Today’s Economic Events

- Japan M2 Money Stock y/y 3.0% vs. 3.40%

- China Trade balance 392bn vs. 339bn

- China, US Denominated trade balance 60.1bn vs. 52.bn

- France CPI m/m 0.20% vs. 0.10%

- Eurozone industrial production m/m -0.70% vs. -0.20%

- SNB Board member Zurbrugg Speech

Coming up

- US Crude Oil inventories

- Fed’s Beige Book

The Asian markets saw the risk-on mode building up in the markets since yesterday. The Japanese Yen was trading considerably weaker as concerns from China show signs of receding for now. The Nikkei225 Index closed the Asian session with gains of 2.88% while the Shanghai Composite continued to remain flat, losing -2.40% for the day today. Data from China today included the China trade balance numbers which showed a trade surplus of over $60 billion for the month as exports fell 1.40% compared to a year before while imports declined 7.60%. The demand in exports was attributed to weak global demand for Chinese goods.

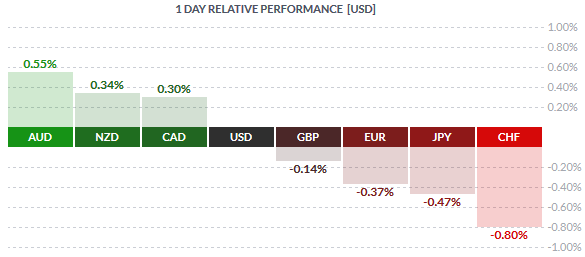

The Yen is weaker with USDJPY gaining 0.48% for the day, trading near the intraday highs of 118.2 in a steady uptrend since the market opening today and is currently trading at a 2-day high. The commodity risk currencies were also stronger in today’s trading with AUDUSD gaining 0.54%, at 0.702 after briefly flirting near intraday highs of 0.704. NZDUSD is also modestly higher at 0.25%, trading near 0.65574.

The European session saw the Euro continue to a pullback in today’s trading. EURUSD was trading at 1.081 at the time of writing posting a steady decline since the market open. Data from the Eurozone included French CPI which showed an increase in consumer inflation to 0.20% after declining -0.20% previously. Eurozone Industrial production was weak, falling -0.70% after rising 0.80% previously. On a YoY basis, industrial production grew at a pace of 1.10%, compared to 1.30% expectations.

The British Pound was trading flat today after posting steep losses on weak Industrial and Manufacturing production numbers released yesterday. GBPUSD is down -0.15% for the day, trading at 1.442 after posting an intraday low to 1.44 before pulling back higher. Equity markets in Europe were also higher following their global counterparts. The German DAX is up 1.05% while the London FTSE100 is up 1.08% for the day.

[Tweet “WTI is trading 3.11% at $31.54 a barrel, ahead of the US Weekly Crude Oil inventories report”]

Crude Oil prices which touched an 11-year low earlier this week saw a continued bounce as investors managed to pick up the WTI Crude Oil at a discount. For the day, WTI is trading 3.11% at $31.54 a barrel, ahead of the US Weekly Crude Oil inventories report which is expected to show a buildup 1.9 million barrels after posting a drawdown of -5.1 million a week before. Gold prices remain on the back foot, giving back the gains from last week. At the time of writing, Gold is down -0.41% lower, trading at $1082 to an ounce, posting a 4-day low.

The remainder of the evening is marked with the US Fed’s Beige Book and Federal Budget balance following the Crude Oil inventories. US markets remain upbeat, with the pre-market futures showing the Dow Jones 0.69% higher while the S&P500 Index is trading 0.87% higher ahead of the open.

Currency market snapshot – (12:44GMT)

Commodity risk currencies take the lead as safe-haven Yen, CHF retreat.