m/m | 0.50% | 0.30% | |

| CAD | Core Retail Sales m/m | 0.70% | -1.60% | ||

| CAD | CPI m/m | 0.20% | 0.20% | ||

| CAD | Retail Sales m/m | 0.80% | -2.20% | ||

| 15:00 | USD | FOMC Member Dudley Speaks | |||

| 17:00 | USD | Prelim UoM Consumer Sentiment | 92.3 | 91.7 | |

| USD | FOMC Member Rosengren Speaks | ||||

| USD | Prelim UoM Inflation Expectations | 2.50% | |||

| 20:00 | USD | FOMC Member Bullard Speaks |

Time: GMT+2

Currencies/Events to Watch this Week

AUD: The monetary policy meeting minutes will be due on Tuesday but the release is not expected to impact the Aussie dollar a lot, given the RBA’s rather neutral stand. On Thursday, the Australian employment data will be released. On a monthly basis, the economy is expected to have added 12.3k jobs, following a decline -7.9k previously. Australian unemployment rate is expected to remain unchanged at 6.0%. The RBA will also be releasing its monetary policy bulletin.

NZD: The week ahead will see a speech from RBNZ Governor Wheeler late Monday. Global dairy price index numbers are due on Tuesday followed by the New Zealand quarterly GDP numbers for Q4 of 2015. Forecasts call for a slower pace of increase of 0.70%, down from 0.90% previously. With the RBNZ cutting rates last week and noting that further rate cuts are possible, weaker growth could likely raise speculation of further RBNZ action over the coming months.

JPY: The Bank of Japan’s monetary policy meeting is due next week on Tuesday and it will be followed up by a press conference from the BoJ. It is widely expected that the BoJ will not cut rates further following its January’s surprise rate cut. However, options are open for potential expansion to the BoJ’s QQE. The USDJPY has remained flat for the most part last week and could remain so into the event with a potential for a breakout and establishing direction.

EUR: Following the ECB’s event last week data for the week ahead is limited to inflation numbers. French final CPI data is due on Tuesday with expectations that consumer prices grew at a pace of 0.20%, unchanged from the previous month. Eurozone quarterly employment change is also expected to show an increase of 0.20% from the previous quarter. Eurozone final CPI year over year is expected to fall -0.20% while the core CPI is expected to remain unchanged at 0.70%. The data is due on Thursday. Winding up the week will be the German producer prices index which is expected to show a decline of -0.20%. The Euro is likely to take a back seat as the Fed’s meeting looms.

GBP: It will be a busy week for the Pound Sterling. On Wednesday, unemployment numbers are due with the average earnings index expected to rise 2.0% following 1.90% growth seen in January. The unemployment rate is expected to remain unchanged at 5.10%. The UK will also be releasing its annual budget later in the day. Thursday, the Bank of England’s monetary policy is likely to remain a non-event with rates remaining at 0.50% while the MPC vote count is also expected to see no dissenters voting for rate hikes.

CHF: The Swiss National Bank holds its quarterly monetary policy meeting this week. Expectations are strongly in favor of the SNB keeping the Libor rates unchanged at -0.75%. Few weeks ago SNB Chairman Thomas Jordan noted that the negative interest rates have a limited impact implying that the SNB could hold rates steady without further rate cuts. On the exchange rate, expect the usual rhetoric from the SNB calling the Swiss Franc overvalued.

CAD: Data from Canada will see the manufacturing sales and foreign securities purchases due on Wednesday. More importantly, consumer inflation and retail sales figures will be released on Friday. Expectations are that consumer inflation increased 0.50% in February, up from 0.30% increase in January on the core while the headline inflation is expected to remain unchanged at 0.20%. Retail sales numbers are forecasted to rise 0.70% on the core and 0.80% on the headline number.

USD: It will be a busy week for the US Dollar with retail sales and consumer inflation numbers coming out earlier in the week. Retail sales expectations are dovish while consumer inflation is expected to fall -0.20% for the month on the headline and rise a meager 0.10% on the core for the month. The big event for the US Dollar will of course be the FOMC meeting on Wednesday. Rates are expected to remain unchanged and the Fed will be holding a press conference and also releasing its new economic forecasts. Expect to see volatility into the event.