Image via © European Union 2016 – European Parliament

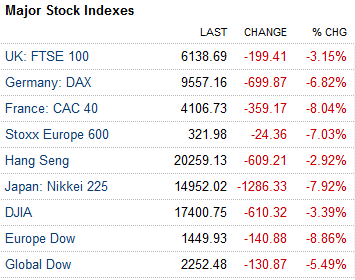

The UK referendum vote stunned the world! In what seemed like a clear victory for Camp Remain, the markets were shocked to see the EU referendum vote win with the Camp Leave voting 51.90%. The outcome of the referendum has indeed upset the status quo in a Eurozone that has often seen countries squabble over a myriad of things: be it the Greece debt crisis or the Syrian migrant crisis. What follows next is obvious. Another summer and perhaps autumn of uncertainty, this time with the European and the UK economies at stake, to a certain extent the global economies as well.

It seems like ages ago, but it was only last year, January – August 2015 that the political drama quickly steamrolled into what was then termed as a ‘Grexit,’ putting Greece on the brink of an exit from the European Union. But back then the uncertainty was largely contained.

The Brexit referendum, on the other hand, has kind of opened Pandora’s Box with larger implications, reaching as far as Washington and Tokyo. By Friday’s close, the global markets plunged and more is likely to follow in the coming week.

Brexit, 2016 “Dark clouds of uncertainty still linger”

The Brexit narrative finds a starkly similar story line, with the exception of the debt crisis of course. The markets are still in uncharted territory, and the EU leaders from Germany, France and Italy along with other EU members (27) meet on Monday. While the now famous, Article 50 has not yet been triggered, the UK had its fair share of political drama as well. PM David Cameron resigned hours after the Brexit verdict was delivered. The ‘Camp Leave’ most famous face, Boris Johnson urged not to rush into the legal proceedings, while the UK is likely to sit on the fence until a new Prime Minister is elected. While the UK leaders took a more calm approach to the referendum, some EU leaders were quick to set the ball rolling calling to put an end to the uncertainty.

“We now expect the United Kingdom government to give effect to this decision of the British people as soon as possible, however painful that process may be. Any delay would unnecessarily prolong uncertainty.” (Joint statement by President Tusk, President Schulz, and Netherlands Prime Minister Rutte).

On Saturday, other EU leaders joined in, calling for a swift exit from the EU with France’s foreign minister, Jean-Marc Ayrault saying ”It is in the interest of Britain and in the interest of Europeans not to have a period of uncertainty that would have financial consequences, and that could have economic and political consequences.” But it was clearly a mixed response with German Chancellor Angela Merkel saying “The facts are such that the U.K. has to decide for itself when it wants to submit its request.”

The UK is also now likely to face a backlash from the Scottish National Party after the first minister; Nicola Sturgeon called the Brexit verdict “constitutionally unacceptable” after Scots voted in favor of Remain and said it was highly likely that a second Scottish Referendum vote would be held. Latest news reports show that Londoners signed a petition for their metropolis to stay in the European Union further adding to the uncertainty on the repercussions of the Brexit vote.

Brexit Fallout – Monetary Policy Uncertainty

Many speculate that the Bank of England will cut rates as early as July. However, that is left to be seen as there are many unknowns. Making a policy decision as early as July would be detrimental for the BoE and could potentially backfire in the long run once real negotiations start on charting the course for an exit from the EU. With interest rates near record lows of 0.50%, the BoE is likely to buy time than to cut rates as a reactionary response and end up with its back against the walls when the time for rate cuts are really needed. Following the Brexit verdict, BoE Governor, Mark Carney said that the bank was ready to inject £250 million to maintain liquidity in the markets. As a worst case scenario, the BoE could be looking at expanding its asset purchases rather than cutting interest rates. The July BoE meeting will, therefore, be another big event to watch for, from a central bank that has stood on the sidelines for a long time.

For the Eurozone, the ECB is slightly better off as the euro is likely to see a more limited reaction to the Brexit outcome. However, that is likely as long as the status quo remains. Following the Brexit reaction, the Eurosceptic parties lost no time to call for their own national referendums. Next year (around summer), France and Germany goes to polls as well and depending on how the events unfold, a lot is left hanging in the balance. EU leaders could use the Brexit event to either grow stronger together or it would be just another crisis that could deepen the already widening cracks.

Ahead of the EU referendum vote, ECB President Mario Draghi signaled a willingness to act just a day before the ECB launched its TLTRO-II program to encourage banks to boost lending. With more stimulus likely if the need arises, the euro is also likely to see further weakening in the medium term.

For its part, the Federal Reserve signaled that it would wait for the global headwinds to recede before the central bank could hike interest rates. But with the new developments, it is starting to look more uncertain on the timing of the next rate hike. Fed Chair Janet Yellen is due to speak later on in the week.

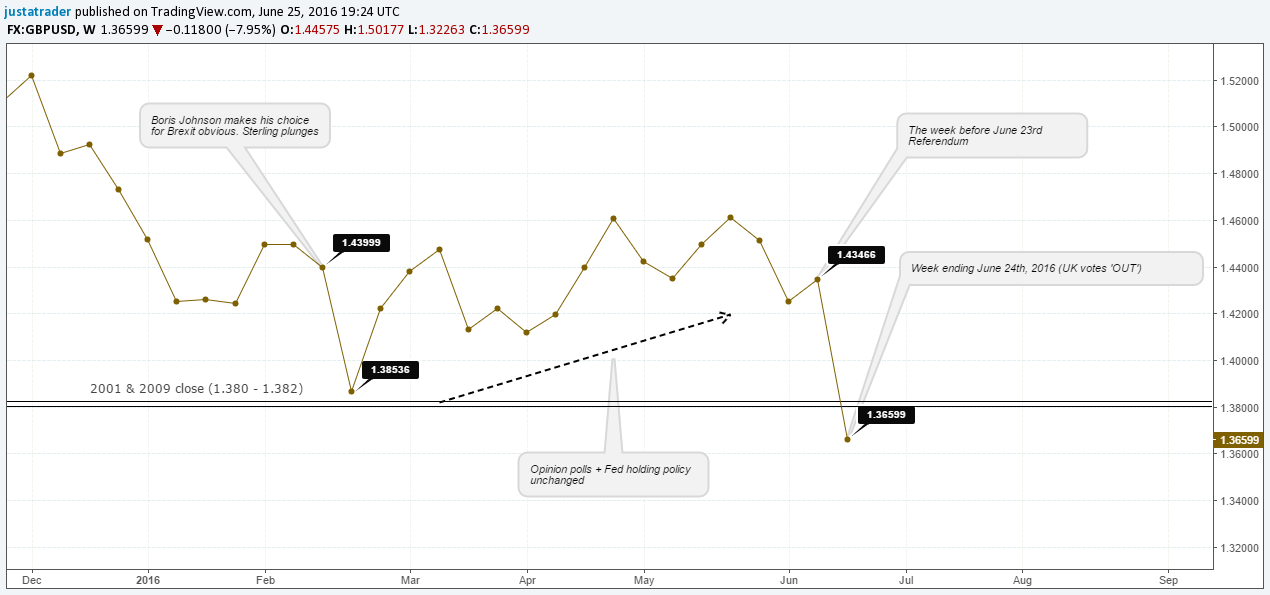

GBPUSD – Long Term Technical Outlook

The monthly chart for GBPUSD shows the ominous break of the head and shoulders neckline support near $1.47 and $1.40, with the right shoulder forming a bearish pennant pattern. Further declines are anticipated for a measured target to $1.2552 and $1.0309 over the longer term horizon. The only saving grace could be to see a price rejection near the current lows, in which case, GBPUSD could either stay range bound within 1.40 and 1.47, but still the downside remains intact. The view shifts only if we see a sustained break above 1.5713, in which case the sterling could see some upside potential build up.