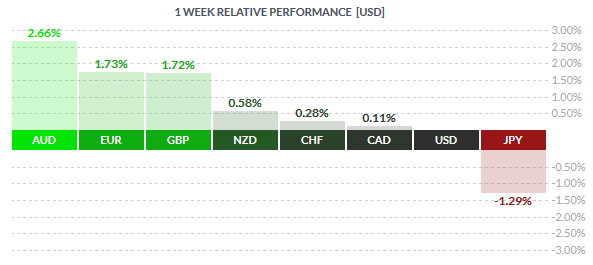

The Aussie closed the week with strong gains of over 2.6% closed followed by the Euro and the British Pound each of which closed with 1.73% and 1.72% respectively. The US Dollar was trading soft for most of last week with lack of any major market impacting data. On Friday, the US Producer price index managed to rise above estimates giving a boost to inflation expectations. However, the University of Michigan consumer sentiment declined sharply leading to the US Dollar to close on a soft note.

The Japanese Yen was the weakest performing currency last week as the modest risk-on sentiment saw investors selling the safe haven currency for the more risky assets. The US Dollar was also obviously weaker for the week. The Kiwi dollar which saw a sharp decline managed to close the week with moderate gains of 0.58%.

Fundamentals for the Week 14/09 – 18/09

| Date | Time | Currency | Detail | Forecast | Previous |

| 14-Sep | 07:30 | JPY | Revised Industrial Production m/m | -0.60% | -0.60% |

| JPY | Tertiary Industry Activity m/m | 0.20% | 0.30% | ||

| 10:15 | CHF | PPI m/m | -0.40% | -0.30% | |

| CHF | Retail Sales y/y | 1.50% | -0.90% | ||

| 12:00 | EUR | Industrial Production m/m | 0.30% | -0.40% | |

| 15-Sep | 04:30 | AUD | Monetary Policy Meeting Minutes | ||

| AUD | New Motor Vehicle Sales m/m | -1.30% | |||

| Tentative | JPY | Monetary Policy Statement | |||

| Tentative | JPY | BOJ Press Conference | |||

| 09:45 | EUR | French CPI m/m | 0.40% | -0.40% | |

| 11:30 | GBP | CPI y/y | 0.00% | 0.10% | |

| GBP | PPI Input m/m | -2.20% | -0.90% | ||

| GBP | RPI y/y | 0.90% | 1.00% | ||

| GBP | Core CPI y/y | 1.00% | 1.20% | ||

| GBP | HPI y/y | 6.20% | 5.70% | ||

| GBP | PPI Output m/m | -0.20% | -0.10% | ||

| 12:00 | EUR | German ZEW Economic Sentiment | 18.3 | 25 | |

| EUR | ZEW Economic Sentiment | 42.1 | 47.6 | ||

| EUR | Employment Change q/q | 0.10% | 0.10% | ||

| EUR | Trade Balance | 21.4B | 21.9B | ||

| 15:30 | USD | Core Retail Sales m/m | 0.10% | 0.40% | |

| USD | Retail Sales m/m | 0.40% | 0.60% | ||

| USD | Empire State Manufacturing Index | 0.7 | -14.9 | ||

| 16:15 | USD | Capacity Utilization Rate | 77.90% | 78.00% | |

| USD | Industrial Production m/m | -0.10% | 0.60% | ||

| 16:30 | GBP | CB Leading Index m/m | -0.20% | ||

| 17:00 | USD | Business Inventories m/m | -0.20% | 0.80% | |

| Tentative | NZD | GDT Price Index | 10.90% | ||

| 16-Sep | 01:45 | NZD | Current Account | -1.51B | 0.66B |

| 02:30 | AUD | RBA Assist Gov Debelle Speaks | |||

| 03:30 | AUD | MI Leading Index m/m | 0.00% | ||

| 08:00 | JPY | BOJ Monthly Report | |||

| 11:30 | GBP | Average Earnings Index 3m/y | 2.50% | 2.40% | |

| GBP | Claimant Count Change | -5.1K | -4.9K | ||

| GBP | Unemployment Rate | 5.60% | 5.60% | ||

| 12:00 | CHF | ZEW Economic Expectations | 5.9 | ||

| EUR | Final CPI y/y | 0.20% | 0.20% | ||

| EUR | Final Core CPI y/y | 1.00% | 1.00% | ||

| 15:30 | CAD | Manufacturing Sales m/m | 1.20% | ||

| CAD | Foreign Securities Purchases | 8.51B | |||

| USD | CPI m/m | -0.10% | 0.10% | ||

| USD | Core CPI m/m | 0.10% | 0.10% | ||

| 17:00 | USD | NAHB Housing Market Index | 61 | 61 | |

| 17:30 | USD | Crude Oil Inventories | 2.6M | ||

| 17-Sep | 01:45 | NZD | GDP q/q | 0.60% | 0.20% |

| 02:50 | JPY | Trade Balance | -0.35T | -0.37T | |

| 04:30 | AUD | RBA Bulletin | |||

| 08:45 | CHF | SECO Economic Forecasts | |||

| 09:35 | JPY | BOJ Gov Kuroda Speaks | |||

| 10:30 | CHF | Libor Rate | -0.75% | -0.75% | |

| CHF | SNB Monetary Policy Assessment | ||||

| 11:00 | EUR | ECB Economic Bulletin | |||

| EUR | Italian Trade Balance | 2.47B | 2.81B | ||

| 11:30 | GBP | Retail Sales m/m | 0.20% | 0.10% | |

| 15:30 | USD | Building Permits | 1.15M | 1.13M | |

| USD | Unemployment Claims | 276K | 275K | ||

| USD | Current Account | -111B | -113B | ||

| USD | Housing Starts | 1.16M | 1.21M | ||

| 17:00 | USD | Philly Fed Manufacturing Index | 6.1 | 8.3 | |

| 17:30 | USD | Natural Gas Storage | 68B | ||

| 21:00 | USD | FOMC Economic Projections | |||

| USD | FOMC Statement | ||||

| USD | Federal Funds Rate | <0.50% | <0.25% | ||

| 21:30 | USD | FOMC Press Conference | |||

| 18-Sep | 02:05 | GBP | BOE Quarterly Bulletin | ||

| 02:30 | AUD | RBA Gov Stevens Speaks | |||

| 02:50 | JPY | Monetary Policy Meeting Minutes | |||

| 11:00 | EUR | Current Account | 21.3B | 25.4B | |

| 15:30 | CAD | Core CPI m/m | 0.00% | ||

| CAD | CPI m/m | 0.10% | |||

| 17:00 | USD | CB Leading Index m/m | 0.20% | -0.20% |

Currencies/Events to Watch this Week

RBA Monetary Policy meeting minutes: The week ahead is a quiet one for the Aussie dollar as far as economic data is concerned. Tuesday, 15th September will see the release of the RBA’s monetary policy meeting minutes. It is most likely expected to remain a non-event given that the Australian Central Bank did not make changes to the monetary policy and also struck a largely neutral tone in the markets.

Canada Manufacturing and CPI: The monthly manufacturing sales and inflation numbers are due from Canada this week. With the BoC staying put on interest rates at its meeting last week, the focus will be on the monthly consumer inflation data which has remained unchanged at 0.00% on the core and 0.1% on the headline. A drop in the monthly consumer inflation is likely to bring back the speculation of a BoC rate cut at its next meeting in October.

SNB Meeting: Besides the Producer Price index data and the retail sales, the Swiss National bank will be meeting on 17th September. No changes are expected to the SNB Libor rate and the focus will more likely remain with the SNB’s currency interventions, especially in light of the Fed’s possible rate hike decision due later in the evening which could see the Swiss Franc being bid up in the process

Eurozone Inflation: The week ahead is quiet for the Euro with only the Eurozone annualized CPI data due for release. Expectations are for the CPI to remain unchanged from the previous month at 0.2% on the headline and 0.1% on the core. However, considering how the GDP data surprised last week, a possible beat on the CPI estimates cannot be ruled out.

UK Inflation and Jobs: Tuesday will see the release of the annualized CPI data from the UK. Expectations are for consumer inflation prices to have declined modestly with the headline CPI expected to stay flat at 0.0% while the Core CPI is expected to have fallen to 1.0% from 1.2% previously. Also this week will be the monthly jobs report. No change is expected to the unemployment rate which stands at 5.6% but the average hourly earnings is expected to rise softly to 2.5% from 2.4% last month.

BoJ Press Conference: The Bank of Japan is due to meet on 15th September. In the past week some officials from Japan voiced opinion that the BoJ should expand its QQE program. Given that the BoJ meets just a few days ahead of the Fed’s interest rate decision, it would be a close call. A possible easing in the QQE could indirectly signal that the Fed could skip hiking rates at this month’s meeting. Expect the Yen to stay volatile.

New Zealand Quarterly GDP: After the RBNZ cut rates by 25bps last week citing a slowdown in the economy, the quarterly GDP data is due for release. Expectations are on the hawkish side with the possibility that the New Zealand GDP expanded strongly at a pace of 0.6%, from 0.2% previously. The Global dairy trade index data is also due which has managed to post positive number in past two auctions. However, dairy prices have declined by over -15% this year and a continued positive data is needed to bring the conviction that the dairy prices might have bottomed out.

US CPI, Retail Sales, Fed decision: It will be a busy week for the US Dollar, starting with the retail sales numbers due on Tuesday followed by the Consumer inflation prices for the month. Friday’s PPI showed some hope as producer prices managed to rise above estimates. A positive print on the CPI could possibly shift the scales for the Fed’s interest rate decision. All eyes however will be tuned to the Fed on Thursday which is due to decide on whether to hike rates or not along with releasing the staff economic projections.