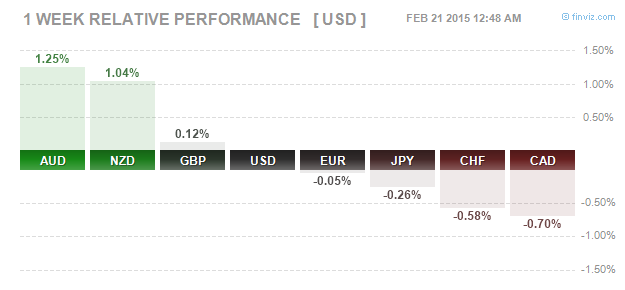

The Kiwi Dollar continued to push on for its second straight week of gains against a weaker Greenback. The Australian dollar also managed to come out on the top, gaining 1.25% for the week despite some fundamental risks to the currency. The Aussie dollar got a boost after S&P reiterated Australia’s business investment rating at AAA despite warning that the Australian budget would be under pressure. Despite the headwinds along with weaker unemployment data, the Australian dollar has been quite resilient across the board.

The Canadian dollar was the weakest performing currency last week as data continued to come out weaker than expected, with the latest retail sales data for the month of January posting a 4-year low. The US Dollar managed to close modestly in the green on Friday posting a two day gain against a broader weakness as we head into the important Janet Yellen testimony this week.

Fundamentals for the Week 23- 27 Feb

| Date | Event | Estimates |

| 23 February | Japan monetary policy meeting minutes | – |

| German Ifo business climate | 107.4 | |

| UK CBI realized sales | 42 | |

| US existing home sales | 5.03mn | |

| 24 February | New Zealand inflation expectations | – |

| Germany final GDP q/q | 0.7% | |

| Eurozone final CPI y/y | -0.6% | |

| Eurozone final core CPI y/y | 0.6% | |

| ECB President Draghi speech | – | |

| S&P/CS composite HPI | 4.5% | |

| US Flash services PMI | 54.5 | |

| US CB consumer confidence | 99.6 | |

| Fed Chair Yellen Testimony | – | |

| Richmond manufacturing index | 7 | |

| BoC Governor Poloz speech | – | |

| 25th February | Australia construction work done q/q | -0.8% |

| Australia wage price index q/q | 0.7% | |

| China HSBC manufacturing PMI | 49.6 | |

| UK BBA mortgage approvals | 36.2k | |

| Fed Chair Yellen testimony | – | |

| US New home sales | 477k | |

| ECB President Draghi speech | – | |

| New Zealand trade balance | -157mn | |

| 26th February | Australia private expenditure q/q | -1.3% |

| Gfk German consumer climate | 9.6 | |

| German unemployment change | -10k | |

| Italy retail sales m/m | 0.3% | |

| UK GDP second estimate q/q | 0.5% | |

| UK prelim business investment q/q | 2.3% | |

| UK index of services 3m/3m | 0.7% | |

| ECB TLTRO | – | |

| Canada core CPI m/m | 0.1% | |

| Canada CPI m/m | -0.3% | |

| US CPI m/m | -0.6% | |

| US Core CPI m/m | 0.1% | |

| US unemployment claims | 285k | |

| US Core durable goods orders m/m | 0.6% | |

| US durable goods orders m/m | 1.7% | |

| US HPI m/m | 0.5% | |

| 27th February | Japan household spending y/y | -4% |

| Tokyo Core CPI y/y | 2.2% | |

| Japan National core CPI y/y | 2.4% | |

| Japan unemployment rate | 3.4% | |

| Japan prelim industrial production m/m | 3.1% | |

| Japan retail sales m/m | -1.1% | |

| UK Gfk consumer confidence | 3 | |

| Australia private sector credit m/m | 0.5% | |

| German import prices m/m | -0.8% | |

| Germany prelim CPI m/m | 0.6% | |

| Spain flash CPI y/y | -1.5% | |

| Italy prelim CPI m/m | 0.2% | |

| US prelim GDP q/q | 2.1% | |

| US prelim GDP price index q/q | 0% | |

| US Chicago PMI | 58.4 | |

| US Pending home sales | 2.5% | |

| Revised UoM consumer confidence | 94.2 | |

| Revised UoM inflation expectations | 2.5% |

Currencies/Events to Watch this Week

Janet Yellen and US GDP: Will the US dollar manage to bounce back on a hawkish tone from Janet Yellen in this week’s testimony? Or will Ms. Yellen continue to remain cautious and expect markets to remain “patient”? That will be the main focus for the Greenback in the first part of this week. US GDP numbers are also expected later on Friday with consensus calling for a 2.1% growth. Considering weaker data for the most part, any beat on the estimates could send the Greenback higher. Expect a lot of volatility in the US Dollar this week.

Focus on Draghi: With the Greece debt negotiations having resulted in a 4-month extension, the Euro can breathe easy now but comes under pressure as ECB President Mario Draghi is expected to speak at various occasions. Although not directly related to monetary policy, Draghi’s speech on 25th February will be to testify on the ECB’s annual report. Also on tap are GDP numbers from Germany.

UK Revised GDP: The only major market moving event this week for the Pound is the Thursday’s revised GDP numbers for the final quarter of 2014. Consensus is expecting the GDP to remain unchanged at 0.5%.

FX Majors Weekly Pivots

| R3 | R2 | R1 | Pivot | S1 | S2 | S3 | |

| EURUSD | 1.163 | 1.1539 | 1.1458 | 1.1368 | 1.1287 | 1.1197 | 1.1115 |

| GBPUSD | 1.564 | 1.556 | 1.5477 | 1.5396 | 1.5313 | 1.5233 | 1.515 |

| USDCAD | 1.2812 | 1.2688 | 1.261 | 1.2486 | 1.2408 | 1.2284 | 1.2206 |

| USDJPY | 120.755 | 120.086 | 119.574 | 118.905 | 118.393 | 117.724 | 117.212 |

| AUDUSD | 0.7986 | 0.7917 | 0.7880 | 0.7811 | 0.7774 | 0.7705 | 0.7667 |

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)