FX Markets Monthly Outlook December 2017

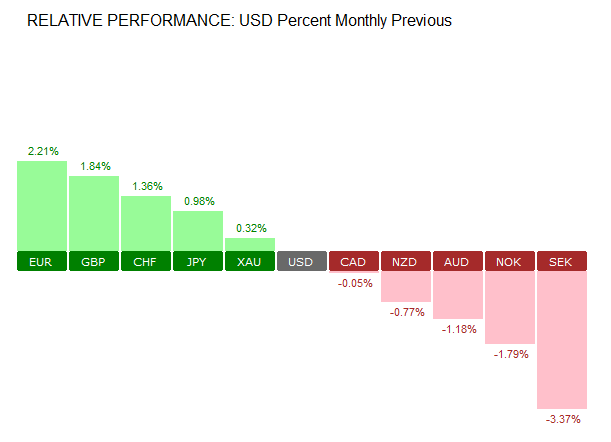

The month of November was fairly quiet for the markets with no major shocks or surprises. The main talking points of the month were the fact that president Trump managed to finally push the tax reforms proposals during the month however, it is still under discussion.

He also selected Fed Governor, Jerome Powell as the next chairman of the Federal Reserve starting March 2018. The Fed Chair, Janet Yellen’s term is due to expire in February.

The Fed was seen staying committed to hiking interest rates in December. However, the slow pace of inflation has yet to convince the markets about this rate hike.

On the other hand, the U.S. GDP data continued to rise strongly, posting a 3.3% third quarter expansion.

In the Eurozone, the economic recovery continued with Germany spearheading growth. However, despite the upbeat numbers, inflation remains weak in the region. The German political landscape also came under pressure during the month as the coalition talks with Angela Merkel’s party and other allies fell apart. This raised the prospect of snap elections in Germany.

The euro initially reacted to the news however, the reaction was short lived, as the common currency started to rise strongly against the U.S. dollar.

The month ahead: December 2017

The month of December promises to be calm. The main highlight of the month will, of course, be the Federal Reserve meeting. Interest rates can be expected to be hiked by 25 basis points. Elsewhere, no major decision making meetings are due. The Brexit saga is expected to continue in the background.

There might be a possibility that the Bank of Canada could hike rates one more time. However, this is highly doubtful and remains to be seen on further incoming data. The recent string of weakness in the Canadian economy could keep the BoC on the sidelines. However, higher oil prices could be seen keeping the Canadian dollar supported in the short term.

Here’s a quick preview of the main events to look forward to in December.

FOMC Meeting: Final rate hike for 2017 (Dec 13th)

The FOMC meeting is scheduled for December 13, 2017. The Fed is widely expected to raise interest rates at this meeting by 25 basis points. This would bring the short term Fed funds rate to 1.25% – 1.50%. The December meeting will also probably be the last rate hike meeting chaired by Janet Yellen when her term expires in February 2018.

The Fed will also release the economic forecasts at this meeting and it will be followed by the press conference hosted by Janet Yellen. Investors will be keen to see the future course of rate hikes in 2018. Currently, three rate hikes are penciled in for the year ahead.

The potential candidate for becoming the new chair of the Fed, Jerome Powell, is widely seen as keeping up with continuity in the current Fed’s policies. As a result, market shocks are expected to be mitigated.

The meeting will most likely address the weak inflation phase which has baffled policy makers. Wage growth in the U.S. has also remained broadly stable this year. Further evidence is required of wage pressures building up which, could give policy makers the confidence to push ahead with the proposed three rate hikes.

The Fed’s dot plot will also come into focus. Next year, the FOMC voting members will be rotated with most of the new voting members seen to be in favor of the hawkish side.

Other central bank meetings to see no changes

Besides the Fed’s meeting, December will also see other monetary policy meetings. This includes meetings of the Bank of Canada, the Swiss National Bank and the European Central Bank to name a few. All the central banks are expected to keep the status quo.

Focus will briefly turn to the ECB’s meeting on December 14th. The ECB had announced that QE will run until September 2018 at a reduced pace of 30 billion euro per month starting January. No major decisions are expected with the ECB likely to remain on the sidelines.

The Bank of Canada’s monetary policy meeting is scheduled for December 6th. Although the latter part of the year started off on a hawkish note, the appreciation in the exchange rate of the Canadian dollar impacted the export business.

Further uncertainty exists regarding the NAFTA deal which is expected to see the Bank of Canada also stay on the sidelines. This is likely to impact the Canadian dollar strongly which has one of the top performing currency pairs this year.

The BoE, RBA and the SNB meetings will likely pass off as a non-event for the most part with the respective governors likely to stay on the sidelines.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)