The markets head into a slow week. From the US Fed speakers include Janet Yellen who will be speaking next week. A rather busy week from the US will see the GDP revisions for the second quarter alongside the core PCE price index data.

In the eurozone, preliminary inflation numbers from Germany, Spain, and France will culminate with the flash inflation estimates for the eurozone in September. An expected increase in inflation could potentially spark further bets on QE tapering from the ECB when it meets in October.

GDP numbers from the UK and Canada are also expected to be released this week. The UK’s GDP is expected to remain steady at 0.3% on the final revision. However, the ongoing Brexit talks remain in the backdrop as far as volatility is concerned.

Here is a brief recap of the main events that will shape the currency markets this week.

US final GDP and PCE Price index

The week ahead is lined up with various Fed speakers taking the stage. Among the speakers, the Fed Chair, Janet Yellen will also be speaking. Ms. Yellen is expected to address the NABE conference on Tuesday. With the markets currently re-pricing another Fed rate hike by December, investors will be closely tuning into what the Fed speakers will have to say this week.

The FOMC meeting held last week was seen as slightly hawkish with the Fed expected to go ahead with its balance sheet unwinding from October and also signaled that rates could rise one more time. This has led to the odds for a rate hike increasing significantly to over 50% last week, following the FOMC meeting and statement.

On the economic front, data this week includes the PCE price index which is the Fed’s preferred inflation gauge. The core PCE price index is expected to remain steady at 1.4% on a year over year basis. The rate remains below the Fed’s 2% target rate and has fallen from January’s increase to 1.9%.

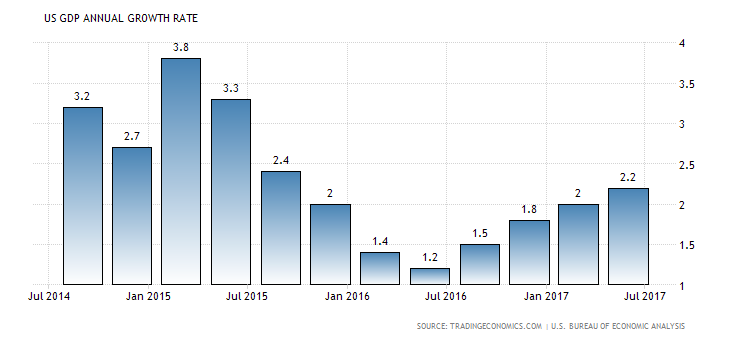

The U.S. final second-quarter GDP is also expected to be released this week. Economic activity is expected to be confirmed at 3% for the quarter ending June.

RBNZ expected to keep OCR unchanged

The Reserve Bank of New Zealand will be meeting next week on Wednesday. According to economists polled, the RBNZ will be holding the OCR steady at 1.75% at this week’s meeting.

Last week, New Zealand’s quarterly GDP data showed a 0.8% increase. This was in line with expectations and posted an annual GDP rate of 2.5% which was the same rate of increase in the first quarter. The previous quarter’s GDP was also slightly revised higher.

Despite modest numbers, the data is not expected to alter the RBNZ’s view on interest rates. In all probability, the central bank will likely maintain its views from the previous month’s meeting. Another key factor this week will be the weekend parliamentary elections being held in New Zealand.

The markets will be still waiting to hear the election verdict. In this context, the central bank is expected to play mute with no changes expected. The central bank is also likely to maintain its tone noting that monetary policy will remain accommodative and will be adjusted accordingly to the numerous uncertainties.

From the economic front, construction activity has seen a decline which was worse than what was estimated by the central bank. According to the latest GDP report, construction spending was weak, falling 3.2% during the first half of 2017. Taking this into consideration, the central bank is thus seen to be keeping the OCR unchanged at this week’s meeting.