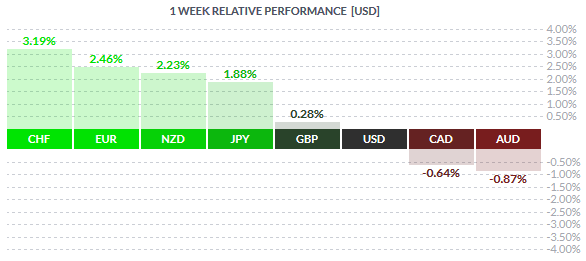

The Swiss Franc was the strongest currency last week gaining 3.19% as the general market sentiment saw investors seek safe haven assets including the Yen. The Euro was the second most top performing currency gaining 2.46% in a week that saw Greece receive its third bailout as well as the ruling SYRIZA calling for snap elections on 20th of September. The Greenback was mostly subdued last week with the currency taking a back seat as investors sold off the US Dollar after a dovish FOMC meeting minutes which brings to question whether the Fed will hike rates in September.

The Canadian dollar and the Aussie dollar made up the tail end of the currency list last week losing -0.64% and -0.87% respectively. Despite the risk off sentiment, both these currencies failed to capitalize. The Canadian dollar was tracking the losses in Crude Oil which fell to 2009 lows amidst a rise in US stockpiles and a continued production levels which outweigh demand.

Fundamentals for the Week August 24 – 28

| Date | Time | Currency | Detail | Forecast | Previous |

| 24-Aug | 22:55 | USD | FOMC Member Lockhart Speaks | ||

| 25-Aug | Tentative | AUD | CB Leading Index m/m | 0.20% | |

| Tentative | CNY | CB Leading Index m/m | 1.00% | ||

| 06:00 | NZD | Inflation Expectations q/q | 1.90% | ||

| 09:00 | EUR | German Final GDP q/q | 0.40% | 0.40% | |

| 10:15 | CHF | Employment Level | 4.24M | 4.23M | |

| 11:00 | EUR | German Ifo Business Climate | 107.6 | 108 | |

| Tentative | GBP | Index of Services 3m/3m | 0.40% | ||

| 16:00 | EUR | Belgian NBB Business Climate | -3.2 | -4.1 | |

| USD | HPI m/m | 0.40% | 0.40% | ||

| USD | S&P/CS Composite-20 HPI y/y | 5.10% | 4.90% | ||

| 16:45 | USD | Flash Services PMI | 54.1 | 55.7 | |

| 17:00 | USD | CB Consumer Confidence | 92.8 | 90.9 | |

| USD | New Home Sales | 512K | 482K | ||

| USD | Richmond Manufacturing Index | 9 | 13 | ||

| 19:25 | CAD | Gov Council Member Schembri Speaks | |||

| 26-Aug | 01:45 | NZD | Trade Balance | -600M | -60M |

| 02:50 | JPY | SPPI y/y | 0.40% | 0.40% | |

| 04:30 | AUD | Construction Work Done q/q | -1.50% | -2.40% | |

| Tentative | AUD | RBA Gov Stevens Speaks | |||

| 09:00 | CHF | UBS Consumption Indicator | 1.68 | ||

| 11:30 | GBP | BBA Mortgage Approvals | 46.0K | 44.5K | |

| 13:00 | GBP | CBI Realized Sales | 19 | 21 | |

| 15:30 | USD | Core Durable Goods Orders m/m | 0.30% | 0.60% | |

| USD | Durable Goods Orders m/m | -0.50% | 3.40% | ||

| 17:00 | USD | FOMC Member Dudley Speaks | |||

| 17:30 | USD | Crude Oil Inventories | 2.6M | ||

| 27-Aug | 04:30 | AUD | Private Capital Expenditure q/q | -2.50% | -4.40% |

| 09:00 | EUR | German Import Prices m/m | -0.30% | -0.50% | |

| GBP | Nationwide HPI m/m | 0.40% | 0.40% | ||

| 11:00 | EUR | M3 Money Supply y/y | 4.90% | 5.00% | |

| EUR | Private Loans y/y | 0.70% | 0.60% | ||

| 15:30 | CAD | Corporate Profits q/q | -6.00% | ||

| USD | Prelim GDP q/q | 3.20% | 2.30% | ||

| USD | Unemployment Claims | 275K | 277K | ||

| USD | Prelim GDP Price Index q/q | 2.00% | 2.00% | ||

| 17:00 | USD | Pending Home Sales m/m | 1.30% | -1.80% | |

| 17:30 | USD | Natural Gas Storage | 53B | ||

| Day 1 | ALL | Jackson Hole Symposium | |||

| 28-Aug | 02:05 | GBP | GfK Consumer Confidence | 4 | 4 |

| 02:30 | JPY | Household Spending y/y | 0.90% | -2.00% | |

| JPY | Tokyo Core CPI y/y | -0.10% | -0.10% | ||

| JPY | National Core CPI y/y | -0.20% | 0.10% | ||

| JPY | Unemployment Rate | 3.40% | 3.40% | ||

| 02:50 | JPY | Retail Sales y/y | 1.10% | 1.00% | |

| 08:45 | CHF | GDP q/q | -0.10% | -0.20% | |

| All Day | EUR | German Prelim CPI m/m | -0.10% | 0.20% | |

| 10:00 | EUR | Spanish Flash CPI y/y | -0.10% | 0.10% | |

| 11:30 | GBP | Second Estimate GDP q/q | 0.70% | 0.70% | |

| GBP | Prelim Business Investment q/q | 1.60% | 2.00% | ||

| 15:30 | CAD | RMPI m/m | 0.00% | ||

| CAD | IPPI m/m | 0.50% | |||

| USD | Goods Trade Balance | -62.3B | |||

| USD | Core PCE Price Index m/m | 0.10% | 0.10% | ||

| USD | Personal Spending m/m | 0.40% | 0.20% | ||

| USD | Personal Income m/m | 0.40% | 0.40% | ||

| 17:00 | USD | Revised UoM Consumer Sentiment | 93.2 | 92.9 | |

| USD | Revised UoM Inflation Expectations | 2.80% | |||

| Day 2 | ALL | Jackson Hole Symposium |

Currencies/Events to Watch this Week

German GDP: The week ahead is relatively quiet for the Euro with only a few important releases. On 25th August, German final GDP numbers are due with the median forecasts pointing to a steady 0.4% growth in the Eurozone’s largest and most important economy. Also during the week, the inflation numbers are due from Germany and Spain, both of which are expected to post a -0.1% print.

UK Second Estimate GDP: The second estimates for the second quarter GDP numbers are due from the UK on the 28th of August. Expectations are for the UK’s GDP to have been steady at 0.7%, unchanged from the first estimates. Besides the GDP print, the economic calendar from the UK is very quiet.

Japan CPI & Retail sales: Economic data from Japan this week will see the Tokyo and Core CPI numbers, both of which are expected to print -0.1% and -0.2% respectively. Retail sales numbers are also due on 28th of August with slightly hawkish expectations of 1.1%, up from 1.0% a month ago.

Kiwi inflation expectations: New Zealand inflation expectation is the only major news release this week. With the most recent quarterly PPI numbers managing to stabilize, inflation expectations could see a pick up after posting 1.9% print for the previous quarter. The Kiwi has been in a prolonged downtrend has managed to rebound for the last two weeks with further upside in store.

US GDP Second Estimates: The second estimate for the US GDP numbers are due this week and the consensus is bullish expecting to see a 3.2% rebound, up from 2.3% as posted previously. A beat on the GDP estimates will no doubt see the Greenback get a boost after weakening considerably last week. A lot of FOMC speeches are due over the week and markets will be keen to hear the views from the various members who will be speaking.