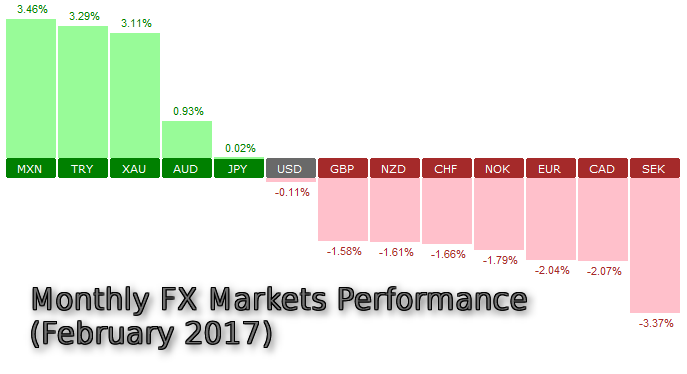

The month of February was short and rather mixed as far as the currency markets were concerned. The U.S. dollar was weaker, interestingly against the Mexican peso and the Turkish lira. Both these currencies came under immense pressure since November after Donald Trump won the elections. Both the respective central banks continued their efforts to hike interest rates and intervening in the currency markets, which looks to have paid off for the moment.

FX Markets – February 2017 Performance

ECB very likely to stay on the sidelines

With the upcoming Netherlands and French elections on the horizon, the European Central Bank’s meeting in March is unlikely to see any major changes. Furthermore, the ECB’s bond purchases will be tapered starting April at a pace of 60 billion euros from the current 80 billion. Therefore, the central bank is likely to focus on the dynamics of this taper and perhaps even paint an optimistic view on the economy.

The European economy has been sending positive signals so far, and despite the fact that the increase in consumer prices was led by higher energy prices, the fact remains that inflation edging closer to the ECB’s target range is something that is to be cheered for.

Monetary policy is thus likely to take a back seat with the ECB more likely pushed into the role of a cheerleader for the Eurozone’s economy amid looming threats of a political breakup of the economic union.

ECB Meeting: March 9, 2017

Will the Fed hike rates in March?

While the interest for a March rate hike was soft after a lackluster February FOMC statement, the testimony from Fed Chair Janet Yellen and subsequent hawkish narrative from other FOMC officials have rekindled hopes of a March rate hike. The odds of a 25 basis point increase has risen further more during the last week of February with tomorrow’s speech from Fed Chair Janet Yellen likely to be closely watched by investors. So far, the economic landscape continues to look positive which warrants a rate hike in March.

However, data next week will be a key part to the rate hike expectations for March as a bad jobs report could seriously dent the hawkish prospects of a rate hike and even cast doubts on the three rate hike plans from the Fed for this year. Traders will be likely watching the uptick in wages with the average number of jobs and the unemployment rate more or less anchored to the Fed’s full employment mandate.

FOMC Meeting: March 15, 2017

Will Britain trigger Article 50?

Latest reports, at the time of writing, suggest that PM Theresa May will trigger Article 50 on March 15. This came on the back of the fact that the Brexit bill was defeated in the House of Lords by a vote of 358 to 256.

Despite being defeated, the Brexit bill still gives power to the British PM to invoke Article 50 and start off formal exit negotiations with the EU. The British pound has been particularly vulnerable to the political developments out of the UK. Earlier this week, reports emerged that Scotland might prepare to hold a second independence referendum, which could potentially shake up the UK. A majority of votes from Scotland voted to remain in the EU during late June’s Brexit referendum.

Beside the political developments, the UK’s economy has also started to show signs of weakness with the manufacturing and construction PMI numbers showing a slowdown alongside stagnant wage growth. The Bank of England will also be meeting this month in March but could be seen staying on the sidelines for the near term. The central bank could be seen in a wait and watch mode before further action could be taken.