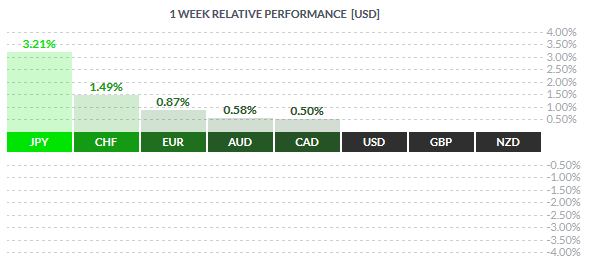

The markets continued another week in a risk aversion mode with the equities continuing to push lower. WTI Crude oil prices were trending lower during the week with prices briefly trading near 13-year lows during the week. The Yen and the Swiss Franc continued to remain strong during the week, gaining over 3.0% and 1.4% respectively. However, by late Friday, the US Dollar showed signs of a recovery led by modestly better retail sales data and comments from some BoJ officials.

The week ahead will see some important economic releases. More importantly, China will be back in the headlines as the world’s second-largest economy is set to release its inflation and PPI data which will no doubt shape the market sentiment this week.

Fundamentals for the Week 15/02 – 19/02

| Date | Time | Currency | Detail | Forecast | Previous |

| 15-Feb | 01:50 | JPY | Prelim GDP q/q | -0.20% | 0.30% |

| JPY | Prelim GDP Price Index y/y | 1.60% | 1.80% | ||

| 02:30 | AUD | New Motor Vehicle Sales m/m | -0.50% | ||

| Tentative | CNY | Trade Balance | 389B | 382B | |

| Tentative | CNY | USD-Denominated Trade Balance | 60.6B | 60.1B | |

| 06:30 | JPY | Revised Industrial Production m/m | -1.30% | -1.40% | |

| JPY | Tertiary Industry Activity m/m | 0.10% | -0.80% | ||

| 12:00 | EUR | Trade Balance | 22.4B | 22.7B | |

| 16:00 | EUR | ECB President Draghi Speaks | |||

| 23:45 | NZD | Retail Sales q/q | 1.50% | 1.60% | |

| NZD | Core Retail Sales q/q | 1.10% | 1.00% | ||

| 16-Feb | 02:30 | AUD | Monetary Policy Meeting Minutes | ||

| 04:00 | NZD | Inflation Expectations q/q | 1.90% | ||

| Tentative | EUR | German Constitutional Court Ruling | |||

| 11:30 | GBP | CPI y/y | 0.30% | 0.20% | |

| GBP | PPI Input m/m | -1.20% | -0.80% | ||

| GBP | RPI y/y | 1.40% | 1.20% | ||

| GBP | Core CPI y/y | 1.30% | 1.40% | ||

| GBP | HPI y/y | 7.90% | 7.70% | ||

| GBP | PPI Output m/m | -0.20% | -0.20% | ||

| 12:00 | EUR | German ZEW Economic Sentiment | 0.1 | 10.2 | |

| EUR | ZEW Economic Sentiment | 10.3 | 22.7 | ||

| 15:30 | CAD | Manufacturing Sales m/m | 0.90% | 1.00% | |

| USD | Empire State Manufacturing Index | -10 | -19.4 | ||

| Tentative | NZD | GDT Price Index | -7.40% | ||

| 17:00 | USD | NAHB Housing Market Index | 60 | 60 | |

| 23:00 | USD | TIC Long-Term Purchases | 31.4B | ||

| 17-Feb | 01:50 | JPY | Core Machinery Orders m/m | 4.80% | -14.40% |

| 17th-19th | CNY | Foreign Direct Investment ytd/y | 6.40% | ||

| 11:30 | GBP | Average Earnings Index 3m/y | 1.90% | 2.00% | |

| GBP | Claimant Count Change | -2.9K | -4.3K | ||

| GBP | Unemployment Rate | 5.00% | 5.10% | ||

| 12:00 | CHF | ZEW Economic Expectations | -3 | ||

| 15:30 | CAD | Foreign Securities Purchases | 2.58B | ||

| USD | Building Permits | 1.21M | 1.20M | ||

| USD | PPI m/m | -0.20% | -0.20% | ||

| USD | Core PPI m/m | 0.10% | 0.10% | ||

| USD | Housing Starts | 1.17M | 1.15M | ||

| 16:15 | USD | Capacity Utilization Rate | 76.70% | 76.50% | |

| USD | Industrial Production m/m | 0.30% | -0.40% | ||

| 21:00 | USD | FOMC Meeting Minutes | |||

| 23:45 | NZD | PPI Input q/q | 1.60% | ||

| NZD | PPI Output q/q | 1.30% | |||

| 18-Feb | 01:50 | JPY | Trade Balance | 0.06T | 0.04T |

| 02:30 | AUD | Employment Change | 13.2K | -1.0K | |

| AUD | Unemployment Rate | 5.80% | 5.80% | ||

| Tentative | AUD | RBA Assist Gov Edey Speaks | |||

| 03:00 | USD | FOMC Member Bullard Speaks | |||

| 03:30 | CNY | CPI y/y | 1.90% | 1.60% | |

| CNY | PPI y/y | -5.50% | -5.90% | ||

| 09:00 | CHF | Trade Balance | 2.67B | 2.54B | |

| Q4 Data | CHF | Employment Level | 4.25M | ||

| Q3 Data | CHF | Employment Level | 4.24M | 4.24M | |

| 11:00 | EUR | Current Account | 22.3B | 26.4B | |

| 14:30 | EUR | ECB Monetary Policy Meeting Accounts | |||

| 15:30 | CAD | Wholesale Sales m/m | -0.30% | 1.80% | |

| USD | Philly Fed Manufacturing Index | -3.1 | -3.5 | ||

| USD | Unemployment Claims | 275K | 269K | ||

| 17:00 | USD | CB Leading Index m/m | -0.10% | -0.20% | |

| 18:00 | USD | Crude Oil Inventories | -0.8M | ||

| 19-Feb | 09:00 | EUR | German PPI m/m | -0.30% | -0.50% |

| 11:30 | GBP | Retail Sales m/m | 0.90% | -1.00% | |

| GBP | Public Sector Net Borrowing | -13.7B | 6.9B | ||

| 15:30 | CAD | Core CPI m/m | 0.20% | -0.40% | |

| CAD | Core Retail Sales m/m | -0.50% | 1.10% | ||

| CAD | CPI m/m | 0.10% | -0.50% | ||

| CAD | Retail Sales m/m | -0.80% | 1.70% | ||

| USD | CPI m/m | -0.10% | -0.10% | ||

| USD | Core CPI m/m | 0.20% | 0.10% | ||

| 17:00 | EUR | Consumer Confidence | -7 | -6 |

Time: GMT+2

Currencies/Events to Watch this Week

AUD: The RBA meeting minutes from January will be released on Tuesday, 16th February followed by the monthly employment data on the 18th. Expectations are for the unemployment rate to remain steady at 5.80% while the average jobs added to the economy is expected to increase but 13.2k. The Australian dollar remains volatile however as China’s CPI numbers will be the other data that will impact the markets.

NZD: After a rather quiet week, data from New Zealand this week is expected to show a broadly positive picture. Retail sales for the quarter are expected to rise 1.50%, while the core retail sales are expected to rise 1.10%, following 1.0% increase in the previous quarter. The quarterly inflation expectations are also due later in the week.

CNY: After the markets closing for a week, China will be back in the news this week. Inflation numbers are due on Thursday, February 18th with China’s CPI expected to rise 1.90%, up from 1.60% increase previously. Producer price index is also expected to improve modestly declining -5.50%, down from -5.90% increase previously. Positive data could help boost the global market sentiment which has seen a strong sell-off since January.

JPY: Japan is set to release its quarterly GDP numbers on Monday. Expectations are dovish, with Japan’s quarterly GDP expected to decline -0.20% for the quarter including a slowdown in the GDP price index. While weak GDP numbers might put more pressure on the BoJ, an upside surprise could potentially see the Yen continue to remain the favorite amid the risk off sentiment. However, with the US Dollar trading at lows of 111Yen, talks of BoJ intervention will likely keep the USDJPY well supported to the upside.

EUR: ECB President Mario Draghi will be talking to the EU parliament on Monday. In light of the recent Euro appreciation, there is scope for the ECB Chief to use the opportunity to talk down the currency. In the absence of such, the Euro could remain well supported as prices will likely find support near $1.10. Besides Draghi’s speech other important data during the week include the German ZEW economic sentiment and ECB monetary policy meeting minutes from the January’s ECB monetary policy meeting.

GBP: The British Pound will have a busy week starting Tuesday where inflation numbers print a mixed picture. Headline CPI in the UK is expected to rise 0.30% while core inflation is expected to be soft, rising 1.20%. Following the inflation numbers, UK’s unemployment data is expected to show the unemployment rate fall to 5.0%, while the average earnings index is expected to show a further slowdown, rising only 1.90%. The week winds up with UK retail sales numbers with expectations of an increase of 0.90% for the month.

CAD: Data from Canada this week includes manufacturing sales, which is expected to rise 0.90% for the month. However, the more important monthly inflation data is due on Friday. Expectations are for Canada’s core CPI to rise 0.20%, after declining -0.40% previously, while headline CPI is expected to rise 0.10%, recovering after -0.50% decline a month ago. Retail sales numbers are also released at the same time but expectations are dovish as median consensus estimates point to -0.50% decline in the core retail sales while headline retail sales are expected to fall -0.80%.

USD: The US producer prices index is due on Wednesday and is expected to show the headline number declining -0.20% with the core PPI expected to rise 0.10%. Later in the day, the FOMC meeting minutes will be released which could add some significant volatility. Besides some Fed member speeches during the week, Friday will see the US inflation numbers which are expected to be mixed. Headline US CPI is expected to decline -0.10% while core CPI is expected to rise 0.20% for the month.