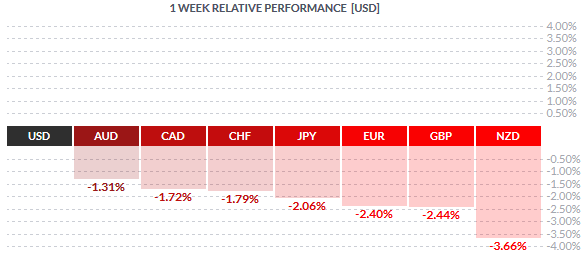

The US Dollar cemented its position as the strongest currency on the back of interest rate/monetary policy divergence. With the Fed now increasingly likely to hike rates in December, Friday’s stellar jobs report has made the December rate hikes very much a possibility. The Dollar continues to trade strong ever since the FOMC’s hawkish October meeting and comments from Janet Yellen last week as she testified to the Congress on the Federal Reserve’s intentions to hike rates at the December meeting.

The British Pound erased gains from last week losing -2.44% for the week as the Bank of England came out on a dovish tone noting that inflation would remain near 1.0% into 2016. The dovish comments saw traders scale back their bets on an earlier rate hike increase in 2016, now pushed back to 2017. The Kiwi dollar was the weakest currency however as fundamentals start to come back into the picture. NZDUSD lost -3.66% for the week on a weak unemployment report and Global Dairy trade index which has turned negative on the past two releases.

Fundamentals for the Week 09/11 – 13/11

| Date | Time | Currency | Detail | Forecast | Previous |

| 09-Nov | 02:30 | AUD | ANZ Job Advertisements m/m | 3.90% | |

| 03:30 | JPY | Average Cash Earnings y/y | 0.50% | 0.40% | |

| 09:00 | EUR | German Trade Balance | 22.3B | 19.6B | |

| 11:30 | EUR | Sentix Investor Confidence | 12.4 | 11.7 | |

| All Day | EUR | Eurogroup Meetings | |||

| 15:15 | CAD | Housing Starts | 198K | 232K | |

| 17:00 | USD | Labor Market Conditions Index m/m | 0 | ||

| 10-Nov | 01:50 | JPY | Current Account | 1.50T | 1.59T |

| JPY | Bank Lending y/y | 2.60% | |||

| 02:01 | GBP | BRC Retail Sales Monitor y/y | 2.60% | ||

| 02:30 | AUD | NAB Business Confidence | 5 | ||

| AUD | Home Loans m/m | 0.10% | 2.90% | ||

| 03:30 | CNY | CPI y/y | 1.50% | 1.60% | |

| CNY | PPI y/y | -5.90% | -5.90% | ||

| 07:00 | JPY | Economy Watchers Sentiment | 48.2 | 47.5 | |

| 08:45 | CHF | Unemployment Rate | 3.40% | 3.40% | |

| 09:45 | EUR | French Industrial Production m/m | 0.10% | 1.60% | |

| 10th-17th | CNY | M2 Money Supply y/y | 13.10% | ||

| 11:00 | EUR | Italian Industrial Production m/m | 0.60% | -0.50% | |

| All Day | EUR | ECOFIN Meetings | |||

| 13:00 | USD | NFIB Small Business Index | 96.4 | 96.1 | |

| 15:30 | USD | Import Prices m/m | 0.00% | -0.10% | |

| 10th-13th | USD | Mortgage Delinquencies | 5.30% | ||

| 17:00 | USD | Wholesale Inventories m/m | 0.10% | 0.10% | |

| 19:00 | CAD | Gov Council Member Wilkins Speaks | |||

| 22:00 | NZD | RBNZ Financial Stability Report | |||

| 22:05 | NZD | RBNZ Gov Wheeler Speaks | |||

| 11-Nov | 01:30 | AUD | Westpac Consumer Sentiment | 4.20% | |

| 01:50 | JPY | M2 Money Stock y/y | 3.80% | 3.80% | |

| 07:30 | CNY | Industrial Production y/y | 5.80% | 5.70% | |

| CNY | Fixed Asset Investment ytd/y | 10.20% | 10.30% | ||

| CNY | Retail Sales y/y | 10.90% | 10.90% | ||

| 08:00 | JPY | Prelim Machine Tool Orders y/y | -19.10% | ||

| 09:00 | EUR | German WPI m/m | 0.20% | -0.60% | |

| 11:30 | GBP | Average Earnings Index 3m/y | 3.20% | 3.00% | |

| GBP | Claimant Count Change | 1.6K | 4.6K | ||

| GBP | Unemployment Rate | 5.40% | 5.40% | ||

| 12:30 | GBP | BOE Gov Carney Speaks | |||

| 15:15 | EUR | ECB President Draghi Speaks | |||

| 23:30 | NZD | Business NZ Manufacturing Index | 55.4 | ||

| 23:45 | NZD | FPI m/m | -0.50% | ||

| 12-Nov | 01:50 | JPY | Core Machinery Orders m/m | 3.40% | -5.70% |

| JPY | PPI y/y | -3.50% | -3.90% | ||

| 02:00 | AUD | MI Inflation Expectations | 3.50% | ||

| 02:30 | AUD | Employment Change | 15.2K | -5.1K | |

| AUD | Unemployment Rate | 6.20% | 6.20% | ||

| 09:00 | EUR | German Final CPI m/m | 0.00% | 0.00% | |

| 09:45 | EUR | French CPI m/m | 0.10% | -0.40% | |

| 12:00 | EUR | Industrial Production m/m | -0.10% | -0.50% | |

| 15:00 | CAD | Gov Council Member Wilkins Speaks | |||

| 15:30 | CAD | NHPI m/m | 0.20% | 0.30% | |

| USD | Unemployment Claims | 276K | |||

| 17:00 | USD | JOLTS Job Openings | 5.37M | ||

| 17:15 | USD | FOMC Member Evans Speaks | |||

| 18:00 | USD | Crude Oil Inventories | 2.8M | ||

| 19:15 | USD | FOMC Member Dudley Speaks | |||

| 21:00 | USD | Federal Budget Balance | -130.2B | 91.1B | |

| 13-Nov | 06:30 | JPY | Revised Industrial Production m/m | 1.00% | 1.00% |

| JPY | Tertiary Industry Activity m/m | 0.20% | 0.10% | ||

| 08:30 | EUR | French Prelim GDP q/q | 0.30% | 0.00% | |

| 09:00 | EUR | German Prelim GDP q/q | 0.30% | 0.40% | |

| 09:45 | EUR | French Prelim Non-Farm Payrolls q/q | 0.10% | 0.20% | |

| 10:15 | CHF | PPI m/m | -0.20% | -0.10% | |

| 11:00 | EUR | Italian Prelim GDP q/q | 0.30% | 0.20% | |

| 11:30 | GBP | Construction Output m/m | 1.60% | -4.30% | |

| 12:00 | EUR | Flash GDP q/q | 0.40% | ||

| EUR | Trade Balance | 19.4B | 19.8B | ||

| 15:30 | USD | Core Retail Sales m/m | 0.40% | -0.30% | |

| USD | PPI m/m | 0.10% | -0.50% | ||

| USD | Retail Sales m/m | 0.30% | 0.10% | ||

| USD | Core PPI m/m | 0.20% | -0.30% | ||

| 16:30 | GBP | CB Leading Index m/m | 0.20% | ||

| 17:00 | USD | Prelim UoM Consumer Sentiment | 91.2 | 90 | |

| USD | Business Inventories m/m | 0.10% | 0.00% | ||

| USD | Prelim UoM Inflation Expectations | 2.70% |

Time: GMT+2

Currencies/Events to Watch this Week

China Inflation Data: Inflation numbers from China is due this week with expectations that inflation declined to 1.5% from 1.6% previously. The producer price index is expected to stay put at -5.9%, same as a month ago. Other data includes industrial production which is expected to post a modest increase of 5.8%, from 5.7% previously. Inflation data will be the main event for the global currencies as a miss on inflation could see a panic risk aversion mode take over the markets.

Australia Jobs Report: The monthly jobs numbers from Australia is due this week and no major changes are expected with the unemployment rate expected to stay put at 6.2%. The monthly employment change is expected to rise 15.2k, after declining -5.1k. The Australian dollar has been largely stable last week with the exception of the stronger US Dollar but has managed to perform fairly well against other currencies. A beat on the estimates could put the Aussie back into the driving seat again with the exception of the US Dollar. Besides the labour market data, other economic releases includes the monthly home loans which is expected to rise 0.1%, a soft print after previous month’s 2.9% after most of the big lenders hiked mortgage rates over the month.

Germany GDP: The week ahead is relatively quiet for the Eurozone with the only major releases including the German GDP number which is expected to rise 0.3% month on month. Eurozone flash GDP numbers are also due with last quarter’s GDP data increasing 0.4%. ECB President Mario Draghi is due to speak at the Bank of London and the markets will be monitoring any references to monetary policy.

UK Jobs: The monthly labor market numbers from the UK is due this week. Expectations are for the unemployment rate to remain unchanged at 5.4% while the average hourly earnings are once again bullish with estimates of 3.2% increase. Last month’s average hourly earnings increased to 3.0% but missed estimates. A beat on the two data points could help the British Pound recover some of its declines from last week.

RBNZ Financial Stability Report: The RBNZ’s financial stability report is due this week and which could keep the markets on the edge. RBNZ Governor Wheeler is also expected to speak this week, but with the Kiwi now taking a plunge, the markets do not expect much of verbal talk down from the RBNZ Governor.

US Retail Sales: After enjoying a fairly bullish week, the US Dollar looks to the retail sales numbers this week. Expectations are for the core retail sales to have increased 0.4% while the headline retail sales numbers are expected to increase a modest growth of 0.3%. The monthly producer price index is also due and is expected to rise 0.2% on the core and 0.1% on the headline. A bullish print in the PPI could likely signal a positive CPI reading in the coming weeks or next month. The week winds up with the UoM consumer sentiment on Friday with modest expectations of an increase of 91.2

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)