September was marked by some big events that include the FOMC, ECB meetings in the backdrop of the German elections. The month was largely a non-event with most of the outcomes coming in line with market expectations.

The ECB managed to match the expectations although it did not make any major changes. The market reaction was also very well managed by Draghi as the decision to taper is expected to be announced in October. The FOMC meeting saw the Fed announcing its plans to start the balance sheet unwinding from October. The Fed still signaled that interest rates could rise later this year, which saw the markets quickly re-pricing the rate hike, although a lot will hinge on the inflation expectations.

Finally, the German elections were held on September 23. The outcome was again as expected as the CDU/CSU led by Angela Merkel saw another victory. Despite the positive headline, the details showed that the German fringe parties made some inroads at the cost of the CDU/CSU which lost some of its votes. The main opponent, Martin Schulz’s came in second with 20.5%. The coalition is expected to be somewhat tough, but something which Ms. Merkel is not new to.

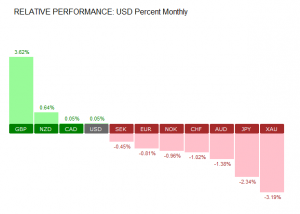

During September, the biggest winner was the British pound that gained 3.62%. On the tail end, gold prices fell 3.19% followed by the Japanese yen.

The month ahead: October 2017

With the Fed and the ECB, both looking to the October monetary policy meeting, the month ahead will see some major changes to monetary policies. It is quite likely that the ECB’s meeting will overshadow that of the Fed’s operations, which in any case seems to be on the back foot.

Here is a quick summary to the major events to look forward to in October 2017.

ECB Monetary policy – Markets fully pricing in the taper announcement (Oct 26th)

All eyes turn to the European central bank this month as the monthly monetary policy meeting is held later in the month on October 26. After months of speculation from the markets and a cautious stance from the ECB’s governing council, the stage is set for the ECB to announce its tapering decision.

The event is widely priced in, since Draghi’s hawkish speech in late June this year. The markets were hoping for a tapering announcement in September, but the ECB put off the decision to this month. Despite the hawkish expectations, the ECB has maintained that it is committed to keeping interest rates at the current levels until the QE program winds down.

According to some estimates, interest rate futures in the Eurozone show just under 50% probability for a rate hike next year. Furthermore, Draghi will also need to manage the euro’s exchange rate which has been one of the top performing currencies this year. Although Draghi briefly made a reference to the exchange rate at last month’s meeting, the markets were seen shrugging off those comments.

With the tapering already well priced in, markets will be looking to what comes next. For one, the ECB’s tapering amount will be the big question, and also Draghi’s forward guidance will be important in shaping the expectations on the euro currency.

FOMC– Balance sheet reduction to start

The month of October will not be seeing any FOMC meeting, although the Fed has a scheduled meeting on November 1st. The meeting will not have any press conference that follows which could thus make the Fed’s meeting a non-event.

Having signaled that the balance sheet unwinding will start in October, the Federal Reserve could be overshadowed by the ECB’s meeting. However, the markets will be looking to the FOMC statement for further clues on how the Fed proposes to increase interest rates. Currently, the expectations are building up that the central bank will hike rates one more time in December by 25 basis points.