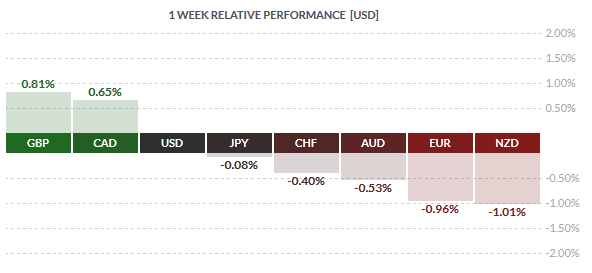

The British pound was the strongest currency last week, rising 0.81% against the US dollar. The Sterling gained as opinion polls suggested that the risks of the UK leaving the EU were ebbing, underlining the fact that the sterling was focusing more on the Brexit risks than the fundamentals. Last week saw the UK’s first quarter GDP coming out unchanged at 0.40% at the second revision. The Canadian dollar was the second best currency pair, rising 0.65%. The Bank of Canada left interest rates unchanged last week. The Loonie was also supported by stronger oil prices.

The NZD and the EUR were the weakest currencies last week, including the AUD. The commodity-linked currencies posted steady declines as gold prices continued to fall for the fourth consecutive week. For the euro, despite an upbeat German GDP data, monetary policy divergence was back pushing the single currency lower.

Fundamentals for the Week 30/05 – 03/06

| Date | Time | Currency | Detail | Forecast | Previous |

| 30-May | 00:50 | JPY | Retail Sales y/y | -1.20% | -1.00% |

| 01:20 | USD | FOMC Member Bullard Speaks | |||

| 02:00 | AUD | HIA New Home Sales m/m | 8.90% | ||

| 02:30 | AUD | Company Operating Profits q/q | 0.50% | -2.80% | |

| 07:00 | EUR | German Import Prices m/m | 0.40% | 0.70% | |

| All Day | EUR | German Prelim CPI m/m | 0.30% | -0.40% | |

| 07:45 | EUR | French Consumer Spending m/m | 0.10% | 0.20% | |

| 08:00 | CHF | KOF Economic Barometer | 102.9 | 102.7 | |

| EUR | Spanish Flash CPI y/y | -1.00% | -1.10% | ||

| 13:30 | CAD | Current Account | -17.4B | -15.4B | |

| CAD | RMPI m/m | 2.20% | 4.50% | ||

| CAD | IPPI m/m | 0.20% | -0.60% | ||

| 23:45 | NZD | Building Consents m/m | -9.80% | ||

| 31-May | 00:30 | JPY | Household Spending y/y | -1.00% | -5.30% |

| JPY | Unemployment Rate | 3.20% | 3.20% | ||

| 00:50 | JPY | Prelim Industrial Production m/m | -1.40% | 3.80% | |

| 02:00 | NZD | ANZ Business Confidence | 6.2 | ||

| 02:30 | AUD | Building Approvals m/m | -2.80% | 3.70% | |

| AUD | Current Account | -19.3B | -21.1B | ||

| AUD | Private Sector Credit m/m | 0.50% | 0.40% | ||

| 06:00 | JPY | Housing Starts y/y | 3.90% | 8.40% | |

| 07:00 | EUR | German Retail Sales m/m | 1.10% | -1.10% | |

| 07:45 | EUR | French Prelim CPI m/m | 0.30% | 0.10% | |

| 08:55 | EUR | German Unemployment Change | -4K | -16K | |

| 09:00 | EUR | M3 Money Supply y/y | 5.00% | 5.00% | |

| EUR | Private Loans y/y | 1.50% | 1.60% | ||

| 10:00 | EUR | CPI Flash Estimate y/y | -0.10% | -0.20% | |

| EUR | Core CPI Flash Estimate y/y | 0.80% | 0.70% | ||

| EUR | Italian Prelim CPI m/m | 0.20% | -0.10% | ||

| EUR | Unemployment Rate | 10.20% | 10.20% | ||

| 13:30 | CAD | GDP m/m | 0.00% | -0.10% | |

| USD | Core PCE Price Index m/m | 0.20% | 0.10% | ||

| USD | Personal Spending m/m | 0.60% | 0.10% | ||

| USD | Personal Income m/m | 0.40% | 0.40% | ||

| 14:00 | USD | S&P/CS Composite-20 HPI y/y | 5.10% | 5.40% | |

| 14:45 | USD | Chicago PMI | 50.8 | 50.4 | |

| 15:00 | USD | CB Consumer Confidence | 96.1 | 94.2 | |

| 23:45 | NZD | Overseas Trade Index q/q | -2.00% | ||

| 01-Jun | 00:01 | GBP | BRC Shop Price Index y/y | -1.70% | |

| 00:30 | AUD | AIG Manufacturing Index | 53.4 | ||

| 00:50 | JPY | Capital Spending q/y | 1.90% | 8.50% | |

| 02:00 | CNY | Manufacturing PMI | 50 | 50.1 | |

| CNY | Non-Manufacturing PMI | 53.5 | |||

| 02:30 | AUD | GDP q/q | 0.60% | 0.60% | |

| 02:45 | CNY | Caixin Manufacturing PMI | 49.3 | 49.4 | |

| 03:00 | JPY | Final Manufacturing PMI | 47.6 | 47.6 | |

| 06:45 | CHF | GDP q/q | 0.30% | 0.40% | |

| 07:00 | GBP | Nationwide HPI m/m | 0.30% | 0.20% | |

| 07:30 | AUD | Commodity Prices y/y | -9.40% | ||

| 08:15 | CHF | Retail Sales y/y | -0.80% | -1.30% | |

| EUR | Spanish Manufacturing PMI | 52.6 | 53.5 | ||

| 08:30 | CHF | Manufacturing PMI | 54.2 | 54.7 | |

| 08:45 | EUR | Italian Manufacturing PMI | 53.5 | 53.9 | |

| 08:50 | EUR | French Final Manufacturing PMI | 48.3 | 48.3 | |

| 08:55 | EUR | German Final Manufacturing PMI | 52.5 | 52.4 | |

| 09:00 | EUR | Final Manufacturing PMI | 51.5 | 51.5 | |

| 09:30 | GBP | Manufacturing PMI | 49.6 | 49.2 | |

| GBP | Net Lending to Individuals m/m | 5.3B | 9.3B | ||

| GBP | M4 Money Supply m/m | 0.20% | -0.40% | ||

| GBP | Mortgage Approvals | 68K | 71K | ||

| 14:30 | CAD | RBC Manufacturing PMI | 52.2 | ||

| 14:45 | USD | Final Manufacturing PMI | 50.5 | 50.5 | |

| 15:00 | USD | ISM Manufacturing PMI | 50.6 | 50.8 | |

| USD | Construction Spending m/m | 0.50% | 0.30% | ||

| USD | ISM Manufacturing Prices | 58 | 59 | ||

| All Day | USD | Total Vehicle Sales | 17.2M | 17.4M | |

| Tentative | NZD | GDT Price Index | 2.60% | ||

| 02-Jun | 00:50 | JPY | Monetary Base y/y | 27.20% | 26.80% |

| 02:30 | AUD | Retail Sales m/m | 0.30% | 0.40% | |

| AUD | Trade Balance | -2.11B | -2.16B | ||

| 06:00 | JPY | Consumer Confidence | 40.4 | 40.8 | |

| 08:00 | EUR | Spanish Unemployment Change | -110.0K | -83.6K | |

| 09:30 | GBP | Construction PMI | 52.1 | 52 | |

| 10:00 | EUR | PPI m/m | 0.10% | 0.30% | |

| All Day | ALL | OPEC Meetings | |||

| 12:45 | EUR | Minimum Bid Rate | 0.00% | 0.00% | |

| 13:15 | USD | ADP Non-Farm Employment Change | 179K | 156K | |

| 13:30 | EUR | ECB Press Conference | |||

| USD | Unemployment Claims | 271K | 268K | ||

| 13:35 | USD | FOMC Member Powell Speaks | |||

| 16:00 | USD | Crude Oil Inventories | -4.2M | ||

| 03-Jun | 01:00 | JPY | Average Cash Earnings y/y | 0.90% | 1.50% |

| 02:00 | NZD | ANZ Commodity Prices m/m | -0.80% | ||

| 02:45 | CNY | Caixin Services PMI | 52 | 51.8 | |

| 08:15 | EUR | Spanish Services PMI | 55.6 | 55.1 | |

| 08:45 | EUR | Italian Services PMI | 52.3 | 52.1 | |

| 08:50 | EUR | French Final Services PMI | 51.8 | 51.8 | |

| 08:55 | EUR | German Final Services PMI | 55.2 | 55.2 | |

| 09:00 | EUR | Final Services PMI | 53.1 | 53.1 | |

| 09:30 | GBP | Services PMI | 52.3 | 52.3 | |

| 10:00 | EUR | Retail Sales m/m | 0.40% | -0.50% | |

| 13:30 | CAD | Trade Balance | -2.6B | -3.4B | |

| CAD | Labor Productivity q/q | 0.10% | |||

| USD | Average Hourly Earnings m/m | 0.20% | 0.30% | ||

| USD | Non-Farm Employment Change | 160K | 160K | ||

| USD | Unemployment Rate | 4.90% | 5.00% | ||

| USD | Trade Balance | -41.9B | -40.4B | ||

| 14:45 | USD | Final Services PMI | 51.2 | 51.2 | |

| 15:00 | USD | ISM Non-Manufacturing PMI | 55.4 | 55.7 | |

| USD | Factory Orders m/m | 0.90% | 1.10% |

Time: GMT+1

Currencies/Events to Watch this Week

AUD: The first quarter GDP data will be the main event to watch for and one which could shift the tide in the AUD’s declines. Economists are looking at 0.60% quarter over quarter growth, same as the previous quarter. On a yearly basis, Australia’s GDP is expected to rise at a slower pace of 2.70% compared the 3.0% annualized GDP growth seen in the previous quarter. A weaker print could likely spur more AUD bears to keep the selling pressure on the Aussie. On Thursday, retail sales numbers will be out and is expected to show a modest increase of 0.30%, down from 0.40% increase seen in March.

NZD: Economic data from New Zealand this week is fairly limited. Building consents are due on Monday while overseas trade index is expected on Tuesday, for the first quarter. The bi-weekly GDT price index is expected on Wednesday with the previous print showing an increase to 2.60% reversing the previous print of 1.40% decline.

JPY: It is likely to be a slow week for the yen next week with the unemployment rate coming out on Monday. Expectations show an unchanged print of 3.20%. Industrial production data is due later and is forecasted to decline 1.50%, down from March’s 3.80% on a monthly basis while on a year over year basis, Japan’s industrial production is expected to fall 5.20%, which is one of the strongest yearly declines since 2014. Later in the week, manufacturing PMI is due followed up by BoJ’s board member, Sato’s speech.

CNY: From China, the markets will be looking to the manufacturing and services PMI this week. Manufacturing PMI is expected to slip to 50.0 in May, which could erase the gains made since March’s increase to 50.2. The Caixin manufacturing PMI is expected to show a contraction with estimates pointing to a slowdown to 49.2 in May from 49.4 in April. On the services side, the Caixin services PMI is expected to rise to 52.0 from 51.8 in April.

EUR: Data from the Eurozone this week will start with inflation estimates. Forecasts are for confirmation that the Eurozone economy slipped into deflation in May, with CPI expected to fall 0.10% on a year over year basis in May. The core CPI, on the other hand, is expected to be steady at 0.70%. The ECB will be meeting next week on June 2nd for its monetary policy meeting. No changes are expected at this event. On Friday, retail sales numbers are expected to show a potential rebound, with sales expected to rise 0.20% in April, after falling 0.50% in March.

CHF: Data from Switzerland this week will include the quarterly GDP report. Estimates point to a 0.20% quarterly increase in GDP in the first quarter of 2016. This is slower than the 0.40% quarterly GDP growth seen in Q4 2015. On an annualized basis, however, Swiss GDP is expected to expand 0.90%, up from 0.40% in the previous quarter.

GBP: From the UK PMI data will be in focus. Manufacturing PMI is expected to moderate with estimates pointing to increase to 49.6 in May, up from 49.2 in April. Construction and services PMI are expected to tick modestly higher.

CAD: From Canada, the markets will be looking to the monthly GDP numbers. Expectations call for a no change to the GDP in March, which follows February’s 0.10% declines. On a quarterly basis, the annualized GDP is expected to rise 2.80%, up from 0.80% in the previous quarter.

USD: A busy week for the US after the markets re-opens on Monday. The PCE price index is expected to rise 1.10%, posting a strong rebound from 0.80% increase seen in March. The Core PCE Price index is expected to rise 1.60% on a year over year basis. On Wednesday, the ISM manufacturing index will be in focus with expectations showing a soft decline to 50.5 in May, from 50.8 in April, while ISM prices paid is expected to slip to 58 from 59.0 in April. Thursday will see the private payrolls report from ADP, which is expected to show a 178k increase in May, up from 156k jobs in April. The ADP report will set the stage for the monthly NFP data on Friday. The US unemployment rate is expected to fall to 4.90%, from 5.0% while the monthly nonfarm payrolls are expected to show 160k jobs being added to the economy.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)