Following a rather busy week in Europe, the focus shifts back to the U.S. shores next week with the FOMC meeting in focus. The Fed’s meeting is likely to overshadow other central bank meetings such as the BoJ, SNB, and the BoE. Economic data from the UK will keep the British pound busy ahead of Thursday’s Bank of England’s monetary policy meeting.

The Euro and the other major currencies take a backseat. New Zealand’s first-quarter GDP is on the tap, while in the Eurozone, the final inflation figures for May will be due on Friday.

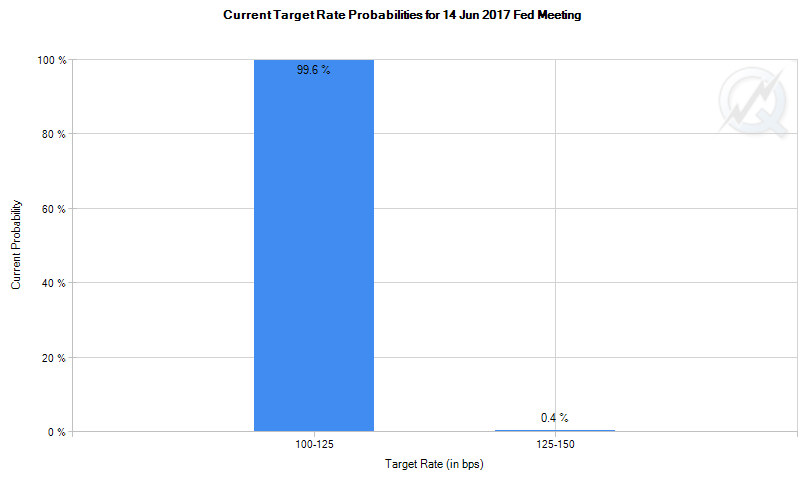

FOMC Meeting – Fed to hike rates, but what about outlook?

The Federal Reserve is all set to hike interest rates at this week’s monetary policy meeting with a 25-basis point increase. This will bring the short term fed funds rate to 1.0% – 1.25% window.

Despite the rate hike which is widely expected, the Fed will also be holding a press conference along with releasing fresh economic forecasts and rate hike expectations for the remainder of this year.

With the rate hike a near certainty, the markets will be looking to what the Fed Chair, Ms. Yellen has to say about the economy. The recent jobs report continued to paint a mixed picture. The only bright spot was the fact that the unemployment rate fell to 4.3%. However, wage growth has remained steady at 2.5%. Inflation has also remained firm but below the Fed’s 2% target rate.

The Fed has so far maintained that there will be another rate hike this year. It is quite likely that the Fed will maintain the tone, given that officials will need to weigh and assess the U.S. economy with further data.

At the previous FOMC meeting, the Fed maintained that the recent string of weak jobs data suggested that it was only temporarily. But with the weak print in May, the possibility of the change in wording could send out a dovish signal.

The next rate hike is currently expected around September, although this could possibly be pushed down to December as well. At the FOMC meeting minutes, the Fed showed that officials were discussing the balance sheet.

Considered a form of tightening, the Fed could also shed some light on its plans to reduce its balance sheet and possibly prepare the markets for a timeline for implementing this.

Busy week for the GBP– Inflation, Jobs, and BoE

It will be a busy week for the UK with a number of high impact events lined up. Data over the week will include the monthly inflation figures as well as the labor market data. This will culminate with Thursday’s Bank of England monetary policy meeting.

Inflation in the UK rose 2.7% a month ago. This came after a somewhat headline print in the previous month. A continued increase in the inflation even this month could potentially keep the BoE officials in a hot spot. While the central bank has maintained that they will tolerate an inflation overshoot above 2%, the question remains for how long.

UK Elections: Cable Crashes As Conservatives Lose Ground

Besides the inflation data, wages are also going to play a major role; more importantly, wage growth in the UK which has stalled.

As far as monetary policy is concerned, no changes are expected from the BoE given that the UK will be starting its Brexit negotiations with the EU from June 19th. This could potentially see the BoE stand on the sidelines until there is some clarity and progress on the UK-EU talks.

BoJ expected to stay on the sidelines

The Bank of Japan’s monetary policy meeting is due this week on Thursday. The Bank of Japan is expected to stay on the sidelines with no major changes expected. At the previous meeting, officials at the BoJ said that it could take longer than previously expected about inflation reaching the central bank’s 2% target.

However, growth is also expected to be muted. Recent data released last week showed that the revised first quarter GDP was at 0.3%, slower than the previous reading of 0.5%. It was also lower than the expectations of 0.6%.

The year over year GDP growth was revised down to 1% after the initial reading of 2.2%.

With the downbeat GDP numbers, the BoJ is likely to caution the downsides to the GDP growth. However as far as further easing expectations from the BoJ is concerned, it is highly unlikely that we will get see one anytime soon.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)