Today’s Economic events

- Japan retail sales y/y -0.10% vs. 0.20%

- Japan preliminary industrial production m/m 3.70% vs. 3.20%

- Australia MI Inflation gauge m/m -0.20% vs. 0.40% previously

- Australia company operating profits q/q -2.80% vs. -1.70%

- Australia private sector credit m/m 0.50% vs. 0.50%

- Japan housing starts y/y 0.20% vs. -0.20%

- Germany retail sales m/m 0.70% vs. 0.30%

- German import prices m/m -1.50% vs. -0.90%

- Swiss KOF Economic barometer 102.4 s. 99.1

- UK Net lending to individuals m/m 5.3bn vs. 5.2bn

- UK M4 money supply m/m 0.0% vs. 0.30%

- Eurozone CPI flash estimates y/y -0.20% vs. 0.0%

- Eurozone core CPI flash estimates y/y 0.70% vs. 0.90%

- Italy preliminary CPI m/m -0.2% vs. 0.10%

- Canada current account -15.4bn vs. -16.8bn

- Canada RMPI m/m -0.40% vs. -3.2%; IPPI m/m 0.50% vs. 0.10%

Coming up

- Chicago PMI

- US Pending home sales m/m

- New Zealand overseas trade index

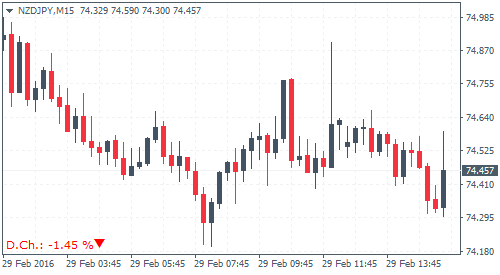

Chart of the day – NZDJPY

The markets opened today following the comments from the G20 summit held over the weekend. While there were no concrete steps taken to tone down the current market uncertainty, the G20 members, however, acknowledged the growing risks to economic growth. The Yen strengthened at the open with USDJPY falling to session lows of 112.76 before attempting to reverse. The risk aversion saw the Asian markets all closing in the Red. The Nikkei225 was down -1.0% with the Shanghai Composite down -2.87% for the day.

Gold prices remained supported as the precious metal climbed steadily since the open following Friday’s decline to the lows of 1213. Gold is currently trading at $1227 an ounce, up 0.38% for the day.

The commodity risk currencies were steady with AUDUSD trading at $0.714, up 0.12% for the day. The Aussie remains at risk ahead of tomorrow’s RBA rate decision as well as other key economic releases including building approvals. The NZDUSD is weaker today, down -0.68% for the day as the Kiwi continued to trend lower. Prices briefly tested session highs above 0.6615 but the failure to hold on the gains saw the Kiwi trending lower.

In the Eurozone, flash inflation estimates released earlier today showed a decline in consumer prices by -0.20% in February on the headline while core inflation rate rose less than expected at 0.70%, down from 1.0% a month ago. The continued decline in Eurozone inflation is likely to keep the pressure on the ECB as the Central Bank meets on March 10th. The Euro remained weaker against the Dollar since the Asian trading session as EURUSD is trading at $1.087, down -0.53% at the time of writing.

[Tweet “WTI Crude Oil is up 1.0% for the day, trading at $33 a barrel after $34.45 on Friday”]

The British Pound continues with its declines. GBPUSD is down -0.04% for the day. The declines came about as opinion polls showed that the Brexit’s ‘Out’ campaign was leading with 53% votes, against the ‘In’ campaign which is trailing at 48%. There is still a large group of voters who are undecided which could change the course of the outcome. The G20 members also mentioned the risks of Britain exiting from the EU but it did little to stem the declines. The European equity markets are also lower today. The German DAX is down -1.04% while the London FTSE100 is down -0.23% lower.

The NY trading session opened on a quiet note. Economic data due later in the day includes the Chicago PMI and the US pending home sales numbers followed by New Zealand overseas trade index data. US pre-market futures show a lower open with the Dow Jones down -0.10% and the S&P500 futures down -0.04%

WTI Crude Oil prices are up 1.0% for the day, trading at $33 a barrel after prices touched a high of $34.45 on Friday before giving back the gains to close Friday’s session at $32.85.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)