Happy New Year!

Traders and investors will be looking to a busy first week of the year coming out of the Christmas and New Year break. The markets are closed on Monday across major trading hubs and the holiday shortened week will gain pace as latest data for December is released. In the U.S. FOMC meeting minutes, ISM surveys and Friday’s payrolls will be high on priority while in Eurozone, Markit PMI’s and flash inflation estimates will be on the agenda. Besides the U.S., Canada will also be report the jobs numbers for December on Friday.

U.S. Payrolls report for December

The pace of hiring in the U.S. has slowed down in recent months, but the unemployment rate looks to be relatively stable. The U.S. economy has been consistently adding 170k – 180k jobs in the past few months and the same trend is likely to continue. Although on a week to week basis, the weekly unemployment claims have edged higher, the long term average remains below the 300k mark indicating that further slack could be absorbed. After last month’s unemployment rate fell to 4.6%, marking a nine-month low, the unemployment rate is expected to rise to 4.7%. On the December payrolls, expectations call for 173k jobs in line with the previous trend.

Last month’s unemployment report however showed a decline of 0.1% in the average hourly earnings on a month over month basis. However, economists are hopeful that the average hourly earnings will rise 0.3% in December, pushing the year over year average hourly earnings back closer to the 2.7% region after the year over year rate slipped to 2.5%.

Ahead of Friday’s payrolls report, Wednesday’s ADP private payrolls is expected to come out with a headline print of 173k. This marks a slight decline compared to November’s solid print of 203k. Services sector is likely to continue to drive jobs in the private sector. However, any downside revisions to previous months could see the markets take a cautious view ahead of Friday’s payrolls release.

ISM manufacturing and non-manufacturing PMI expected to rise

The manufacturing and non-manufacturing activity in the U.S is expected to post another increase in December. The ISM’s manufacturing PMI is expected to rise to 53.5. This is slightly higher than November’s print of 53.2. The ISM price paid for December is however expected to show a strong increase with forecasts pointing to 56.0, up from November’s 54.5. The recent leading indicators from the regional manufacturing surveys are likely to ascertain the potential for a beat on the forecasts in the ISM’s Manufacturing PMI report which will be coming out on Tuesday.

The non-manufacturing PMI data for December is expected rise to 56.7 as the non-manufacturing sector is expected to maintain the gains from November’s print of 57.2. The non-manufacturing PMI will be released on Thursday.

The FOMC meeting minutes will also be additional event risk for the markets. It is quite likely that the meeting minutes could more hawkish than expected, although with the Fed signaling three rate hikes in 2017 the markets look to be well prepared.

Eurozone Markit PMI’s and flash inflation estimates

Data from Europe kicks off from Monday with Markit’s manufacturing PMI for Germany and the Eurozone lined up. No major changes are expected. Tuesday will mark data from Germany which includes inflation and unemployment data. Germany’s unemployment rate is expected to remain stable at 6.0% on a month over month basis, seasonally adjusted. Preliminary inflation figures out of Germany are expected to show a strong increase in the headline print of 1.5%, up from 0.8% previously on a year over year basis. The Services PMI scheduled for Wednesday is expected to show that the Eurozone services PMI remained steady at 53.1, while the composite PMI is also expected to be stable at 53.9.

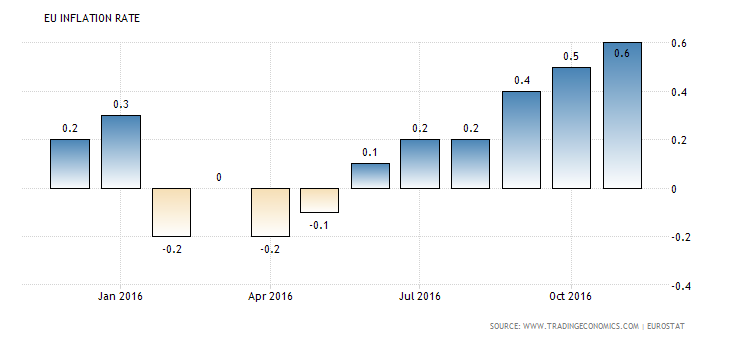

Eurozone’s flash CPI estimates are due on Wednesday and data is expected to show an increase of 1.0% on the headline CPI for December, which could be encouraging for the ECB. Core CPI is however expected to remain steady at 0.8% for the period.

Later in the week, retail sales figures and factory orders data will be coming out of Germany followed by consumer confidence and economic sentiment data expected to show a modest improvement.