Weekly Forex Forecast for 13-17 April 2015 features the following:

The currency markets saw a roller coaster ride this week as most of the majors shifted their bias. The Euro, which was looking stronger last week turned around to be the most weakest currency this week, while the British Pound is starting to look like it is about to embark on a long volatile and bearish journey into the UK elections.

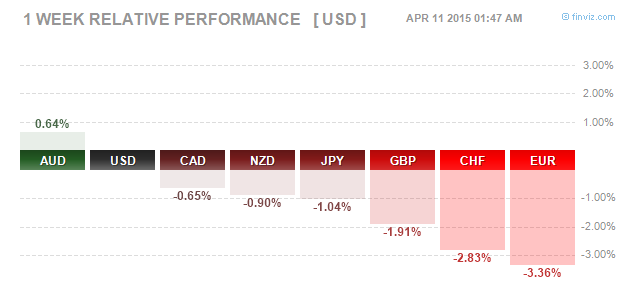

Figure 1: Weekly Spot FX Performance – 10/04/2015 (Source: Finviz.com)

The Australian Dollar was the top performer of the week as RBA left interest rates unchanged and was very resilient even against the US Dollar. Canada’s Dollar managed to ease some of its losses, especially after Friday’s jobs data managed to beat very pessimistic estimates.

Fundamentals for the Week 13 – 17 April

| Date | Time | Currency | Detail | Forecast | Previous |

| 13-Apr | 02:50 | JPY | Core Machinery Orders m/m | -2.60% | -1.70% |

| JPY | Monetary Policy Meeting Minutes | ||||

| JPY | M2 Money Stock y/y | 3.60% | 3.50% | ||

| JPY | PPI y/y | 0.40% | 0.50% | ||

| Tentative | CNY | Trade Balance | 43.4B | 60.6B | |

| 11:00 | EUR | Italian Industrial Production m/m | 0.20% | -0.70% | |

| 21:00 | USD | Federal Budget Balance | -43.1B | -192.3B | |

| 01:00 | NZD | NZIER Business Confidence | 23 | ||

| 02:01 | GBP | BRC Retail Sales Monitor y/y | 0.20% | ||

| 14-Apr | 04:30 | AUD | NAB Business Confidence | 0 | |

| 14th-15th | NZD | REINZ HPI m/m | 0.80% | ||

| 09:00 | EUR | German WPI m/m | 0.50% | ||

| 14th-15th | CNY | New Loans | 1050B | 1020B | |

| 14th-15th | CNY | M2 Money Supply y/y | 12.30% | 12.50% | |

| 11:30 | GBP | CPI y/y | 0.00% | 0.00% | |

| GBP | PPI Input m/m | -0.50% | 0.20% | ||

| GBP | RPI y/y | 1.00% | 1.00% | ||

| GBP | Core CPI y/y | 1.20% | 1.20% | ||

| GBP | HPI y/y | 8.70% | 8.40% | ||

| GBP | PPI Output m/m | 0.20% | 0.20% | ||

| 12:00 | EUR | Industrial Production m/m | 0.30% | -0.10% | |

| 15:30 | USD | Core Retail Sales m/m | 0.70% | -0.10% | |

| USD | PPI m/m | 0.30% | -0.50% | ||

| USD | Retail Sales m/m | 1.10% | -0.60% | ||

| USD | Core PPI m/m | 0.20% | -0.50% | ||

| 16:00 | USD | NFIB Small Business Index | 98.4 | 98 | |

| 17:00 | USD | Business Inventories m/m | 0.20% | 0.00% | |

| 01:45 | NZD | FPI m/m | -0.70% | ||

| 03:30 | AUD | Westpac Consumer Sentiment | -1.20% | ||

| 15-Apr | 05:00 | CNY | GDP q/y | 7.00% | 7.30% |

| CNY | Industrial Production y/y | 6.90% | 6.80% | ||

| CNY | Fixed Asset Investment ytd/y | 13.80% | 13.90% | ||

| CNY | NBS Press Conference | ||||

| CNY | Retail Sales y/y | 10.90% | 10.70% | ||

| 07:30 | JPY | Revised Industrial Production m/m | -3.10% | -3.40% | |

| 09:00 | EUR | German Final CPI m/m | 0.50% | 0.50% | |

| 09:45 | EUR | French CPI m/m | 0.70% | 0.70% | |

| Jan Data | EUR | Trade Balance | 21.9B | 23.3B | |

| 12:00 | EUR | Trade Balance | 21.2B | ||

| Tentative | EUR | German 10-y Bond Auction | 0.25|2.4 | ||

| 14:45 | EUR | Minimum Bid Rate | 0.05% | 0.05% | |

| 15:30 | CAD | Manufacturing Sales m/m | -0.20% | -1.70% | |

| EUR | ECB Press Conference | ||||

| USD | Empire State Manufacturing Index | 7.2 | 6.9 | ||

| 16:15 | USD | Capacity Utilization Rate | 78.70% | 78.90% | |

| USD | Industrial Production m/m | -0.30% | 0.10% | ||

| 16:30 | GBP | CB Leading Index m/m | 0.20% | ||

| 17:00 | CAD | BOC Monetary Policy Report | |||

| CAD | BOC Rate Statement | ||||

| CAD | Overnight Rate | 0.75% | 0.75% | ||

| USD | NAHB Housing Market Index | 55 | 53 | ||

| 17:30 | USD | Crude Oil Inventories | 10.9M | ||

| Tentative | NZD | GDT Price Index | -10.80% | ||

| 18:15 | CAD | BOC Press Conference | |||

| 21:00 | USD | Beige Book | |||

| 23:00 | USD | TIC Long-Term Purchases | 23.4B | -27.2B | |

| 01:30 | NZD | Business NZ Manufacturing Index | 55.9 | ||

| 02:01 | GBP | RICS House Price Balance | 15% | 14% | |

| 16-Apr | 02:30 | USD | FOMC Member Lacker Speaks | ||

| 04:00 | AUD | MI Inflation Expectations | 3.20% | ||

| 04:30 | AUD | Employment Change | 14.7K | 15.6K | |

| AUD | Unemployment Rate | 6.30% | 6.30% | ||

| AUD | New Motor Vehicle Sales m/m | 2.90% | |||

| 16th-19th | CNY | Foreign Direct Investment ytd/y | 16.40% | ||

| 10:15 | CHF | PPI m/m | 0.10% | -1.40% | |

| 11:00 | EUR | Italian Trade Balance | 1.21B | 0.22B | |

| Tentative | EUR | Spanish 10-y Bond Auction | 1.23|1.9 | ||

| Day 1 | ALL | G20 Meetings | |||

| 15:30 | USD | Building Permits | 1.08M | 1.10M | |

| USD | Unemployment Claims | 284K | 281K | ||

| USD | Housing Starts | 1.05M | 0.90M | ||

| 17:00 | USD | Philly Fed Manufacturing Index | 6.5 | 5 | |

| 17:30 | USD | Natural Gas Storage | 15B | ||

| 20:00 | USD | FOMC Member Lockhart Speaks | |||

| 22:00 | USD | FOMC Member Fischer Speaks | |||

| 08:00 | JPY | Consumer Confidence | 41.4 | 40.7 | |

| 10:15 | CHF | Retail Sales y/y | 0.70% | -0.30% | |

| 17-Apr | 11:00 | EUR | Current Account | 27.4B | 29.4B |

| 11:30 | GBP | Average Earnings Index 3m/y | 1.80% | 1.80% | |

| GBP | Claimant Count Change | -29.0K | -31.0K | ||

| GBP | Unemployment Rate | 5.60% | 5.70% | ||

| 12:00 | EUR | Final CPI y/y | -0.10% | -0.10% | |

| EUR | Final Core CPI y/y | 0.60% | 0.60% | ||

| Day 2 | ALL | G20 Meetings | |||

| 15:30 | CAD | Core CPI m/m | 0.30% | 0.60% | |

| CAD | Core Retail Sales m/m | 0.50% | -1.80% | ||

| CAD | CPI m/m | 0.50% | 0.90% | ||

| CAD | Foreign Securities Purchases | 5.73B | |||

| CAD | Retail Sales m/m | 0.20% | -1.70% | ||

| USD | CPI m/m | 0.20% | 0.20% | ||

| USD | Core CPI m/m | 0.20% | 0.20% | ||

| 17:00 | USD | Prelim UoM Consumer Sentiment | 93.8 | 93 | |

| USD | CB Leading Index m/m | 0.30% | 0.20% | ||

| USD | Prelim UoM Inflation Expectations | 3.00% |

Currencies/Events to Watch this Week

Will the ECB give an optimistic outlook? The European Central Bank meets this week in its first official monetary policy meeting after the launch of its QE program in January. There have been whispers about the ECB’s QE program ending ahead of schedule as economic data starts to show a bottom has been put in place. How will the ECB respond to this? Furthermore with Greece continuing to weigh on the market sentiment, there will definitely be questions asked in regards to the ECB’s role as well as any contingency plans should a Grexit happen.

BoC could put rates on hold: A better than expected jobs report is most likely to see the Bank of Canada remain muted to interest rate decisions. It is widely expected that the BoC could put policy on hold as both Crude Oil prices as well as the Canadian labor market show signs of stabilization. However, the BoC could paint a dovish outlook in the near term and choose to walk the path of caution.

China GDP and Australia jobs report: The Australian dollar might have enjoyed a stellar comeback but major headwinds arise this week as China reports its quarterly GDP data. Expectations are modest, looking to see a 7% growth, a very low reading for the likes of China. Later in the week the Australian unemployment numbers are also due, calling for the unemployment rate to remain steady at 6.3% with a moderate improvement in the employment change. A better than expected data from both ends could see the Aussie rocket higher, but any miss of estimates could equally weaken the currency and yet again raise speculation of a rate cut from the RBA.

Data heavy week for the US: This week will see a lot of Tier-1 market moving data being released from the US. Important fundamentals include retail sales and CPI. With last month’s CPI managing to beat estimates, will the momentum keep up? Estimates are moderate, expecting to see a 0.2% increase in CPI. Retail sales will also be closely watched because so far, the ‘tax break’ from falling oil prices has failed to boost retail sales. Any weakness in the data is most likely to trigger a sharp sell-off in the US Dollar.