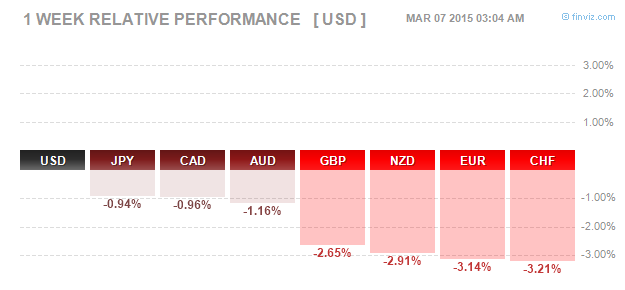

The Greenback found renewed strength as the US Dollar bulls start to resume another leg in the rally. Noticeably, the Greenback was the strongest across the board with the Swiss Franc and the Euro making up the tail end of the list.

A better than expected jobs reports with US unemployment rate ticking lower to 5.5% coupled with a better than expected job growth has brought back the optimism for a June interest rate hike, which is clearly the main driver as far as the US Dollar’s rally is concerned. However, the Greenback does seem to be heading into some major resistance levels especially the 100 psychological level. At Friday’s close, the Dollar Index ended the week at 97.67.

Fundamentals for the Week 09 – 13 March

| Date | Time | Currency | Forecast | Previous | |

| Mar-09 | 01:50 | JPY | Current Account | 1.16T | 0.98T |

| JPY | Final GDP q/q | 0.50% | 0.60% | ||

| JPY | Bank Lending y/y | 2.50% | |||

| JPY | Final GDP Price Index y/y | 2.30% | 2.30% | ||

| 02:30 | AUD | ANZ Job Advertisements m/m | 1.30% | ||

| 07:00 | JPY | Economy Watchers Sentiment | 46.7 | 45.6 | |

| 09:00 | EUR | German Trade Balance | 20.4B | 21.8B | |

| 11:30 | EUR | Sentix Investor Confidence | 15.3 | 12.4 | |

| All Day | EUR | Eurogroup Meetings | |||

| 14:15 | CAD | Housing Starts | 176K | 187K | |

| 16:00 | USD | Labor Market Conditions Index m/m | 4.9 | ||

| Mar-10 | 01:50 | JPY | M2 Money Stock y/y | 3.50% | 3.40% |

| 02:01 | GBP | BRC Retail Sales Monitor y/y | 0.20% | ||

| 02:30 | AUD | NAB Business Confidence | 3 | ||

| 03:30 | CNY | CPI y/y | 1.00% | 0.80% | |

| CNY | PPI y/y | -4.20% | -4.30% | ||

| 10th-13th | NZD | REINZ HPI m/m | -1.00% | ||

| 08:00 | JPY | Prelim Machine Tool Orders y/y | 20.40% | ||

| 08:45 | CHF | Unemployment Rate | 3.20% | 3.10% | |

| 09:45 | EUR | French Industrial Production m/m | -0.20% | 1.50% | |

| 11:00 | EUR | Italian Industrial Production m/m | 0.20% | 0.40% | |

| All Day | EUR | ECOFIN Meetings | |||

| 15:00 | USD | NFIB Small Business Index | 99.2 | 97.9 | |

| 16:00 | USD | JOLTS Job Openings | 5.04M | 5.03M | |

| USD | Wholesale Inventories m/m | 0.00% | 0.10% | ||

| Mar-11 | 00:05 | AUD | RBA Assist Gov Kent Speaks | ||

| 01:30 | AUD | Westpac Consumer Sentiment | 8.00% | ||

| 01:50 | JPY | Core Machinery Orders m/m | -3.90% | 8.30% | |

| JPY | PPI y/y | 0.50% | 0.30% | ||

| 02:30 | AUD | Home Loans m/m | -1.90% | 2.70% | |

| 07:30 | CNY | Industrial Production y/y | 7.70% | 7.90% | |

| CNY | Fixed Asset Investment ytd/y | 15.10% | 15.70% | ||

| CNY | Retail Sales y/y | 11.60% | 11.90% | ||

| 08:30 | EUR | French Final Non-Farm Payrolls q/q | 0.00% | 0.00% | |

| 11th-15th | CNY | New Loans | 755B | 1470B | |

| 11th-15th | CNY | M2 Money Supply y/y | 11.10% | 10.80% | |

| 11:30 | GBP | Manufacturing Production m/m | 0.20% | 0.10% | |

| GBP | Industrial Production m/m | 0.20% | -0.20% | ||

| 16:30 | USD | Crude Oil Inventories | 10.3M | ||

| 17:00 | GBP | NIESR GDP Estimate | 0.70% | ||

| 19:01 | USD | 10-y Bond Auction | 2.00|2.6 | ||

| 20:00 | USD | Federal Budget Balance | -187.3B | -17.5B | |

| 22:00 | NZD | Official Cash Rate | 3.50% | 3.50% | |

| NZD | RBNZ Rate Statement | ||||

| NZD | RBNZ Monetary Policy Statement | ||||

| 22:05 | NZD | RBNZ Press Conference | |||

| 23:30 | USD | Bank Stress Test Results | |||

| 23:45 | NZD | FPI m/m | 1.30% | ||

| Mar-12 | 01:50 | JPY | BSI Manufacturing Index | 5.7 | 8.1 |

| JPY | Tertiary Industry Activity m/m | 0.60% | -0.30% | ||

| 02:00 | AUD | MI Inflation Expectations | 4.00% | ||

| 02:01 | GBP | BOE Quarterly Bulletin | |||

| GBP | RICS House Price Balance | 6% | 7% | ||

| 02:30 | AUD | Employment Change | 15.3K | -12.2K | |

| AUD | Unemployment Rate | 6.40% | 6.40% | ||

| 07:00 | JPY | Consumer Confidence | 39.9 | 39.1 | |

| 09:00 | EUR | German Final CPI m/m | 0.90% | 0.90% | |

| 09:45 | EUR | French CPI m/m | 0.60% | -1.00% | |

| 11:30 | GBP | Trade Balance | -9.7B | -10.2B | |

| 12:00 | EUR | Industrial Production m/m | 0.30% | 0.00% | |

| Tentative | EUR | Spanish 10-y Bond Auction | 1.62|2.0 | ||

| 14:30 | CAD | NHPI m/m | 0.20% | 0.10% | |

| CAD | Capacity Utilization Rate | 83.70% | 83.40% | ||

| USD | Core Retail Sales m/m | 0.60% | -0.90% | ||

| USD | Retail Sales m/m | 0.50% | -0.80% | ||

| USD | Unemployment Claims | 317K | 320K | ||

| USD | Import Prices m/m | 0.20% | -2.80% | ||

| 16:00 | USD | Business Inventories m/m | 0.20% | 0.10% | |

| 16:30 | USD | Natural Gas Storage | |||

| 19:01 | USD | 30-y Bond Auction | 2.56|2.3 | ||

| 23:30 | NZD | Business NZ Manufacturing Index | 50.9 | ||

| Mar-13 | 06:30 | JPY | Revised Industrial Production m/m | 4.00% | 4.00% |

| 09:00 | EUR | German WPI m/m | -0.20% | -0.40% | |

| 11:30 | GBP | Construction Output m/m | 1.40% | 0.40% | |

| 14:30 | CAD | Employment Change | 21.3K | 35.4K | |

| CAD | Unemployment Rate | 6.50% | 6.60% | ||

| USD | PPI m/m | 0.20% | -0.80% | ||

| USD | Core PPI m/m | 0.10% | -0.10% | ||

| 16:00 | USD | Prelim UoM Consumer Sentiment | 95.6 | 95.4 | |

| USD | Prelim UoM Inflation Expectations | 2.80% |

Currencies/Events to Watch this Week

Japan GDP data: The Japanese Yen was relatively quiet for most part of the past few weeks. The week ahead will see the quarterly GDP data from Japan. After barely toeing the line into a technical recession few quarters ago, the GDP data will be important for the Yen. Expectations are for a 0.5% soft decline from 0.6% previously while on an annualized basis GDP is expected remain steady at 2.3%.

Australia Jobs report: With GDP showing a modest increase from 0.4% to 0.5%, the Australian employment data will be closely watched. While the RBA expects short term unemployment rate to rise, the markets will be focused on how much of a deviation to expect. Expectations are for a 6.4% unemployment rate to remain steady. Also on focus will be the home loans, which is likely to provide insight into the activity in the housing sector which has continued to grow on account of an easing conditions in the monetary policy.

Canada Jobs report: With the BoC standing pat on policy, the markets turn their attention to this Friday’s jobs report from the country. Expectations are for an improved unemployment rate to 6.5% from 6.6%. With no other news releases for this week, the jobs data is likely to be a market mover for the Canadian cross currency rates.

RBNZ Monetary policy: With the RBA, BoC holding rates steady, markets tune up to the RBNZ. The central bank is expected to keep its rates on hold and markets would focus on the tone of the statement and forward guidance. Will the RBNZ continue to hike rates later this year or will the Central bank hold the rate hikes? The Kiwi has been trading in a tight range for the most part and the RBNZ event is likely to set the further direction this week.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)