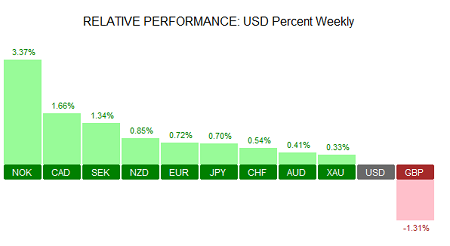

The US dollar closed the week as the second weakest currency, only next to the British pound. The US dollar fell sharply over the week but managed to recover some ground on late Friday. Data over the week included weak nonfarm productivity data for the second quarter and a flat retail sales print. Despite a weak print, gold prices settled modestly higher, gaining 0.33% for the week after multiple attempts to breakout above $1350 failed.

Although oil prices started off on a weaker note, Oil managed to close higher and thus led the oil related currencies, namely the NOK and CAD to outperform over the week. The Norwegian Krone closed the week with 3.37% gains relative to the US dollar, while the Canadian dollar came in second, rising 1.66%.

Economic Calendar for the Week 15/08 – 19/08

| Date | Time | Currency | Event | Forecast | Previous |

| 15-Aug | 00:50 | JPY | Prelim GDP q/q | 0.20% | 0.50% |

| JPY | Prelim GDP Price Index y/y | 0.70% | 0.90% | ||

| 05:30 | JPY | Revised Industrial Production m/m | 1.90% | 1.90% | |

| 08:15 | CHF | PPI m/m | -0.20% | 0.10% | |

| 13:30 | USD | Empire State Manufacturing Index | 2.1 | 0.6 | |

| 16-Aug | 02:30 | AUD | Monetary Policy Meeting Minutes | ||

| AUD | New Motor Vehicle Sales m/m | 3.10% | |||

| 09:30 | GBP | CPI y/y | 0.50% | 0.50% | |

| GBP | PPI Input m/m | 0.60% | 1.80% | ||

| GBP | RPI y/y | 1.70% | 1.60% | ||

| GBP | Core CPI y/y | 1.30% | 1.40% | ||

| GBP | HPI y/y | 8.30% | 8.10% | ||

| GBP | PPI Output m/m | 0.30% | 0.20% | ||

| 10:00 | EUR | German ZEW Economic Sentiment | 2.1 | -6.8 | |

| EUR | ZEW Economic Sentiment | -6.3 | -14.7 | ||

| EUR | Trade Balance | 23.2B | 24.5B | ||

| 13:30 | CAD | Manufacturing Sales m/m | 0.80% | -1.00% | |

| USD | Building Permits | 1.16M | 1.15M | ||

| USD | CPI m/m | 0.00% | 0.20% | ||

| USD | Core CPI m/m | 0.20% | 0.20% | ||

| USD | Housing Starts | 1.18M | 1.19M | ||

| 14:15 | USD | Capacity Utilization Rate | 75.70% | 75.40% | |

| USD | Industrial Production m/m | 0.20% | 0.60% | ||

| 23:45 | NZD | Employment Change q/q | 0.60% | 1.20% | |

| NZD | PPI Input q/q | -1.00% | |||

| NZD | Unemployment Rate | 5.30% | 5.70% | ||

| NZD | PPI Output q/q | -0.20% | |||

| 17-Aug | 02:30 | AUD | Wage Price Index q/q | 0.50% | 0.40% |

| 09:30 | GBP | Average Earnings Index 3m/y | 2.50% | 2.30% | |

| GBP | Claimant Count Change | 5.2K | 0.4K | ||

| GBP | Unemployment Rate | 4.90% | 4.90% | ||

| 18:00 | USD | FOMC Member Bullard Speaks | |||

| 19:00 | USD | FOMC Meeting Minutes | |||

| 18-Aug | 00:50 | JPY | Trade Balance | 0.14T | 0.33T |

| 02:30 | AUD | Employment Change | 10.2K | 7.9K | |

| AUD | Unemployment Rate | 5.80% | 5.80% | ||

| 09:00 | EUR | Current Account | 27.3B | 30.8B | |

| 09:30 | GBP | Retail Sales m/m | 0.10% | -0.90% | |

| 10:00 | EUR | Final CPI y/y | 0.20% | 0.20% | |

| EUR | Final Core CPI y/y | 0.90% | 0.90% | ||

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | |||

| USD | Philly Fed Manufacturing Index | 1.4 | -2.9 | ||

| USD | Unemployment Claims | 269K | 266K | ||

| 15:00 | USD | CB Leading Index m/m | 0.30% | 0.30% | |

| 15:05 | USD | FOMC Member Dudley Speaks | |||

| 19-Aug | 05:30 | JPY | All Industries Activity m/m | 0.90% | -1.00% |

| 07:00 | EUR | German PPI m/m | 0.10% | 0.40% | |

| 09:30 | GBP | Public Sector Net Borrowing | -2.3B | 7.3B | |

| 13:30 | CAD | Core CPI m/m | 0.00% | 0.00% | |

| CAD | Core Retail Sales m/m | 0.40% | 0.90% | ||

| CAD | CPI m/m | 0.00% | 0.20% | ||

| CAD | Retail Sales m/m | 0.80% | 0.20% |

Time: GMT+1

Currencies/Events to Watch this Week

AUD: The week ahead will see the release of the RBA’s meeting minutes on Tuesday. The meeting minutes cover the monetary policy meeting from earlier in August where the central bank cut interest rates by 25bps to 1.50%. Economic data is light during the mid-week and then follows the Australian unemployment report. Forecasts point to the unemployment rate staying unchanged at 5.80%, same as the month before in June. The economy is expected to show a net employment change of 9.9k – 10.2k.

NZD: After the RBNZ’s rate cut last week and a better than expected quarterly retail sales report, the week ahead will see the release of New Zealand’s quarterly employment change. Forecasts point to a 0.60% increase, which is slower than the first quarter’s 1.20% increase. New Zealand’s quarterly unemployment rate is also expected to show a decline to 5.30% in the second quarter, down from 5.70% seen in the first quarter.

JPY: Economic data from Japan this coming week will cover the preliminary GDP report for the second quarter. After posting solid gains of 0.50%, Japan’s economy is expected to rise at a slower pace of only 0.30%. The annualized GDP is expected to decline as a result with forecasts estimating an annual GDP growth rate of 0.80%, down from 1.90% in the first quarter. Industrial production and merchandise trade balance data make up for the remainder of the data.

EUR: Data from the Eurozone is fairly quiet this week, with Tuesday’s ZEW economic sentiment being the main release. German ZEW economic sentiment is forecast to rise 2.1 in August, while the Eurozone ZEW economic sentiment is expected to fall 6.30. Eurozone inflation data is also expected this week with estimates pointing to a 0.40% decline in headline CPI on a month over month basis. On a yearly basis, consumer prices are expected to inch higher, rising 0.20%. Later on Thursday, the ECB’s monetary policy meeting accounts will be released, but nothing much is expected following the ECB leaving policy unchanged.

GBP: It could turn out to be a big week for the British pound with the retail sales numbers coming out on Thursday. The retail sales data for July is expected to rise 0.10% excluding auto fuel while the headline retail sales are expected to fall to 4.10% in July compared to 4.30% in June. The retail sales report will be the first official release accounting for a full month after the Brexit vote which could have a potential surprise to the downside. UK inflation data will be on the tap on Tuesday. Headline CPI is expected to rise 0.50%, rising at the same pace as a month before while core CPI is expected the rise to 1.30%, compared to 1.40% year over year growth seen in June.

CAD: Data from Canada this week kicks off with Tuesday’s manufacturing sales report which is expected to show an increase of 0.80% in June following the 1.0% contraction in May. On Friday, inflation data from Canada is expected to show the annual inflation rate unchanged at 1.50%, while the BoC’s core CPI gauge is expected to remain steady at 2.10%. Retail sales numbers are also due on Friday with forecasts pointing to a 0.70% increase on a month over month basis.

USD: A busy week for the US starts on Tuesday with inflation data on the tap. Headline CPI is expected to remain unchanged in July on a month over month basis while rising 1.0% in July, the same pace as in June. Core CPI is expected remain steady at 2.30% on a year over year basis in July. Housing starts, building permits are also out on Tuesday and expected to show a moderate pace of increase in July following a strong pace of growth seen in June. On Wednesday, the FOMC meeting minutes will be the main event to watch out for. Fed members are also lined up this week starting with Lockhart, Bullard, Dudley and Williams speaking throughout the week.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)