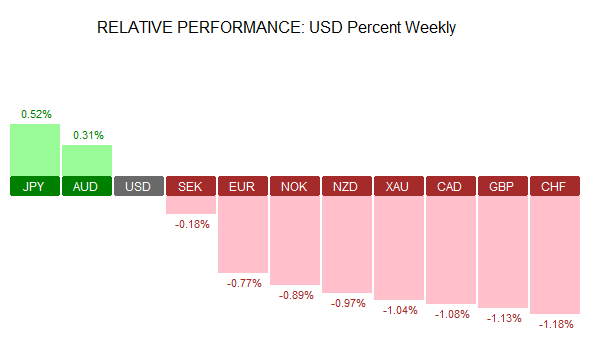

The US dollar managed to recover last week with most of the gains being attributed to last Friday’s payrolls report which managed to revive the dollar bulls. Still, the Japanese yen was the strongest currency last week, gaining 0.52% against the US dollar and emerging as the strongest currency overall. This was followed by the Australian dollar interestingly. Despite an interest rate cut by the RBA and the fact that the central bank expects inflation to remain low at the current levels the Australian dollar was trading stronger across the board.

On the weaker side, the British pound was seen closing the week 1.13% lower, but the Swiss franc was the weakest, down 1.180% on the week. The Canadian dollar was also one of the weaker currencies after Friday’s jobs report proved to be disappointing and Oil prices touching lows of $40 last week. Gold prices also closed weaker, down 0.97% after posting strong gains the week before.

Economic Calendar for the Week 08/08 – 12/08

| Date | Time | Currency | Event | Forecast | Previous |

| 08-Aug | 0:50 | JPY | Current Account | 1.60T | 1.41T |

| JPY | BOJ Summary of Opinions | ||||

| JPY | Bank Lending y/y | 2.00% | |||

| Tentative | CNY | Trade Balance | 313B | 311B | |

| Tentative | CNY | USD-Denominated Trade Balance | 47.6B | 48.1B | |

| 06:00 | JPY | Economy Watchers Sentiment | 42.6 | 41.2 | |

| 07:00 | EUR | German Industrial Production m/m | 0.90% | -1.30% | |

| 08:15 | CHF | CPI m/m | -0.50% | 0.10% | |

| 09:30 | EUR | Sentix Investor Confidence | 3.6 | 1.7 | |

| 13:30 | CAD | Building Permits m/m | 2.70% | -1.90% | |

| 15:00 | USD | Labor Market Conditions Index m/m | -1.9 | ||

| 09-Aug | 00:50 | JPY | M2 Money Stock y/y | 3.30% | 3.40% |

| CNY | CPI y/y | 1.70% | 1.90% | ||

| CNY | PPI y/y | -2.00% | -2.60% | ||

| 06:45 | CHF | Unemployment Rate | 3.30% | 3.30% | |

| 07:00 | EUR | German Trade Balance | 23.2B | 22.2B | |

| JPY | Prelim Machine Tool Orders y/y | -19.90% | |||

| 09:30 | GBP | Manufacturing Production m/m | 0.00% | -0.50% | |

| GBP | Goods Trade Balance | -9.6B | -9.9B | ||

| GBP | Industrial Production m/m | -0.10% | -0.50% | ||

| 11:00 | USD | NFIB Small Business Index | 94.5 | 94.5 | |

| 13:15 | CAD | Housing Starts | 196K | 218K | |

| 13:30 | USD | Prelim Nonfarm Productivity q/q | 0.50% | -0.60% | |

| USD | Prelim Unit Labor Costs q/q | 1.80% | 4.50% | ||

| 15:00 | GBP | NIESR GDP Estimate | 0.60% | ||

| USD | IBD/TIPP Economic Optimism | 46.2 | 45.5 | ||

| USD | Wholesale Inventories m/m | 0.00% | 0.10% | ||

| 10-Aug | 00:50 | JPY | Core Machinery Orders m/m | 3.40% | -1.40% |

| JPY | PPI y/y | -4.00% | -4.20% | ||

| 02:30 | AUD | Home Loans m/m | 2.40% | -1.00% | |

| 04:05 | AUD | RBA Gov Stevens Speaks | |||

| 05:30 | JPY | Tertiary Industry Activity m/m | 0.30% | -0.70% | |

| 07:45 | EUR | French Industrial Production m/m | 0.30% | -0.50% | |

| 22:00 | NZD | Official Cash Rate | 2.00% | 2.25% | |

| NZD | RBNZ Rate Statement | ||||

| NZD | RBNZ Monetary Policy Statement | ||||

| 22:05 | NZD | RBNZ Press Conference | |||

| 11-Aug | 02:00 | AUD | MI Inflation Expectations | 3.70% | |

| 07:45 | EUR | French Final CPI m/m | -0.40% | -0.40% | |

| 11th-16th | CNY | M2 Money Supply y/y | 11.10% | 11.80% | |

| 11th-16th | CNY | New Loans | 900B | 1380B | |

| 13:30 | CAD | NHPI m/m | 0.20% | 0.70% | |

| USD | Unemployment Claims | 272K | 269K | ||

| USD | Import Prices m/m | -0.20% | 0.20% | ||

| 23:30 | NZD | Business NZ Manufacturing Index | 57.7 | ||

| 23:45 | NZD | Retail Sales q/q | 1.00% | 0.80% | |

| NZD | Core Retail Sales q/q | 1.10% | 1.00% | ||

| 12-Aug | 03:00 | CNY | Industrial Production y/y | 6.20% | 6.20% |

| CNY | Fixed Asset Investment ytd/y | 8.90% | 9.00% | ||

| CNY | Retail Sales y/y | 10.50% | 10.60% | ||

| 07:00 | EUR | German Prelim GDP q/q | 0.30% | 0.70% | |

| EUR | German Final CPI m/m | 0.30% | 0.30% | ||

| EUR | German WPI m/m | 0.30% | 0.60% | ||

| 07:45 | EUR | French Prelim Non-Farm Payrolls q/q | 0.20% | 0.30% | |

| 09:00 | EUR | Italian Prelim GDP q/q | 0.20% | 0.30% | |

| 09:30 | GBP | Construction Output m/m | 0.90% | -2.10% | |

| 10:00 | EUR | Flash GDP q/q | 0.30% | 0.30% | |

| EUR | Industrial Production m/m | 0.60% | -1.20% | ||

| 13:30 | USD | Core Retail Sales m/m | 0.20% | 0.70% | |

| USD | PPI m/m | 0.10% | 0.50% | ||

| USD | Retail Sales m/m | 0.40% | 0.60% | ||

| USD | Core PPI m/m | 0.20% | 0.40% | ||

| 15:00 | USD | Prelim UoM Consumer Sentiment | 91.5 | 90 | |

| USD | Business Inventories m/m | 0.10% | 0.20% | ||

| USD | Prelim UoM Inflation Expectations | 2.70% |

Time: GMT+1

Currencies/Events to Watch this Week

AUD: After last week’s rate cut and inflation outlook failed to change the status quo in the AUD, the week ahead is relatively soft with no major events scheduled, save for the RBA Gov. Steven’s speech. The Aussie dollar is, therefore, more likely to take its cues from the strength of the US dollar and the general market sentiment. Home loans are expected to rise 2.40% in June following a 1.0% decline the month before.

NZD: The Reserve Bank of New Zealand will be the main focus next week as the central bank is expected to cut the official cash rate by 25bps. Following the weak inflation outlook from the RBNZ a few weeks ago, the expectation for a rate cut has been priced in already. The NZD could, therefore, be at risk of the RBNZ’s forward guidance. Many economists expect the RBNZ to eventually lower the OCR rate to 1.75% by the end of 2016. On Thursday, retail sales will be on the tap and is expected to show a 1.0% increase in the second quarter, following a slower than expected increase of 0.80% in the first quarter.

JPY: Japan is likely to stay on the sidelines this week with no major events coming out. The economy watchers sentiment is expected to improve to 42.6 from 41.2 while the machinery orders and industry activity make up the remainder of the events. Watch for PPI from Japan which is forecast to fall 4.0%, less than the previous print of a 4.20% decline.

EUR: In the eurozone, the focus will be on industrial production numbers. In Germany, industrial production is expected to reverse May’s decline of 1.30% with the median consensus showing a 0.90% expected increase. Overall, the industrial production data in the Eurozone is expected to show a positive reversal in June. Preliminary GDP numbers will also be released over the week, with Germany’s GDP expected to slow to 0.30% in the second quarter, while the Eurozone’s GDP is expected to remain unchanged at 0.30%.

GBP: Still reeling from the BoE rate cuts and asset purchase increases, the GBP will be looking to the manufacturing and industrial production numbers. Estimates show no change to manufacturing production on a month over month basis, while industrial production is expected to decrease 0.10%. The data still covers the most part of June which is, therefore, unlikely to impact the British pound. NIESR will be releasing the GDP estimates.

CAD: A slow week in Canada, building permits, and housing starts are the only two events coming out over the week. Building permits are expected to rise 2.70% in June following the 1.90 declines the month before, while housing starts are expected to rise 196k, down from 218k seen earlier.

USD: The economic calendar from the US is slow for the first part of the week. The only big events to look at over next week are the data from Friday which covers retail sales and PPI for July. Retail sales are expected to grow, but forecasts point to a slower pace of gains. Core, retail sales data, is forecast to rise 0.20% down from 0.70% increase, seen a month before. The headline retail sales are forecast to rise 0.40%. Producer price index is expected to remain moderate, forecast to rise 0.10% on the headline and 0.20% on the core, slightly lower than June’s print.

CNY: The week ahead is data heavy for China. Import and export data is forecast to fall compared to a year ago and could result in a worsening trade balance. Other big events from China include the retail sales, industrial production numbers and fixed asset investment. Inflation figures will be released on Tuesday and forecast points to a slower than expected increase of 1.70%, down from 1.90% seen a month before. PPI is however expected to continue to improve with forecasts pointing to a 2.0% decline.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)