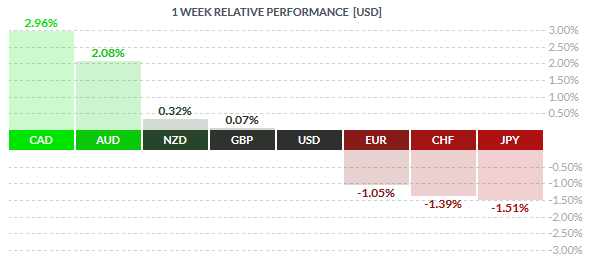

The commodity risk currencies managed to emerge on the top last week in a mid-week rally. The markets turned around after ECB President Mario Draghi hinted at more stimulus expansion at the meeting in March. The Canadian dollar closed the week with 2.96% gains as the Bank of Canada left interest rates unchanged against expectations of a 25bps rate cut. Oil prices also bounced back strongly last week supporting the CAD. The Australian Dollar was the second top performer, gaining 2.08% for the week on the risk-on sentiment.

On the other side of the scale, the Yen was the weakest, losing -1.51% for the week followed by the Swiss Franc which lost -1.39% for the week as investors shed the safe haven currencies as equity markets rallied. The Euro also came under pressure last week, losing -1.05% against the US Dollar, mostly on dovish comments from Draghi.

Fundamentals for the Week 25/01 – 29/01

| Date | Time | Currency | Detail | Forecast | Previous |

| 25-Jan | 01:50 | JPY | Trade Balance | 0.00T | |

| 11:00 | EUR | German Ifo Business Climate | 108.5 | 108.7 | |

| EUR | Italian Retail Sales m/m | 0.20% | -0.30% | ||

| 20:00 | EUR | ECB President Draghi Speaks | |||

| All Day | AUD | Bank Holiday | |||

| 26-Jan | 01:50 | JPY | SPPI y/y | 0.20% | 0.20% |

| 04:00 | NZD | Credit Card Spending y/y | 8.50% | ||

| 09:00 | CHF | Trade Balance | 3.33B | 3.14B | |

| 12:45 | GBP | BOE Gov Carney Speaks | |||

| 16:00 | USD | HPI m/m | 0.40% | 0.50% | |

| USD | S&P/CS Composite-20 HPI y/y | 5.70% | 5.50% | ||

| 16:45 | USD | Flash Services PMI | 53.9 | 54.3 | |

| 17:00 | USD | CB Consumer Confidence | 96.6 | 96.5 | |

| USD | Richmond Manufacturing Index | 3 | 6 | ||

| 27-Jan | 01:30 | AUD | MI Leading Index m/m | -0.20% | |

| 02:30 | AUD | CPI q/q | 0.30% | 0.50% | |

| AUD | Trimmed Mean CPI q/q | 0.50% | 0.30% | ||

| 09:00 | CHF | UBS Consumption Indicator | 1.66 | ||

| EUR | GfK German Consumer Climate | 9.3 | 9.4 | ||

| 16:00 | USD | New Home Sales | 503K | 490K | |

| Tentative | CNY | CB Leading Index m/m | 0.60% | ||

| 17:30 | USD | Crude Oil Inventories | 4.0M | ||

| 21:00 | USD | FOMC Statement | |||

| USD | Federal Funds Rate | <0.50% | <0.50% | ||

| 22:00 | NZD | Official Cash Rate | 2.50% | 2.50% | |

| NZD | RBNZ Rate Statement | ||||

| 23:45 | NZD | Trade Balance | -130M | -779M | |

| 28-Jan | 01:50 | JPY | Retail Sales y/y | 0.20% | -1.10% |

| 02:30 | AUD | Import Prices q/q | -0.80% | 1.40% | |

| 09:00 | EUR | German Import Prices m/m | -1.00% | -0.20% | |

| All Day | EUR | German Prelim CPI m/m | -0.80% | -0.10% | |

| 10:00 | EUR | Spanish Unemployment Rate | 21.30% | 21.20% | |

| 11:30 | GBP | Prelim GDP q/q | 0.50% | 0.40% | |

| GBP | Index of Services 3m/3m | 0.60% | 0.50% | ||

| 13:00 | GBP | CBI Realized Sales | 18 | 19 | |

| 15:30 | USD | Core Durable Goods Orders m/m | 0.00% | -0.10% | |

| USD | Unemployment Claims | 281K | 293K | ||

| USD | Durable Goods Orders m/m | -0.70% | 0.00% | ||

| 17:00 | USD | Pending Home Sales m/m | 1.10% | -0.90% | |

| 17:30 | USD | Natural Gas Storage | -178B | ||

| 23:45 | NZD | Building Consents m/m | 1.80% | ||

| 29-Jan | 01:30 | JPY | Household Spending y/y | -2.30% | -2.90% |

| JPY | Tokyo Core CPI y/y | 0.10% | 0.10% | ||

| JPY | National Core CPI y/y | 0.10% | 0.10% | ||

| JPY | Unemployment Rate | 3.30% | 3.30% | ||

| 01:50 | JPY | Prelim Industrial Production m/m | -0.30% | -0.90% | |

| 02:05 | GBP | GfK Consumer Confidence | 1 | 2 | |

| 02:30 | AUD | PPI q/q | 0.60% | 0.90% | |

| AUD | Private Sector Credit m/m | 0.60% | 0.40% | ||

| Tentative | JPY | Monetary Policy Statement | |||

| 07:00 | JPY | BOJ Outlook Report | |||

| JPY | BOJ Core CPI y/y | 1.20% | 1.20% | ||

| JPY | Housing Starts y/y | 0.50% | 1.70% | ||

| 08:30 | EUR | French Prelim GDP q/q | 0.20% | 0.30% | |

| Tentative | JPY | BOJ Press Conference | |||

| 09:00 | EUR | German Retail Sales m/m | 0.30% | 0.20% | |

| 09:45 | EUR | French CPI m/m | |||

| EUR | French Consumer Spending m/m | 0.80% | -1.10% | ||

| 10:00 | CHF | KOF Economic Barometer | 95.9 | 96.6 | |

| EUR | Spanish Flash CPI y/y | 0.10% | 0.00% | ||

| EUR | Spanish Flash GDP q/q | 0.80% | 0.80% | ||

| 11:00 | EUR | M3 Money Supply y/y | 5.20% | 5.10% | |

| EUR | Private Loans y/y | 1.50% | 1.40% | ||

| 12:00 | EUR | CPI Flash Estimate y/y | 0.40% | 0.20% | |

| EUR | Core CPI Flash Estimate y/y | 0.90% | 0.90% | ||

| 15:30 | CAD | GDP m/m | 0.00% | ||

| CAD | RMPI m/m | -4.00% | |||

| CAD | IPPI m/m | -0.20% | |||

| USD | Advance GDP q/q | 0.80% | 2.00% | ||

| USD | Advance GDP Price Index q/q | 1.20% | 1.30% | ||

| USD | Employment Cost Index q/q | 0.60% | 0.60% | ||

| USD | Goods Trade Balance | -60.0B | -60.5B | ||

| 16:45 | USD | Chicago PMI | 45.4 | 42.9 | |

| 17:00 | USD | Revised UoM Consumer Sentiment | 93.1 | 93.3 | |

| USD | Revised UoM Inflation Expectations | 2.40% |

Time: GMT+2

Currencies/Events to Watch this Week

AUD: Australia quarterly inflation numbers are the main event to watch for next week. Expectations are dovish with the fourth quarter CPI expected to rise 0.30%, against 0.50% inflation lodged in the third quarter. With New Zealand’s inflation dipping into the negative last week, there could be a possibility for Australian inflation numbers to post negative reading as well. Besides inflation, Producer Price index is also due with expectations of a slowdown to 0.60% against 0.90% increase a quarter before. Overall, the Australian markets will be seeing a short trading week with the markets closed on January 26th on account of Australia Day.

NZD: The RBNZ will be the main event risk for the Kiwi next week. Expectations are currently flat with the RBNZ likely to hold on to rate cuts at the meeting this week, keeping the RBNZ official cash rate unchanged at 2.50%. The RBNZ’s statement will be key in this aspect especially in light of weaker than expected inflation data seen a week ago. Besides the RBNZ rate decision, building consents and visitor arrivals are the other data points to look forward to during the week.

JPY: Japan inflation data will be released next week alongside retail sales numbers. However, the main event will be the Bank of Japan which is due to meet on the 29th January. The Yen gave back its gains last Friday with markets starting to price in a possible BoJ easing during the week with the Yen flirting near 116 levels and based on the assumption that a stronger Yen would hurt Japan exports while also put a drag on inflation via the imports on a stronger Yen. However, the BoJ’s decision could be a close call nonetheless.

EUR: After last week’s ECB meeting where Mario Draghi signaled a potential policy announcement at the March meeting, the week ahead is relatively quiet for the Euro. Draghi is due to speak on Monday and as seen during the December meeting, dovish talk from the ECB officials is likely to repeat itself. Besides, the speech from Draghi, German retail sales and France quarterly GDP numbers are on the tap next week.

GBP: The UK will see the first/preliminary GDP data for the fourth quarter of 2015. Expectations are for the UK’s GDP to have increased 0.50%, up from 0.40% growth lodged during the third quarter. Over the week, BoE’s Carney is again slated to speak and could pose some event risk to the British Pound which managed to form a base last week.

CAD: Canadian GDP data is due for release on January 29th and expectations are flat for the monthly GDP data after growth in the Canadian economy contracted -0.50% a month prior. Besides the GDP data, the economic data from Canada is light with no other major releases expected.

USD: The main event next week will be the FOMC rate decision due on January 27th. No changes to the Fed funds rate is expected at this meeting as the Fed is likely to wait for more data after hiking rates in December. Also during the week, Core durable goods orders are due followed by the preliminary GDP data which is expected to show that the US economy grew at a slower pace of 0.80% in the final quarter of 2015 after rising 2.0% in Q3.