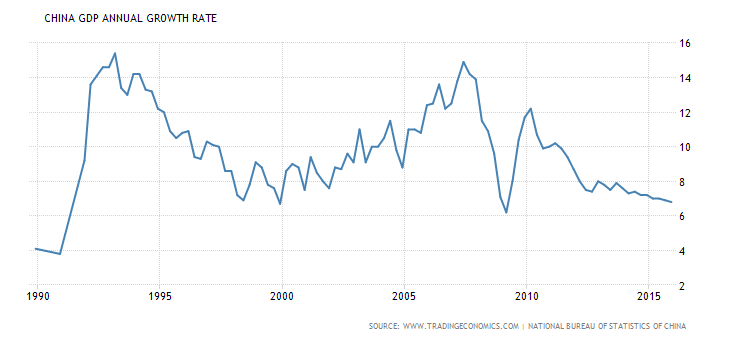

It was only less than a decade ago that China overtook Japan in 2005 to become the world’s second-largest economy. Powered by a population of over 1.3 billion, as a hitherto closed economy, China powered ahead after it undertook a series of economic reforms, growing at a rate of over 10% in over a decade. China emerged as a strong economy largely due to its manufacturing sector. Indeed, nowadays, it’s more common to find goods that are ‘Made in China‘ than the US or any other country for that matter. By maintaining a weak exchange rate against the US Dollar, the Chinese Yuan was able to make exports competitive against its peers while the Chinese authorities maintained strict control on capital flows, especially when it came to the US Dollars.

However, since the 2008 Global Financial Crisis where most of the developed economies took a strong hit, as well as emerging markets, demand for Chinese goods fell, bringing down the once strong GDP growth rate from above 10% to currently near the 7.0% growth rate.

In recent years, especially since 2015, the markets, in general, started paying more attention to Chinese data and the Yuan’s exchange rate. It gained, even more, prominence when last year, in November 2015, the Yuan was accepted into the IMF’s currency basket known as ‘Special Drawing Rights’ or SDR, prompting rumors that the Yuan could soon replace the US Dollar as the world’s reserve currency. Indeed, the Yuan now has proper frameworks in place for direct convertibility against currencies such as the British Pound, Russian Ruble to name few. Despite all the inroads made by China, the market concerns are largely due to the fact that a slowdown in China could have widespread repercussions on both developed and emerging economies with China’s exchange rate controls at the very core of the issue.

Here are a few reasons why the markets are concerned with China.

Exchange Rate Valuation

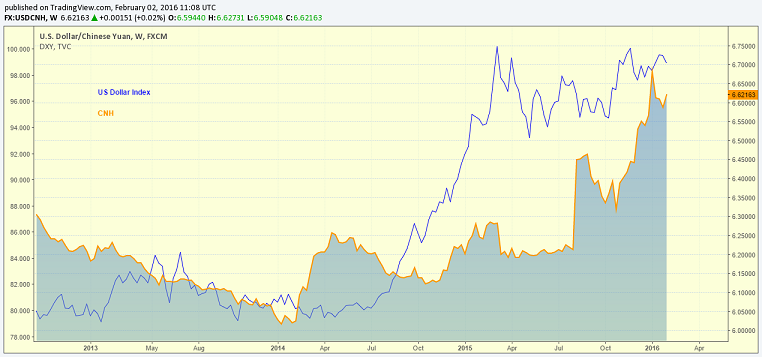

Up until 2005, the Yuan was strongly pegged to the US Dollar but in a bid to boost exports, it was further devalued to make Chinese goods more competitive in the global markets. As the Yuan grew in popularity, Chinese authorities allowed for a partial float against the US Dollar, making it trade within a price band. Currently, the US Dollar trades just under 7Yuan with the PBoC setting a daily average rate. Because the Yuan floats within a tight band to the US Dollar, the problem starts with the fact that with the US Dollar continuing to appreciate strongly against other economies, the Yuan also appreciated steadily, making Chinese goods more expensive than they were before. The chart below shows the Chinese Yuan overlaid with the US Dollar Trade Weighted Index and shows how the Yuan has in fact been appreciating along with the Greenback and the subsequent devaluations being undertaken by Chinese authorities in order to keep the Yuan more competitive.

When China eventually makes the Yuan free floating, there is no doubt that the US Dollar will decline against the Yuan which has been artificially kept lower. This would result in inflation being imported into the US as the Yuan grows in value making exports to the US, more expensive.

Slowing Demand

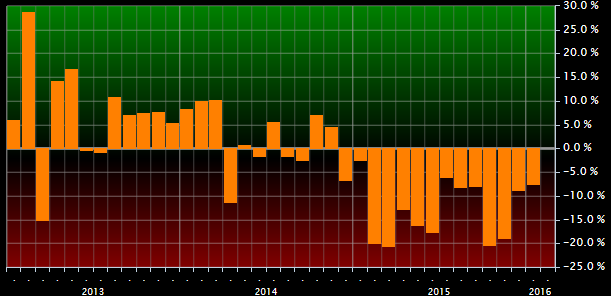

As the world’s second largest economy, China imports a lot of raw materials to sustain its manufacturing sector. In other words, when China slows down, imports of commodities and raw materials also fall taking a significant chunk of exports off many countries which inevitably add up to a loss in the GDP for the raw materials and commodity exporting countries.

A good illustration of this is Australia, which is one of the largest trading partners with China. According to estimates, in the first seven months of 2015, China’s demand fell by -14.6% which cost Australia close to 1.70% of GDP. By the end of 2015, China’s imports fell a total -13.2% compared to a year ago. As evidenced by the chart below, falling demand for raw materials and commodities from China tend to drag down a lot of export oriented economies as well.

Speculative Bets on the Yuan

A theme that played out in 2015 was that of the markets vs. artificially pegged currencies. It was only a matter of time before the Swiss Franc gave way and then it was the Russian Ruble, in the height of the US sanctions. The PBoC has led massive efforts into keeping the Yuan weak, and with the recent market volatility; it is more of a ‘When’ than ‘If’ the Yuan starts to float freely without the Central Bank interventions. A stronger Yuan will no doubt weaken the US Dollar; this, in turn, means that the other currencies, namely the Yen, Euro, AUD and NZD will suffer as the respective Central Banks will need to do more than just rate cuts to further weaken their currencies against the US Dollar.

As one can see from the above points, China is key and perhaps the center of attention. While it is hard to say when the ball will set rolling, one thing is for sure, once the play is set into motion, we can expect it to snowball rather quickly. With the ECB already into negative deposit rates, and the BoJ already at the far end of the scale, a weaker USD could mean that something will have to give.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)