The second week of April will see the inflation theme taking over the markets with data expected from the U.S., China, and the UK. Inflation in the U.S. and the UK is expected to rise at a slower pace, while consumer prices in China are expected to accelerate at a pace of 1.1%, following a 0.8% increase previously.

Fed chair, Janet Yellen is due to speak on Monday which could be the main event risk for the markets. Overall, the week ahead is likely to remain quiet with the focus mostly on the UK jobs while on the central bank meetings, the Bank of Canada is expected to keep interest rates steady. Here’s a quick preview of this week’s events.

U.S. Inflation and Retail Sales

The coming week will see the release of the monthly consumer price index data for the month of March. Economists surveyed are expecting a flat print in inflation while the core CPI is expected to rise 0.2% from February.

The main consensus for lower inflation this month is expected to come on the back of lower energy prices.

On a year over year basis, consumer prices are expected to rise 2.3% on the core while the headline consumer prices are expected to rise 2.8%. Despite the inflation figures likely to impact the markets, the Fed will be watching the PCE core inflation figures.

Retail sales figures are also expected to be released this week for March. In February, core retail sales rose 0.2% while headline retail sales rose 0.1% in February. The decline in retail sales came on the delayed tax refunds which were pending.

This is expected to pick up in March following the tax refund payments which is expected to give a boost to retail spending.

Besides the inflation and retail sales figures, Fed Chair Janet Yellen is expected to speak on Monday at the University of Michigan where she will also take audience questions.

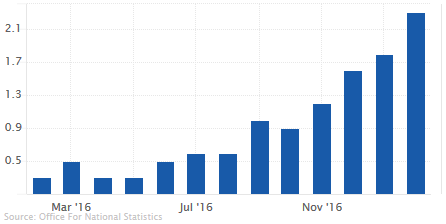

Eurozone Sentix Investor Confidence

The Eurozone Sentix investor confidence is forecast to show a reading of 20.1, slightly lower than 20.7 registered in March. The Sentix index touched a 10-year high in March with investors giving a favorable view of the current situation.

Thus, in the backdrop of the high reading in the index, the moderation is expected. Political uncertainty is expected to overshadow the economic performance in the eurozone.

The industrial production figures for February are also expected this week with forecasts suggesting a 0.2% increase on a month over month basis after rising to 0.9% previously. Most of the gains came from an increase in the German industrial production numbers.

Later in the week, the final inflation readings are expected from Germany and France which is expected to confirm headline inflation readings of 0.2% and 0.6% respectively.

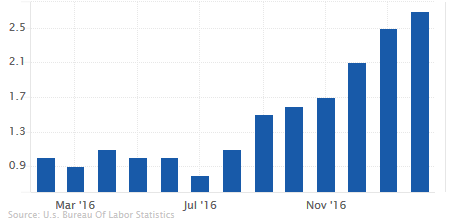

UK inflation expected to rise at a slower pace

The monthly inflation figures from the UK this week is expected to show a slower pace of increase in consumer prices. Economists are predicting a headline print of 2.2% on a year over year basis, while core CPI is expected to rise 1.8%.

This marks a slower pace of increase in consumer prices after rising to the highest level since September 2013. The decline in inflation is expected due to higher import prices. The Bank of England has signaled that it will be tolerating an overshoot of inflation in the short term.

Later in the week on Wednesday, the monthly jobs report for March is due. The 3-month unemployment rate is expected to remain unchanged at 4.7%. However, the focus will no doubt remain on the average weekly earnings which are expected to rise 2.1%, slower than 2.2% seen previously.

Another bout of a weaker pace of increase could infer that the real wage growth is starting to turn negative which could imply lower private consumption growth.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)