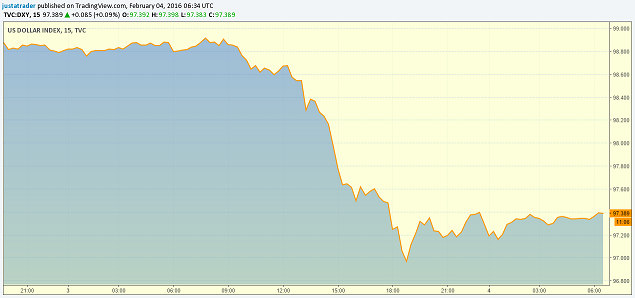

The US Dollar saw one of the strongest intraday sell-off during the NY trading session yesterday, losing over -1.52% for the day. The US Dollar Index, which opened at 98.82, closed the day at 97.30. Yesterday’s declines are only second to the -2.10% decline seen on December 3rd when the ECB failed to expand its QE.

Yesterday’s decline was however marked by the fact that almost all the major currencies posted strong gains.

| Currency | %age Change | Currency | %age Change |

| AUDUSD | +1.90% | NZDUSD | +2.27% |

| EURUSD | +1.70% | GBPUSD | +1.35% |

| USDJPY | -1.75% | USDCAD | -1.96% |

| USDCHF | -1.35% | Gold | +1.19% |

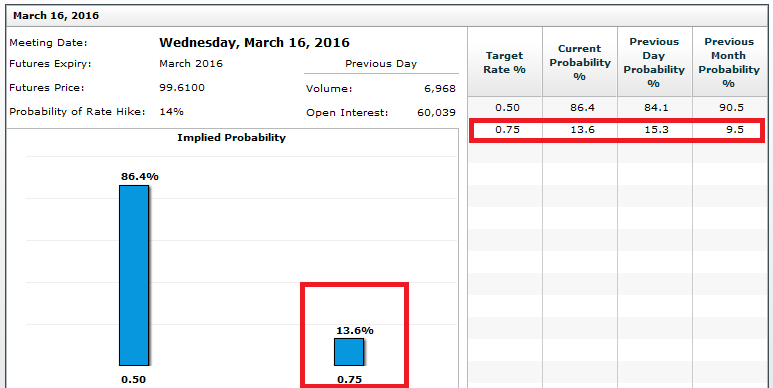

The Greenback declined sharply as falling interest rates in the US coupled with concerns about global economic growth saw the markets almost crush some of the most popular trades. The markets gained momentum in early European trading where the Kiwi started its ascent. Boosted by better unemployment numbers and hawkish tone in RBNZ Governor Wheeler’s speech, the NZD rallied as speculators cut short their bets on further RBNZ easing. USDJPY fell back to 117Yen, pre-BoJ levels completely erasing all the gains made after the BoJ’s surprise negative rates. By the NY trading session, despite a better than expected ADP private payrolls data, the markets shrugged off the news as ISM numbers for January remained weak, leading to reduced expectations on the pace of the US Fed rate hikes this year. At the time of writing, the Fed funds futures rate expectations are currently pricing in only one rate hike this year. In early January, expectations for March rate hikes fell to around 35% and at the time of writing, the expectations further deteriorated to just under than 15%.

The weaker US Dollar’s impact was so profound that even Crude Oil managed to gain in yesterday’s turmoil, gaining 10.60% to settle at $32.72 a barrel. The gains came about despite yesterday’s weekly Crude Oil inventory report showed a larger than expected build-up of the US stockpiles, which surged 7.8 Million barrels, following an 8.4 Million barrels from a week before.

Gold prices were also trending stronger with a total year to date gains of over 7.0%.

US NFP could turn the sentiment

With the ISM manufacturing into the fourth month of contraction and the effects being seen on weaker non-manufacturing (services) PMI as well, the markets are likely to turn their attention to the January jobs report. We noted earlier this week that US economic data would be scrutinized closely and the NFP will no doubt garner the most of the attention. Expectations are fairly modest, with no change to the US unemployment rate, which currently stands at 5.0%. The monthly job gains are expected to average around 186k – 189k, a rather soft print off December’s 292k addition.

Failing to meet the NFP expectations could most likely cement further downside bias in the US Dollar and could result in pushing other currencies higher. Such a move in the markets could result in various Central Banks likely to come out strongly dovish, as seen earlier today with BoJ’s Kuroda attempting to soothe the markets by stating that the Japanese Central Bank has enough room to expand its QQE as well as further pushing down its negative interest rates.

However, as a silver lining, the US equity markets showed signs of a rebound as the US Dollar weakened last night. The US Dow Jones Industrial rose 1.13% while the S&P500 closed with 0.50% gains. Of course, the question now remains if this Friday’s jobs report will help the markets to recover, or there could be more of what the markets saw yesterday.