Market Summary

- RBNZ keeps OCR unchanged at 2.0%, signals further easing likely

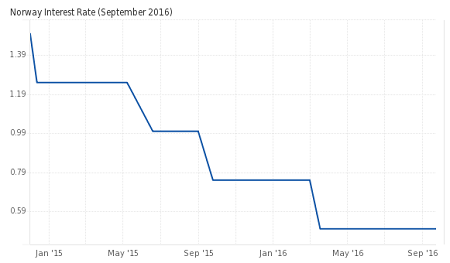

- Norges Bank keeps interest rate unchanged at 0.50%, signals rate stability

- NOK rallies on Norges Bank decision

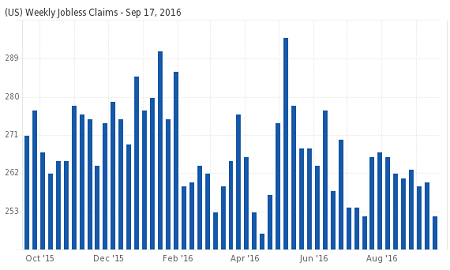

- US weekly unemployment claims now below 300k for 81 straight weeks

Today’s Economic events

- RBNZ keeps OCR unchanged at 2.0%

- RBA Gov. Lowe speech

- ECB LTRO 45.3bn vs. 399.3bn previously

- UK CBI industrial order expectations -5 vs. -5

- Norges Bank interest rate 0.50% vs. 0.50%

- US weekly unemployment claims 252k vs. 261k

Coming Up

- (EUR) ECB President Mario Draghi speech

- (USD) HPI m/m

- (GBP) BoE MPC Member Cunliffe speech

- (EUR) Eurozone consumer confidence

- (USD) Existing home sales

- (USD) CB leading index

- (GBP) BoE Gov. Carney speech

Fed stands pat. Signals December rate hike

As expected, the US Federal Reserve at the conclusion of its two-day FOMC meeting kept the short-term interest rates unchanged in the band of 0.25% – 0.50%. The decision was made with a vote of 7 – 3. The three dissenters, voting for a rate hike were Kansas City Fed chief, Esther George, Cleveland Fed chief, Loretta Mester and Boston Fed chief, Eric Rosengren.

The Fed, however, sent strong signals, noting that “the case for an increase in the federal funds rate has strengthened.” But the case wasn’t as compelling for the dovish policymakers. The statement said, “[The Fed] decided, for the time being, to wait for further evidence of continued progress toward its objectives.”

The Fed’s statement also saw officials bringing back the balance of risks in the language which was missing previously. The September statement said “Near-term risks to the economic outlook appear roughly balanced” which indicates that officials will consider a rate hike in the near future. The Fed also made further references noting that it “continues to closely monitor inflation indicators and global economic and financial developments.”

The Fed’s decision to hold rates steady at yesterday’s meeting was widely expected with the markets seeing a rather soft response as a result. Gold prices gained over 1.50% on the day while the yen gained 1.38%. The US dollar was, of course, the weakest, losing 0.90% on the day.

At the close of the day, the CME Futures Fed funds tool showed a modest increase to 59% in probability of a Fed rate hike in December, up from 57% from a day before.

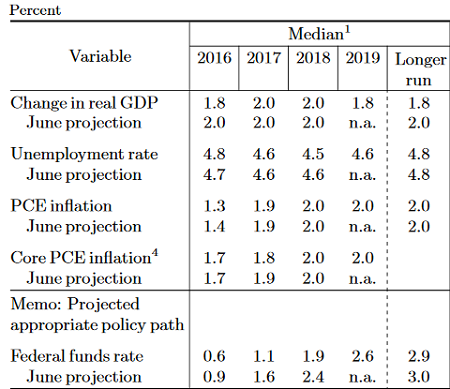

The Fed also released its expectations on future interest rates which showed that officials expect rates to hit 1.10% by the end of 2017, which is slightly lower than June’s expectations of 1.60%. On updated forecasts for growth and inflation, the data was largely unchanged from June’s projections. The median forecasts showed that the US economy is poised to grow at a rate of 1.80% in this year, down from the projected 2.0% in June while the unemployment rate is expected to fall to 4.80% by the end of this year. On inflation, the Fed projections show inflation to register at 1.30% while core inflation is expected to rise to 1.70% by the end of the year, both of which are below the Fed’s 2.0% target.

RBNZ holds rates but signals future rate cuts

A few hours after the FOMC meeting, the Reserve Bank of New Zealand’s monetary policy meeting showed the central bank keeping the OCR unchanged at 2.0% as widely expected. Despite holding rates steady, the RBNZ said that further easing remains likely, pointing to factors such as the entrenched low inflation and the bloated exchange rate of the New Zealand dollar. The RBNZ previously cut the OCR by 25bps at its previous meeting in August.

“Our current projections and assumptions indicate that further policy easing will be required to ensure that future inflation settles near the middle of the target range,” RBNZ Governor, Wheeler said noting that “We will continue to watch closely the emerging economic data.” On the recent GDP numbers, the central banks said that it was in line with earlier forecasts.

The dovish signals come despite a broad improvement in the New Zealand economy. Imre Speizer, the currency strategist at Westpac, said that “Markets have so far interpreted the outcome as a mild dovish surprise. That is because the stream of good NZ economic news over the past month had caused a hawkish reassessment of market pricing.”

The RBNZ’s next policy meeting is scheduled for November where another 25bps rate cut is likely to be introduced. Su-Lin Ong, senior economist at RBC Capital Markets, says, “the RBNZ has left rates on hold at a policy meeting, which likely reflects some solid economic data of late, but there can be little doubt the bank is pondering deeply cutting interest rates again in November. While inflation remains stubbornly low and the currency too high, the balance of risks will remain toward lower interest rates.”

Following the RBNZ’s decision, the Kiwi kept its gains, closing the day 0.56% higher, closing at an 8-day high at 0.7355.

Norges Bank keeps rates on hold

Norway’s central bank (Norges Bank) at its monetary policy meeting today held its key interest rate unchanged at 0.50%, as widely anticipated. Norges Bank, in its statement, said that interest rate was likely to remain steady in the near term brushing aside concerns of another rate cut to stimulate the economy or to hike rates to curb housing prices.

The Norges Bank decision comes after it delivered a 25bps rate cut in March 2016.

“Our current assessment of the outlook suggests that the key policy rate will most likely remain at today’s level in the period ahead,” Governor Olsen from Norges Bank said in the statement.

Following the rate decision, the NOK surged strongly against the euro on potential hints that the central bank was moving away from an easing bias. NOK was seen rising as much as 1 percent against its peers. Norges Bank raised the outlook for its rate based on key economic indicators which hint at the optimism that the worst might just be over after the economy managed to come out largely unscathed following the plunge in oil prices over the past years.

Among the key economic indicators that led to the decision towards interest rate stability was that inflation turned higher in recent months, which the bank noted and not least within the real estate market. “House price inflation has accelerated and been higher than projected,” the statement said noting that the central bank’s low-interest rate policy was partly contributing to “persistently high rate of increase in house prices.”

Analysts at DNB say that the Norges Bank could keep interest rate unchanged for the remainder of 2016 while maintaining that economic data will continue to improve. “The central bank’s own forecasts signal a 20% likelihood of a rate cut in December,” DNB says, lowering the risks of further changes to interest rates.

US unemployment claims rise less than expected

The number of Americans filing for unemployment benefits last week fell to the weakest level since July this year, highlighting the strength in the labor markets. Initial jobless claims fell by 8000 to a seasonally adjusted 252k for the week ending September 17, data from the labor department showed on Thursday. This was less than the market expectations of 261k.

Initial jobless claims data for the previous week of September 10 was unchanged at 260k while the 4-week moving average for the claims fell to 258k. The weekly jobless claims are now into the 81st week of coming out below 300k, marking the longest streak since 1970.

The US dollar was muted to the news.

In a separate report, regional economic indicator from the Chicago Fed showed a decline in August. The National Activity Index released by the Chicago Federal Reserve fell to -0.55 in August, following a revised print of 0.24 in July. The gauge was lower from a year ago, recorded at -0.33. The National activity index is a weighted basket of over 85 indicators covering the broad categories of the economy including production and income, employment, personal consumption among others. The index provides a snapshot of the national economic activity as well as inflation pressures. The reading of below zero in August suggests that the US economy was growing below its long-run trend level or below average growth.