The last trading week of the third quarter closed with risk aversion led by weakness in the banking sector. Wells Fargo and Deutsche Bank remained in the forefront, erasing gains from the surprise decision by OPEC to limit production levels. Looking ahead, the economic data this week that stands out will be the ISM surveys and the September jobs report, which is the first of the three jobs report before the December FOMC meeting.

ISM surveys looking to rebound, payrolls expected to rise

In August, the ISM manufacturing and non-manufacturing surveys surprised to the downside. The manufacturing PMI fell below 50 for the first time this year to 49.4 highlighting the uncertainty in the manufacturing sector after averaging around 50.2 over the past 12-months.

The weakness in the data for August brought back questions on the health of the manufacturing sector which had posted five consecutive months of expansion between March and July. In August, manufacturers exposed to commodities were the biggest hit with declining conditions in the construction equipment sector. If that wasn’t enough, the non-manufacturing PMI or services PMI fell by 4.1 points to 51.4 in August.

The services PMI report said that growth in the services sector continued to expand at a slower rate. Both the reports combined quickly shifted market expectations for the Fed to hold interest rates steady in September, which it did.

For September, the median estimates point to a 50.4 reading in the manufacturing survey while ISM’s services PMI is expected to recover by 1.7 points to 53.1. The expectation for recovery was driven by regional manufacturing surveys which came out broadly positive.

Thoughts on ISM manufacturing and non-manufacturing PMI

Although a recovery is expected, the data is unlikely to sustain a strong dollar buying. For traders, the question to ask is whether September’s turnaround (if it will), is a mere blip, or if the previous slow but steady increase in the sectors is back on track. Unless September’s ISM data shows a strong upside surprise, the markets are likely to take the data with a pinch of salt, awaiting further confirmation. Although still early, deterioration in the data will impact the expectations of a December rate hike.

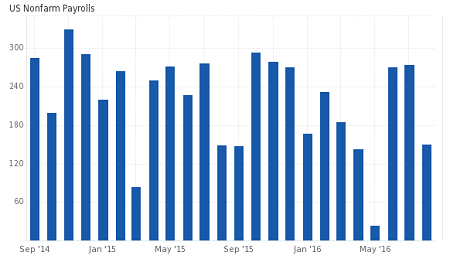

Higher expectations from September Jobs Report

The September jobs report is more optimistic with median estimates expecting to see a 171k headline print on the payrolls for the month. This follows Augusts’ 151k print. The US unemployment rate is expected to remain steady at 4.90% while the average hourly earnings are forecast to rise 2.60% on a year over year basis, higher than 2.40% registered in August. A match on the estimates here could push the average hourly earnings to the highs, close to July’s 2.70% year on year growth.

Expect to see revisions to the August data which could see an upside surprise, more than the initially reported 151k. A continued pace of hiring in September could potentially strengthen the expectations for the Fed to act in December. Wage growth will be another component to look to, as an increase in September could support the case for an increase in inflation.

UK PMI’s expected to moderate in September

After a strong performance in August, Markit’s manufacturing, services and construction PMI will be closely watched. Median estimates show that the PMI’s are expected to turn out soft, pulling back after posting a strong rebound in August. A weaker than expected print could potentially sour whatever bullish sentiment is left for the GBP, but on the flipside, a beat on the estimates could see the currency make some steady gains.

UK’s manufacturing and industrial production numbers are also up this week. Manufacturing is expected to recover, rising 0.40% in September while industrial production is forecast to rise 0.10%, same as in August. With the Bank of England signaling that a potential rate cut is likely in November, any hints of weakness in the PMI’s could strengthen the bearish case.