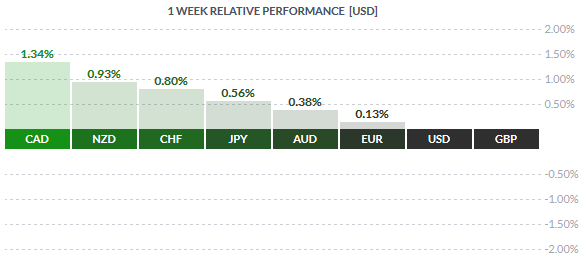

The US Dollar gave up its gains built over the week on Friday as disappointing nonfarm payrolls saw investors shedding the US Dollar. Risky assets gained with Canadian dollar posting the strongest gains of the week rising 1.34%. The gains in the Canadian dollar were also supported by Crude Oil prices which posted modest gains for the week despite trading largely flat. The Kiwi dollar close the week with gains of 0.93%, despite the lack of any clear fundamentals supporting the New Zealand dollar, but was mostly due to the weaker US Dollar.

The British Pound was flat for the week but looks poised to recover from its previous week’s sharp declines. The Euro failed to capitalize on the USD’s weakness gaining only 0.13% for the week.

Fundamentals for the Week 05/10 – 09/10

| Date | Time | Currency | Detail | Forecast | Previous |

| 05-Oct | 01:30 | AUD | AIG Services Index | 55.6 | |

| 02:30 | AUD | MI Inflation Gauge m/m | 0.10% | ||

| 03:30 | AUD | ANZ Job Advertisements m/m | 1.00% | ||

| 04:30 | JPY | Average Cash Earnings y/y | 0.70% | 0.90% | |

| 10:15 | EUR | Spanish Services PMI | 59.7 | 59.6 | |

| 10:45 | EUR | Italian Services PMI | 54.8 | 54.6 | |

| 10:50 | EUR | French Final Services PMI | 51.2 | 51.2 | |

| 10:55 | EUR | German Final Services PMI | 54.4 | 54.3 | |

| 11:00 | EUR | Final Services PMI | 54 | 54 | |

| 11:30 | EUR | Sentix Investor Confidence | 12.2 | 13.6 | |

| GBP | Services PMI | 56.4 | 55.6 | ||

| 12:00 | EUR | Retail Sales m/m | -0.10% | 0.40% | |

| Day 1 | EUR | Eurogroup Meetings | |||

| 16:45 | USD | Final Services PMI | 55.7 | 55.6 | |

| 17:00 | USD | ISM Non-Manufacturing PMI | 58 | 59 | |

| USD | Labor Market Conditions Index m/m | 2.1 | |||

| 06-Oct | 00:00 | NZD | NZIER Business Confidence | 5 | |

| 03:30 | AUD | Trade Balance | -2.36B | -2.46B | |

| 06:30 | AUD | Cash Rate | 2.00% | 2.00% | |

| AUD | RBA Rate Statement | ||||

| 09:00 | EUR | German Factory Orders m/m | 0.50% | -1.40% | |

| 6th-9th | GBP | Halifax HPI m/m | 2.70% | ||

| 10:15 | CHF | CPI m/m | 0.10% | -0.20% | |

| 11:10 | EUR | Retail PMI | 51.4 | ||

| 11:30 | GBP | Housing Equity Withdrawal q/q | -12.5B | -13.0B | |

| All Day | EUR | ECOFIN Meetings | |||

| Day 2 | EUR | Eurogroup Meetings | |||

| 15:30 | CAD | Trade Balance | -0.3B | -0.6B | |

| USD | Trade Balance | -42.2B | -41.9B | ||

| Tentative | NZD | GDT Price Index | 16.50% | ||

| 17:00 | CAD | Ivey PMI | 58 | ||

| USD | IBD/TIPP Economic Optimism | 44.6 | 42 | ||

| 20:00 | EUR | ECB President Draghi Speaks | |||

| 07-Oct | 00:30 | USD | FOMC Member Williams Speaks | ||

| 01:30 | AUD | AIG Construction Index | 53.8 | ||

| 02:01 | GBP | BRC Shop Price Index y/y | -1.40% | ||

| 03:00 | AUD | HIA New Home Sales m/m | -1.80% | ||

| Tentative | JPY | Monetary Policy Statement | |||

| 08:00 | JPY | Leading Indicators | 103.40% | 105.00% | |

| 09:00 | EUR | German Industrial Production m/m | 0.30% | 0.70% | |

| Tentative | JPY | BOJ Press Conference | |||

| 09:45 | EUR | French Trade Balance | -3.6B | -3.3B | |

| 10:00 | CHF | Foreign Currency Reserves | 540B | ||

| 11:30 | GBP | Manufacturing Production m/m | 0.50% | -0.80% | |

| GBP | Industrial Production m/m | 0.30% | -0.40% | ||

| Tentative | EUR | German 10-y Bond Auction | 0.69|1.2 | ||

| 15:30 | CAD | Building Permits m/m | -0.60% | ||

| 17:00 | GBP | NIESR GDP Estimate | 0.50% | ||

| 17:30 | USD | Crude Oil Inventories | 4.0M | ||

| 20:01 | USD | 10-y Bond Auction | 2.24|2.7 | ||

| 22:00 | USD | Consumer Credit m/m | 18.6B | 19.1B | |

| 08-Oct | 02:01 | GBP | RICS House Price Balance | 56% | 53% |

| 02:50 | JPY | Core Machinery Orders m/m | 3.10% | -3.60% | |

| JPY | Current Account | 1.28T | 1.32T | ||

| 06:45 | JPY | 30-y Bond Auction | 1.41|3.1 | ||

| 08:00 | JPY | BOJ Monthly Report | |||

| JPY | Economy Watchers Sentiment | 48.6 | 49.3 | ||

| 08:45 | CHF | Unemployment Rate | 3.40% | 3.30% | |

| 09:00 | EUR | German Trade Balance | 20.2B | 22.8B | |

| 14:00 | GBP | MPC Official Bank Rate Votes | 1-0-8 | 1-0-8 | |

| GBP | Monetary Policy Summary | ||||

| GBP | Official Bank Rate | 0.50% | 0.50% | ||

| GBP | Asset Purchase Facility | 375B | 375B | ||

| GBP | MPC Asset Purchase Facility Votes | 0-0-9 | 0-0-9 | ||

| 14:30 | EUR | ECB Monetary Policy Meeting Accounts | |||

| 15:15 | CAD | Housing Starts | 217K | ||

| 15:30 | CAD | NHPI m/m | 0.20% | 0.10% | |

| USD | Unemployment Claims | 274K | 277K | ||

| 21:00 | USD | FOMC Meeting Minutes | |||

| 22:30 | USD | FOMC Member Williams Speaks | |||

| 09-Oct | 03:30 | AUD | Home Loans m/m | 5.10% | 0.30% |

| 09:45 | EUR | French Gov Budget Balance | -79.8B | ||

| EUR | French Industrial Production m/m | 0.60% | -0.80% | ||

| 11:00 | EUR | Italian Industrial Production m/m | -0.30% | 1.10% | |

| 11:30 | GBP | Trade Balance | -10.0B | -11.1B | |

| GBP | Construction Output m/m | 1.10% | -1.00% | ||

| 15:30 | CAD | Employment Change | 12.0K | ||

| CAD | Unemployment Rate | 7.00% | |||

| USD | Import Prices m/m | -0.50% | -1.80% | ||

| 16:10 | USD | FOMC Member Lockhart Speaks | |||

| 17:00 | USD | Wholesale Inventories m/m | 0.10% | -0.10% | |

| 17:30 | CAD | BOC Business Outlook Survey | |||

| 20:30 | USD | FOMC Member Evans Speaks |

Time: GMT+3

Currencies/Events to Watch this Week

RBA interest rates: The RBA will convene this Tuesday, October 6th with expectations high that the central bank will leave interest rates unchanged at 2.0%. The data over the month has been broadly mixed but hasn’t declined drastically that would warrant a rate cut. The Aussie has managed to strengthen reasonably well in the past week which could be addressed in the RBA’s monetary statement as commodity prices remain pressured to the downside. A dovish narrative in the Australian Central bank statement could see some potential downside moves in the Aussie. However, the downside risks remain more of a short term dip.

BoJ Monetary policy: The consensus is finely divided as to whether the Bank of Japan will expand its QQE purchases or not. While the risks remain, an expansion to QQE will be somewhat contradictory to BoJ’s Kuroda who has so far maintained an optimistic view that Japan’s inflation would reach the 2% target range. The Japanese Yen has firmer in the past few weeks albeit trading flat for the most part. Should the BoJ stay put on policy, the Yen is likely to appreciate further in the near term.

ECB’s Draghi Speaks: There is not much going on for the Euro in terms of fundamentals this week. For the most part, the week ahead is busy with the services PMI data from various Eurozone economies and retail sales numbers. ECB Chief, Mario Draghi is due to speak on Tuesday, October 6th. While he has maintained a cautious approach at his speech earlier last week regarding the ECB expanding its QE plans, it will be interesting to see how Draghi will word his statement.

BoE Monetary Policy: The British Pound has weakened considerably over the past few weeks and the week ahead will pose another important risk from the BoE. While no change is expected, focus still remains if there will be other dissenters for a rate hike, which currently stands at 1. Various BoE officials have sounded hawkish in their speeches since last month’s BoE monetary policy meeting, but it will be left to see how much of those comments translate to when it comes to voting for rate hikes.

Canada Jobs: On Friday, October 9th, the monthly jobs numbers from Canada is due. Expectations are for the Canadian unemployment rate ….. So far, the Canadian jobs report has largely managed to beat estimates and has posted positive prints. A beat on estimates yet again could keep the USDCAD pressured to the downside. Besides the unemployment data, BoC Governor Poloz’s speech is due along with the building permits and Ivey PMI number.

FOMC Meeting Minutes: On Thursday, October 8th the Federal Reserve will reveal the meeting minutes from its monetary policy in September. It was a close call with the Fed opting to keep rates changed almost unanimously. The markets will be focused on the minutes to view what the Fed thinks on its prospects of a rate hike. Last month’s FOMC meeting was very hawkish with the Fed reiterating rate hikes this year including October. However with the September jobs report faring badly, the FOMC minutes could gain significance into what the future course of the Federal Reserve would be. FOMC meeting minutes aside, other data this week from the US is relatively light with the exception of the ISM non-manufacturing PMI.