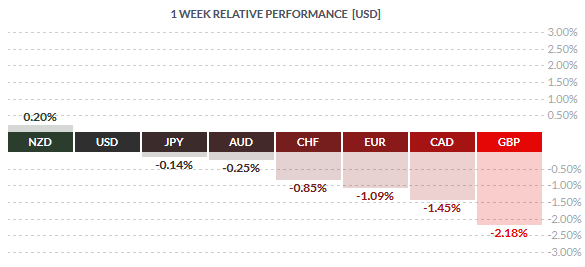

The New Zealand Dollar was the top performing currency last week closing with gains of 0.20%. The Kiwi came out tops with not much of fundamentals going in its favor. While most of the commodity risk currencies came under pressure last week, the NZD outperformed its peers. The US Dollar was the second best currency last week. The Dollar gained as the US Federal Reserve raised interest rates by 25bps and signaling a gradual rate hike in 2016.

The British Pound was the weakest, losing -2.18% for the week despite a better than expected retail sales numbers and the UK’s unemployment rate falling to 5.20%. It was wages which rose less than expected at 2.40%. Wages was a big concern for the BoE where last week, BoE member, Shafik noted that unless there was strong evidence of UK wages growing, rate hikes would likely to remain at the current levels. The Canadian dollar lost -1.45% for the week led by weak inflation and GDP numbers and falling Oil prices.

Fundamentals for the Week 21/12 – 25/12

| Date | Time | Currency | Detail | Forecast | Previous |

| 21-Dec | 04:00 | NZD | Credit Card Spending y/y | 7.80% | |

| 06:30 | JPY | All Industries Activity m/m | 0.90% | -0.20% | |

| 07:00 | JPY | BOJ Monthly Report | |||

| 09:00 | EUR | German PPI m/m | -0.20% | -0.40% | |

| 13:00 | EUR | German Buba Monthly Report | |||

| GBP | CBI Realized Sales | 22 | 7 | ||

| 17:00 | EUR | Consumer Confidence | -6 | -6 | |

| 22-Dec | 02:05 | GBP | GfK Consumer Confidence | 1 | 1 |

| 04:00 | CNY | CB Leading Index m/m | 0.60% | ||

| 09:00 | CHF | Trade Balance | 3.82B | 4.16B | |

| EUR | German Import Prices m/m | 0.20% | -0.30% | ||

| EUR | GfK German Consumer Climate | 9.3 | 9.3 | ||

| 11:30 | GBP | Public Sector Net Borrowing | 11.9B | 7.5B | |

| 15:30 | USD | Final GDP q/q | 1.90% | 2.10% | |

| USD | Final GDP Price Index q/q | 1.30% | 1.30% | ||

| 16:00 | EUR | Belgian NBB Business Climate | -4 | -3.9 | |

| USD | HPI m/m | 0.40% | 0.80% | ||

| 17:00 | USD | Existing Home Sales | 5.32M | 5.36M | |

| USD | Richmond Manufacturing Index | -1 | -3 | ||

| 23:45 | NZD | Trade Balance | -812M | -963M | |

| 23-Dec | 09:45 | EUR | French Consumer Spending m/m | 0.20% | -0.70% |

| 10:00 | CHF | KOF Economic Barometer | 98.9 | 97.9 | |

| 11:30 | GBP | Current Account | -21.3B | -16.8B | |

| GBP | Final GDP q/q | 0.50% | 0.50% | ||

| GBP | Index of Services 3m/3m | 0.60% | 0.70% | ||

| GBP | Revised Business Investment q/q | 2.20% | 2.20% | ||

| 12:00 | EUR | Italian Retail Sales m/m | 0.30% | -0.10% | |

| 15:30 | CAD | Core Retail Sales m/m | -0.50% | ||

| CAD | GDP m/m | -0.50% | |||

| CAD | Retail Sales m/m | -0.50% | |||

| USD | Core Durable Goods Orders m/m | 0.10% | 0.50% | ||

| USD | Core PCE Price Index m/m | 0.10% | 0.00% | ||

| USD | Durable Goods Orders m/m | -0.60% | 3.00% | ||

| USD | Personal Spending m/m | 0.30% | 0.10% | ||

| USD | Personal Income m/m | 0.20% | 0.40% | ||

| 17:00 | USD | New Home Sales | 507K | 495K | |

| USD | Revised UoM Consumer Sentiment | 92.1 | 91.8 | ||

| USD | Revised UoM Inflation Expectations | 2.60% | |||

| 17:30 | USD | Crude Oil Inventories | 4.8M | ||

| 24-Dec | 01:00 | AUD | CB Leading Index m/m | -0.10% | |

| 01:50 | JPY | Monetary Policy Meeting Minutes | |||

| 11:30 | GBP | BBA Mortgage Approvals | 46.2K | 45.4K | |

| 15:30 | USD | Unemployment Claims | 270K | 271K | |

| 25-Dec | 01:30 | JPY | Household Spending y/y | -2.10% | -2.40% |

| JPY | Tokyo Core CPI y/y | 0.10% | 0.00% | ||

| JPY | National Core CPI y/y | 0.00% | -0.10% | ||

| JPY | Unemployment Rate | 3.20% | 3.10% | ||

| 01:50 | JPY | SPPI y/y | 0.40% | 0.50% | |

| 07:00 | JPY | BOJ Core CPI y/y | 1.20% | 1.20% | |

| JPY | Housing Starts y/y | 0.90% | -2.50% |

Time: GMT+2

Currencies/Events to Watch this Week

The week ahead will mark the start of the holiday season with most of the institutional banks closing business on account of Christmas. Data is largely limited and the holiday-shortened week will see the markets wind up by Wednesday with most of the markets across the globe being closed from Thursday onwards. Most of the US and Canadian data will be released on Wednesday, 23rd December ahead of the market close for the remainder of the week.

From Asia-Pacific region, data from Australia is limited to the CB leading index. However, this data is unlikely to see any big moves coming into the markets. On December 21st, New Zealand trade balance data will be released and credit card spending. Expect some moves on credit card spending data which saw the Kiwi bounce strongly during the last release.

It will be a somewhat short but busy week for the Eurozone. Monday’s data includes German PPI numbers followed by Tuesday’s German import prices and Gfk consumer expectations. However, despite the data, it is unlikely to see any significant moves in the market this coming week.

The British Pound will be looking to the final quarterly revised GDP which currently stands at 0.50% at the second revision. An upside surprise to see the British Pound book some gains, but it unlikely to impact the markets much.

On Tuesday, 22nd December the US final GDP data will be released. Expectations are slightly dovish with the GDP expected to be revised down to 1.90% against second estimates of 2.10%. Canada’s GDP numbers will be released on 23rd December. As of the previous month, Canadian economy contracted -0.50% and puts the economy on the risk of a technical recession. Core retail sales numbers will also be released at the same time while the US durable goods orders are expected to increase 0.10% after a 0.50% increase a month ago.