The U.S. dollar was seen making a comeback in the month of February as the once deemed to be weak currency was seen making signs of a temporary bottom. The sentiment in the U.S. dollar was lifted by a mix of broad fiscal and monetary policy signals.

Although no major changes were seen in the month of February, the potential talks of President Trump’s infrastructure spending alongside a hawkish Fed speak led to the USD’s reversal.

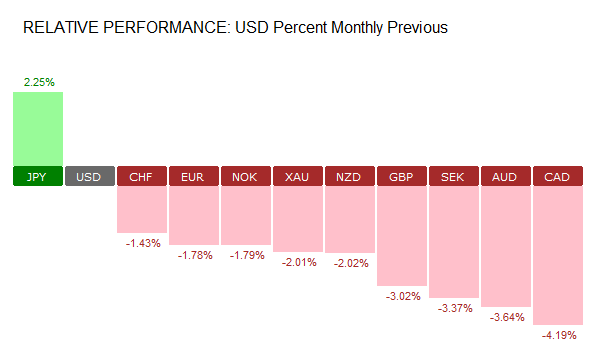

The Japanese yen, of course emerged as the top performing currency in the month of February. The yen managed to rise 2.25% on the month. The weakest currency was of course the Canadian dollar which fell over 4.19%. The weakness in the Canadian dollar came about as economic data remained mixed, with the exception of inflation which showed signs of resurgence.

Following the rather mixed spell, expectations of aggressive rate hikes from the Bank of Canada also fell. Investors were also aware about the ongoing uncertainty surrounding the U.S. administration’s approach to the NAFTA deal.

Data from the Eurozone was limited which saw the common currency mostly consolidating and eventually led to a decline as the U.S. dollar strengthened. The market speculation of hawkish ECB forward guidance were also quashed as the minutes of the meeting from January showed that officials were hesitant to change the language in the ECB’s statement.

There were also some minor headwinds for the common currency as Germany was still undecided on forming a majority government. While coalition talks finally led to the famed alliance between Merkel’s CDU/CSU and the SPD party, the market reaction was muted. The Italian elections that were held in early days of March also weighed in on the markets keeping the sentiment in check in the euro currency.

The March 2018 Monthly Outlook

The month ahead will see some major central bank meetings lined up, mostly during the first part of the month. Broadly, no changes are expected from most of the central banks. However, the FOMC meeting, due later in March will no doubt stand out as investors start to price in another rate hike from the Fed.

Here’s a quick preview of the March 2018 Monthly Outlook and the main events to look forward to.

ECB expected to remain on the sidelines

The European Central Bank will be holding its meeting this week on Thursday. There are no expectations for any potential changes to either interest rates or the central bank’s QE purchases which are expected to continue through September this year.

However, given the fact that officials backtracked on the potential changes to the ECB’s forward guidance, the markets are likely to wait for more cues at this week’s meeting. Although inflation was showing encouraging signs just a few months ago, the recent subdued pace of growth in consumer prices still weighs on the markets, despite hawkish expectations.

The March ECB meeting will also see officials releasing the official forecasts. These are unlikely to spring any surprises. It is common knowledge that the Eurozone economic activity continued to rise at a steady pace in the first quarter. Inflation and unemployment remain two key factors that could offset the hawkish narrative as far as GDP growth is concerned.

There is also speculation that the recent high levels of the euro’s exchange rate might have dampened inflationary pressures. This could potentially result in the ECB staying neutral to dovish at the March meeting.

Fed’s Powell likely to start first official meeting with a rate hike

The new Federal Reserve Chairman, Jerome Powell is most likely to start off his first official FOMC meeting with a rate hike. Given the upbeat trend in the underlying economic data, officials are expected to vote for a rate hike at the March meeting.

The Fed’s meeting is due only later in March. However, it is unlikely that the FOMC could change its mind on interest rates. This week’s nonfarm payrolls could potentially play a key role in shaping the interest rate expectations.

Wage growth remains a concern but officials remain optimistic that inflation will start to rise on the back of tightening labor market conditions. Speculation in the markets has also increase on the number of rate hikes this year. While the Fed had previously signaled three rate hikes in March, this could potentially change to four if the momentum keeps up.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)